US DATA: Weak Philly Fed Mfg Activity With Higher Prices, But Outlook Brightens

Aug-21 12:57

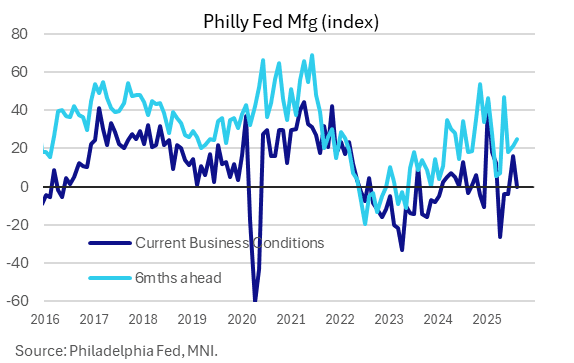

The Philadelphia Fed's Business Outlook survey showed a bigger-than-expected relapse in regional manufacturing activity in August, along with a continued surge in prices paid - making for a largely stagflationary report, albeit with some improvement in forward-looking indicators.

- The a -0.3 reading for current general business conditions (6.5 expected, 15.9 prior) brought it back negative where it had been for 4 consecutive months amid tariff-related concerns, before jumping to a 5-month high in July.

- The internals for current activity were poor. New orders were negative for the first time in 4 months, falling to -1.9 from +18.4 (suggesting a decline in orders). Shipments fell to a 3-month low 4.5 from 23.7, while employment also slipped, to 5.9 from 10.3 - these suggest growth but much weaker than prior.

- One saving grace on the activity front was that the outlook improved, with 6-month ahead sentiment up to 25.0 from 21.5, for the highest reading in 3 months. future new orders and future shipments rose to the highest in 3 months, with future capex more than doubling to 38.4, highest since January (the latter has historically been seen as a leading indicator of national non-residential investment).

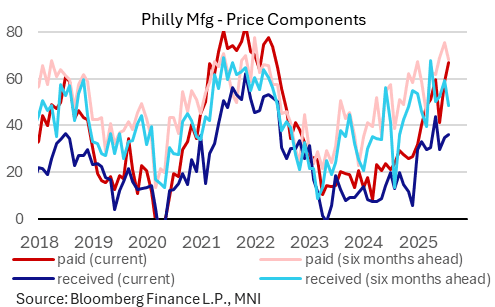

- However, there were very pronounced price pressures in the survey: current prices paid rose to 66.8 from 58.5, with prices received not keeping pace, up to a 39-month high 36.1 from 34.8. Again, the outlook was the silver lining, with 6-month-ahead prices paid dipping to 68.4 from 75.3, and received to 48.5 to 59.4.

- Philly Fed's survey echoed that of the neighboring district covered by the NY Fed in the price pressure department, but its decline in activity stood out versus Empire's.

- That leaves it a little early to tell what the readthrough of the regional surveys is for the national manufacturing picture, though this should become clearer with August PMI, Dallas Fed, and Richmond Fed data through early next week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: Sep'25 10Y Calls

Jul-22 12:56

+29,000 TYU5 112 calls, 27 vs. 111-07/0.31% - total volume near 60k

US DATA: Philly Fed Services Sentiment Greatly Improved, Amid Stubborn Inflation

Jul-22 12:55

The Philadelphia Fed's Nonmanufacturing Business Outlook Survey continued to show improvement in July, though cost pressures remained elevated.

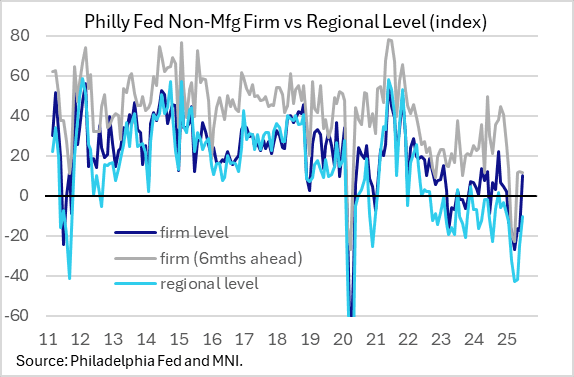

- The regional current general activity index rose to a 6-month high -10.3 from -25.0 prior. This was the 3rd consecutive improvement since bottoming at -42.7 in April amid tariff policy concerns.

- Even more impressively, the index for current general activity at the firm level increased to 10.2 from -17.3, the first positive reading since January and the highest outright since October 2024.

- The regional question asks respondents what their assessment if of general business activity for the region, while the latter asks for their assessment of activity for their own firm. Throughout the tariff episode, firms have been much more positive about their situation than they have been on the regional picture.

- The subindices were strong: new orders rose to 9.7 from -20.1; revenues 11.8 from 3.4; full-time permanent employment 4.1 from -2.1, albeit there were some pullbacks in capex and part-time employment.

- Future assessments were steadier, with the 6-month regional outlook at -3.9 from -8.2 prior, and firm-level ticking lower to 11.7 from 12.3.

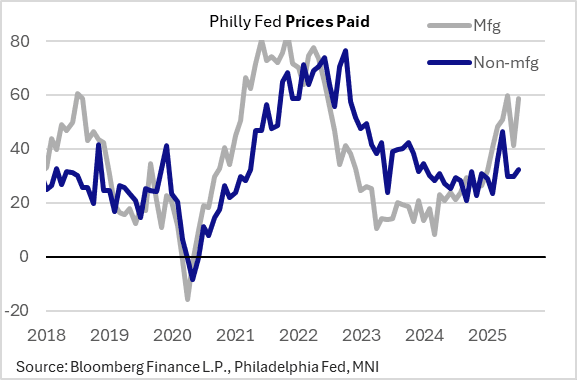

- That said, price pressures increased: current paid ticked up to a 3-month high 32.5 from 29.7, and prices received jumped to 12.4 from 2.2, marking a 7-month high.

- These results mirror those seen in the NY Fed's Empire services survey: price pressures remaining elevated vs 2024 but not nearly as pronounced as for manufacturers.

MNI: US REDBOOK: JUL STORE SALES +5.2% V YR AGO MO

Jul-22 12:55

- MNI: US REDBOOK: JUL STORE SALES +5.2% V YR AGO MO

- US REDBOOK: STORE SALES +5.1% WK ENDED JUL 19 V YR AGO WK