SECURITY: WSJ Confirms Additional US Warships/Troops Deployed To Middle East

The Wall Street Journal reports, "The Pentagon is sending three warships and thousands of additional Marines to the Middle East." The report supports a Newsmax piece yesterday noting, "Six amphibious ships will add about 8,000 service members in the region, including 4,000-5,000 Marines."

- The Journal, "Roughly 2,200 to 2,500 Marines from the California-based USS Boxer amphibious ready group and 11th Marine Expeditionary Unit are heading to the U.S. Central Command, responsible for all American forces in the Middle East... This is the second massive deployment of Marines in the past week, after the Pentagon sent the Japan-based USS Tripoli and 31st MEU to the region."

- When asked yesterday about US 'boots on the ground', Trump gave his stock answer to questions regarding military strategy: “No. I'm not putting troops anywhere," but "If I were, I certainly wouldn't tell [reporters]…”

- MNI's Political Risk Team wrote in today's US Daily Brief, noting the Newsmax article, that such a large-scale military deployment is "consistent with imminent military action." While some analysts may conclude the buildup is aimed at increasing leverage, previous such buildups in Ukraine, Venezuela, - and the Middle East ahead of this conflict -, have resulted in kinetic and ground operations.

- Confirmation of the deployment comes amid reports that the US is weighing two possible ground operations in Iran: One to secure defensive positions around the Strait of Hormuz; another to seize control of Iran’s crucial oil and gas export terminal on Kharg Island. No reports have suggested a final decision has been taken.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Data & Swelling $IG Supply Weighs

A swelling $IG supply slate (11 deals announced in the last 30 minutes or so, with the BBG underwriter survey indicating around 10 borrowers plan sales today) adds to the pressure that came on the back of the 08:30 NY data.

- TY futures to fresh session lows at 112-30, through initial support at the Dec 18 high (112-31), with the next downside level of note located at the Feb 11 high (112-20).

- Block sale of TY futures (14,977 lots/~$990K DV01 at 112-31+) adds further weight.

- Yields 1.0-2.5bp higher, curve bear flattens.

- FOMC meeting minutes and 20-Year supply due later.

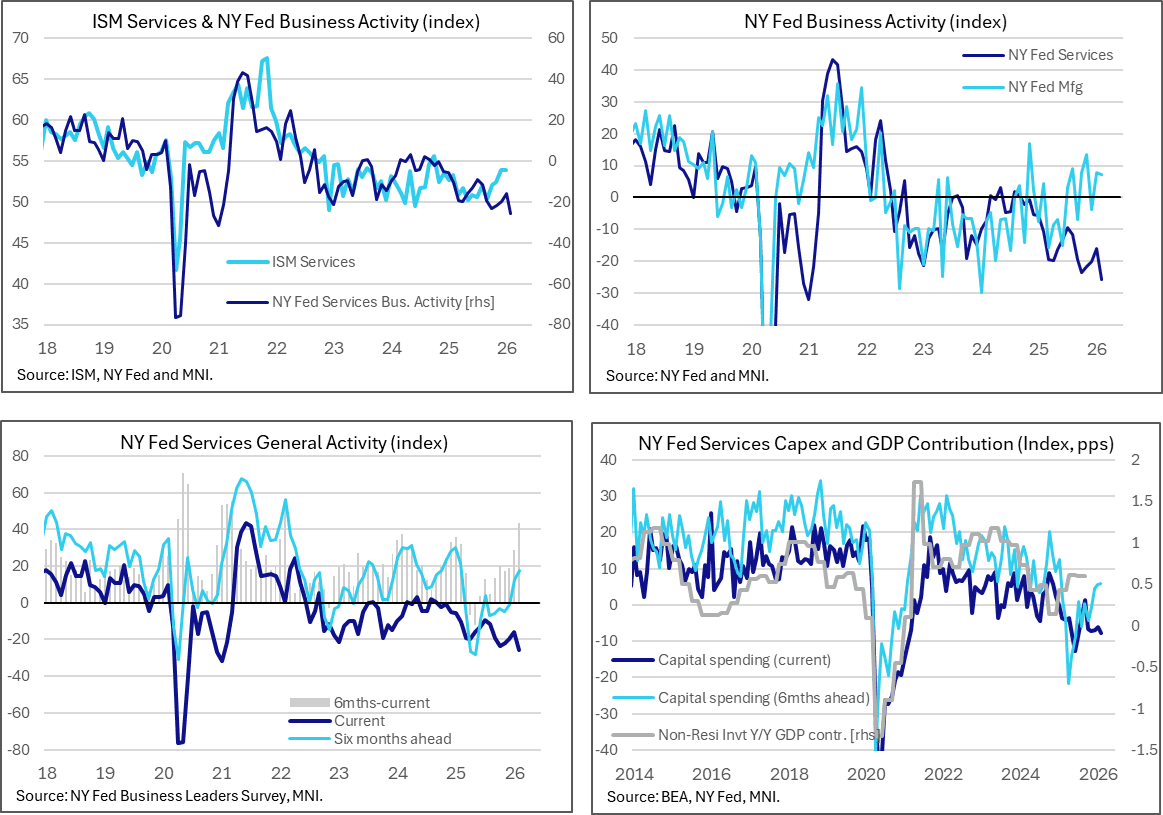

US DATA: NY Fed Services Activity Hits Five-Year Low But Stronger Expectations

The NY Fed’s Business Leaders Survey of services firms had mixed implications, with the current general activity index falling to a five-year low despite a further improvement in six-month ahead readings. The gap between six-month ahead and current general activity readings is at its relatively most optimistic since early 2022.

- The headline activity index fell 9.6pts to -25.7, below the -23.6 of Oct 2025 for a five-year low.

- The business climate index fell 7.3pts to -41.7, even if that remained above the -43.1 averaged in Oct-Dec and the post-pandemic low of -60.7 from Apr on global tariff announcements.

- Employment was also weak, falling 4.2pts to -9.7 as it pushed below the -8.6 in Nov for its lowest since early 2021. It notched up a sixth consecutive month in contraction territory.

- Against that, the wages index climbed 7.4pts to 37.4 for its highest since Feb 2025.

- “The prices paid index held steady at 62.6, and the prices received index was stable at 29.9, pointing to little change in the pace of both input and selling price increases.”

- “The supply availability index dipped six points to -9.2, suggesting supply availability worsened modestly.”

- Going against this, the six-month ahead general activity index increased 5.1pts to 17.5, its highest and also the second consecutive month in expansionary territory for the first time since Feb 2025.

- Capital expenditure plans are one area helping here, inching up 0.3pts to 6.0 for the highest since Jan 2025. They have seen a less pronounced increase in recent months than in their manufacturing counterpart, yesterday reporting a 7.9pt increase to 18.2 for the highest since Feb 2023.

US TSY FUTURES: BLOCK: Mar'26 10Y Post-Data Sale

- -14,977 TYH6 112-31.5, sell through 113-00 post time bid at 0842:22ET, DV01 $990,000.

- The 10Y contract trades 112-31 last (-5)