US TSYS: Yields Up on NFP Beat, Near Term O/Look to Neutral for Yields

NFP growth was far stronger than expected in January at 130k (est. 65k) after two-month revisions of -17k (mainly in Nov). Private payrolls saw a larger beat, both with the 172k (68k est) in January but with also a two-month revision of +49k (fairly evenly split over Dec and Nov). However, the Jan increase was led by a huge 124k rise from health & social assistance, a cyclically insensitive category that has been a lifeline for private sector job creation.

10-Yr cash had rallied c. 14bps from the February highs of 4.28%, reaching 4.14% in the days leading into NFP and below mid-point of the 1M range. Unsurprisingly the release saw a significant sell off, with yields in the front end up almost +6bps.

- The 2-Yr is up +5.8bps at 3.514%

- The 5-Yr is up +4.2bps at 3.745%

- The 10-Yr is up +2.8bps at 4.174%

- The 30-Yr is up +2.2bps at 4.808%

- A $42B 10Y note auction saw a 2.39x bid-to-cover vs. 2.55x prior.

- KC Fed Pres. Schmid (not a 2026 FOMC voter) continued a hawkish monetary policy view in a speech Wednesday saying "With demand outpacing supply and inflation running closer to 3% than 2%, I see it as appropriate to maintain a somewhat restrictive policy stance."

- Projected rate cut pricing cooling significantly Wednesday vs. late Tuesday levels (*): Mar'26 at -1.5bp (-5.2bp), Apr'26 at -5.6bp (-11.6bp), Jun'26 at -17.9bp (-26.3bp), Jul'26 at -26.6bp (-35.6bp).

Futures have opened up flat at 112-09 in Asia today, atop the 100-day EMA of 112-08+

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH Downtrend Reaffirms, Oversold On RSI, But Upticks Likely To Be Sold

Spot USD/CNH got to fresh lows of 6.9628 in Monday trade (levels last seen in the first half of 2023), amid broader USD softness as Fed independence concerns crept back into the market. We track just under 6.9700 in early Tuesday dealings, with a downtrend in the pair still intact. Note we have crept back into oversold conditions per RSI (14) (latest read around 28.3), but upticks in the pair are likely to remain sold. The 20-day EMA resistance point is under 7.0000, which is also close to earlier 2026 highs. Downside focus is likely to rest around 6.9500, then potentially 6.9000. Spot USD/CNY finished up at 6.9731, while the CNY CFETS basket tracker rose further to 98.64, fresh highs since early April last year.

- Amidst a downtrend in the USD/CNY fixing and potentially positive January yuan seasonality, risks for USD/CNH remain skewed lower, despite reaching oversold status per RSI. The yuan stands to benefit from diversification flows amid fresh Fed independence concerns.

- The USD/CNY fixing will remain in focus for signs of pushback on the stronger yuan bias, although recent error terms are sub wides.

- Our China policy team noted late yesterday: China should allow the yuan to trade with greater flexibility, giving market forces a larger role, as Beijing continues its push to boost international use of its currency, said Huang Yiping, a member of the People’s Bank of China’s Monetary Policy Committee. Foreign-exchange policy needs to become more flexible, and if market pressure for yuan appreciation intensifies, regulators should allow market forces to play a greater role, Huang argued.

- On the data front we still await Dec new loans/ aggregate finance data, while tomorrow Dec trade figures are due.

AUSSIE BONDS: Little Changed, AU-US 10Y Diff Holding Post-CPI Narrowing

ACGBs (YM flat& XM +1.0) are little changed after cash US tsys finished slightly weaker on Monday amid uncertainty over future Federal Reserve independence. This came after the DOJ announced it's investigation of Fed Chairman Powell over the weekend related to his testimony before the Senate Banking Committee last June.

- Geopolitical tensions continue to heat up (or at least simmer) after the US attack on Venezuela, followed by threats to Iran and Greenland.

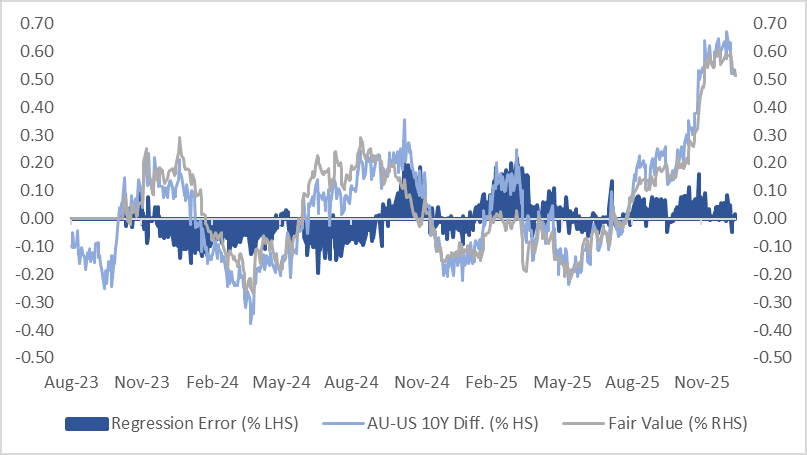

- Cash ACGBs are flat to 1bp richer with the AU-US 10-year yield differential at +51bps. A simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month (1Y3M) swap spread over the past two years suggests the current spread sits at its regression-implied fair value.

- The bills strip is flat to -2 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 33% for February to 96% by June and 140% by December 2026.

- Today, the local calendar will see Westpac Consumer Confidence.

- This week, the AOFM plans to sell A$300mn 4.75% 2054 bond on Tuesday, A$1bn 4.25% 2036 bond on Wednesday and A$700mn 3.25% 2029 bond on Friday.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Bloomberg Finance LP / MNI

AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.870 @ 16:25 GMT Jan 12

- SUP 1: 95.740 - Low Dec 22

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices bounced again Thursday, supported by strength in global bond markets and a smoother inflation picture at the December CPI print. As such, prices edged further away from recent lows. Nonetheless, slower pricing for additional RBA easing - and partial pricing for a return to rate hikes in 2026 - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.