US COMMUNICATIONS: Warner Bros Discovery: Scenario Analyses

• The first round of non-binding bids for WBD was due on Nov. 20th and PSKY, CMCSA and NFLX reportedly submitted bids. Another round of bids is expected in the coming weeks, with the auction targeted to conclude by year-end.

• We assess four scenarios with a focus on the resulting capital structures:

• WBD executes its planned 1H26 split (30% probability)

• PSKY acquires all of WBD (45% probability)

• CMCSA acquires WBD’s Studios & Streaming (15% probability)

• NFLX acquires WBD’s Studios & Streaming (10% probability)

• We consider regulatory and financial hurdles of the respective transactions in our probability odds.

• We see streaming concentration as a regulatory hurdle to NFLX+WBD S&S and view the deal as strategically additive, rather than essential for NFLX, reducing the incentive to stretch on valuation.

• We see regulatory hurdles in a CMCSA+WBD S&S deal due to the company’s history with the current administration and view its higher equity portion as relatively unattractive.

• We view the PSKY+WBD transaction as most likely, with modest regulatory scrutiny on linear concentration surmountable.

• Scenario 1) WBD separates into Studios & Streaming (S&S) and Global Networks (GN) following the spinout as planned in 1H26 (30% probability)

• WBD would refinance its $16B secured bridge loan (originally $17B) with new secured HY bonds. The loan currently carries SOFR+300bps, stepping to +350bps on 12/31/2025 and +400bps on 03/31/2026.

• We estimate ~$7.5B of new secured HY bonds at the S&S entity which has consensus 2026 EBITDA of $3.9B, for 1.9x and 1.7x gross and net leverage, respectively.

• The remaining $26B of new secured and legacy unsecured bonds would be at the GN entity. Consensus 2026 EBITDA is $5.6B which implies ~4.6x and 4.0x gross and net leverage, respectively.

• GN could utilize FCF supported by solid but declining EBITDA to reduce debt, in addition to monetizing its 20% retained stake in S&S over time.

• The legacy unsecured bonds would trade well wide of the secureds and we note the difference between Ba2/BB/BB+ and Ba3/BB/BB+ rated bonds based on junior lien exchange rights from participation in the June 2025 tender.

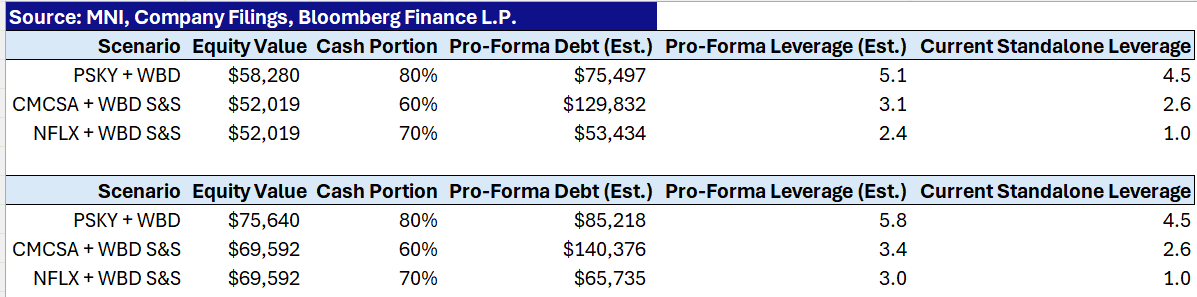

• Scenario 2) PSKY acquires all of WBD (45% probability)

• We consider $23.50-30.50/share as our valuation bounds which imply ~$58B-$76B equity value. The low end reflects 5x and 15x GN and S&S 2026 consensus EBITDA estimates, and the high end reflects 5x and 19.5x GN and S&S 2026 EBITDA estimates.

• PSKY’s bid is said to be majority cash, so we consider an 80% cash scenario (60%-90% scenarios available on request).

• Further, we assume Larry contributes 30% of the cash portion (10%-50% scenarios available on request), with the rest being debt funded.

• We use 2026 consensus EBITDA estimates of $8.7B and $3.5B for WBD and PSKY, respectively and estimate ~$2.5B synergies for the pro-forma (PF) company.

