SECURITY: White House Denies Shortages Ahead Of Meeting w/Defence Contractors

Mar-06 16:08

US President Donald Trump is expected to meet defence contractors at the White House today, amid con...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: MNI Reports on Possible European Union Swap Line Proposal

Feb-04 16:06

- MNI reports on a possible European Union swap line proposal -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

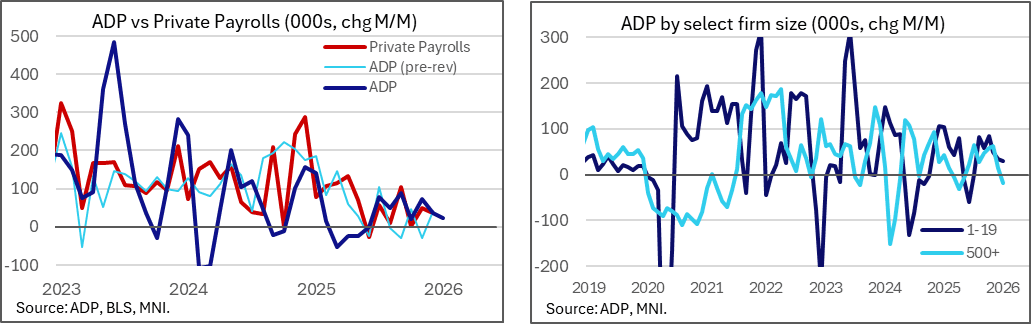

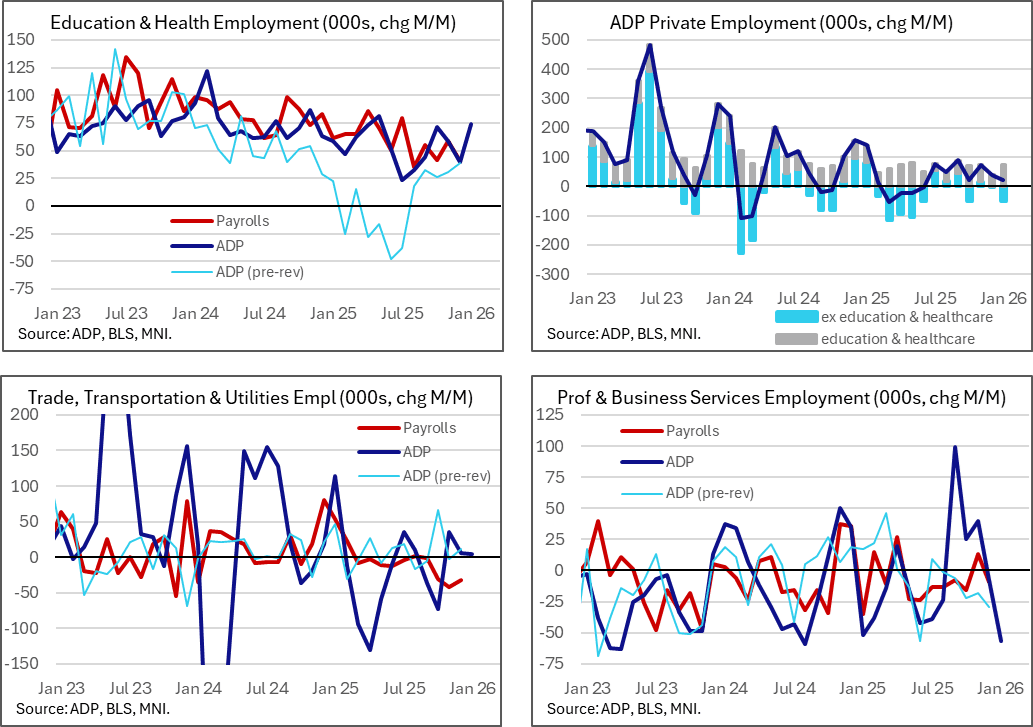

US DATA: ADP Revisions See Healthcare As A Major Driver, Echoing Payrolls

Feb-04 16:01

The wide-ranging revisions have seen the education & healthcare sector provide a much larger contribution, more closely reflecting trends in BLS private sector job creation.

- Education & healthcare jobs increased a cumulative 642k over 2025 vs the 28k previously estimated.

- This net revision of +614k across 2025 was in stark contrast to most industries considering the cumulative revision of -216k. The next largest positive revision was other services at +39k whilst the largest downward revision was trade, transportation & utilities at -325k.

- The BLS private payrolls data have for some time shown a large contribution from health & social assistance, rising 49k on average in the three months to December vs -19k for all other private industries.

- The broader ADP category of education & healthcare has now increased an average of 58k per month in the three months to January vs -13k for other industries.

- This reliance on healthcare has received plenty of attention, including Governor Bowman on Jan 30 (link): "Despite some tentative signs of the unemployment rate leveling off, it seems too early to say that the labor market has stabilized,... Job gains have been concentrated in just a few nonbusiness service industries that are less cyclically sensitive, with health care accounting for all private job gains last quarter."

US DATA: ADP Employment Sees Modest Miss and Large Downard Revisions On QCEW

Feb-04 15:59

ADP employment was a little softer than weekly tracking had implied with a larger miss against Bloomberg consensus. It was part of a release that was clouded by some large annual revisions, negative across 2025 as a whole but with a small net upward revision to Q4.

- ADP private employment was softer than Bloomberg consensus in January, rising 22k vs 45k expected, with the latest weekly series’ 31k monthly equivalent having hinted at risk of a downward surprise as we had flagged.

- However, the fact it was broadly close to consensus seems down to luck as much as anything following large annual revisions.

- Cumulative private sector jobs growth now stands at 398k across 2025 vs the 614k seen after last month’s update.

- These downward revisions were concentrated in the first half of 2025 whilst more recently there were net upward revisions in Q4 owing to a large change to Nov (+74k vs -29k). It leaves the latest three-month rate at 44k, unchanged from 44k in December vs what was originally 20k.

- The monthly profile now shows what was a much more aggressive slowdown in job creation back in March, with a particularly large downward revision to -53k vs +147k shown in last month’s vintage (linked to QCEW revisions – more on this below). March also coincided with an increased touting of tariff threats before the Liberation Day announcements in April and indeed the three-month average has for now bottomed at -33k in May before recovering in 2H25.

- On today’s revisions: “The January 2026 report reflects a scheduled annual revision of the ADP National Employment Report. The data series has been reweighted to match the Quarterly Census of Employment and Wages (QCEW) benchmark data through March 2025.”

- “Beginning this month, in addition to the annual benchmark revision, the ADP National Employment Report also will reflect data from the most recent QCEW release.”

- Recall that these QCEW data have been pointing to significant downawrd revisions to the level of nonfarm payrolls to March 2025. Fed Chair Powell has previously estimated a hit worth circa 60k/month.