• $58B EV; $75.5B PF debt and 5.1x gross leverage, from current 4.5x

• $76B EV; $85.5B PF debt and 5.8x gross leverage

• In this scenario, we think the capital structure could be split between secured IG bonds and unsecured HY bonds, akin to CHTR’s capital structure, with optionality for hybrid issuance to contain ratings pressure.

• Scenario 3) CMCSA acquires WBD’s S&S (15% probability)

• We think WBD’s GN would continue with its spinout. A combination of WBD’s GN and CMCSA’s Versant had been rumored and a combined entity would have ~$8B 2026 EBITDA and ~$29B debt implying ~3.6x gross leverage. Declining EBITDA could initially be offset by a prioritization of FCF for debt paydown.

• Consistent with assumptions in scenario 1, we estimate S&S would have ~$7.5B of debt, ~$1B cash and we consider $52B and $70B equity values - 15.0x and 19.5x 2026 consensus EBITDA.

• Given CMCSA’s $9.3B cash, $15B estimated 2026 pre-div. FCF and higher baseline leverage, we would expect a higher equity funded portion, reducing competitiveness.

• We consider a 60% cash funded deal (30%-80% scenarios available on request) and estimate CMCSA uses $7B of balance sheet cash - does not include proceeds from VSNT. We estimate $1B synergies.

• $52B EV; $130B PF debt and 3.1x gross leverage, from current 2.6x

• $70B EV: $140B PF debt and 3.4x gross leverage

• We estimate an initial high-BBB rated capital structure.

• Scenario 4) NFLX acquires WBD’s S&S (10% probability)

• WBD’s GN would still be spun out, although its long-term strategy would be more uncertain.

• We consider $52B and $70B equity values for S&S and given NFLX’s lower baseline leverage, we think its bid would have a higher cash portion, although we acknowledge NFLX’s strong equity currency.

• We look at a 70% cash funded deal (60%-90% scenarios available on request) and estimate NFLX uses $4B of balance sheet cash. We estimate $1B synergies.

• $52B EV; $53B PF debt and 2.4x gross leverage, from current 1.0x

• $70B EV: $66B PF debt and 3.0x gross leverage

• We estimate a high-BBB capital structure initially, with upside dependent on management’s commitment to deleveraging.

Sources: MNI, Bloomberg Finance L.P., Company Filings

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: MNI Fed Preview - October 2025: QT, Or Not QT

MNI's preview of the October FOMC has been published - Download Full Report Here

- The Federal Reserve is overwhelmingly expected to cut the funds rate by 25bp for a 2nd consecutive meeting on October 29, bringing the target range to 3.75-4.00%.

- This will again be framed as a risk management cut, with the limited data available since the September meeting not disconfirming that the shift in the balance of risks had tilted toward labor market downside.

- Dissent to this decision should once again be limited to Gov Miran in favor of a 50bp cut.

- With limited new developments and official data to opine on, Chair Powell’s press conference will be eyed for affirmation that a December cut remains on track, as signalled by the most recent Dot Plot.

- He’s unlikely to give much away, but it would be surprise given the lack of data and relevant developments if he suggested that a further 2025 cut was in any greater doubt than it was 6 weeks earlier.

- Instead, we think focus in terms of action at this meeting will be on the balance sheet, with the Fed likely to announce an end to quantitative tightening amid diminishing reserve levels and nascent evidence of funding market pressures.

- We will also be watching for any news on the Fed’s communications framework, with an updated “Dot Plot” potentially unveiled at some point by year-end.

MNI’s separate preview of sell-side analyst summaries to follow on Monday Oct 27

RATINGS: Moody's Lowers France's Outlook To Negative, Maintains Aa3 Rating

Moody's has lowered its outlook on France to negative from stable.

- Moody's was expected to at least lower the outlook, so this is not a surprise - there had been some risks perceived of a downgrade to A1 (from Aa3) in the domestic and foreign currency long-term issuer and domestic-currency senior unsecured ratings.

- Per the Moody's release: "The decision to change the outlook to negative reflects the increased risk that the fragmentation of the country's political landscape will continue to impair the functioning of France's legislative institutions. This political instability risks hampering the government's ability to address key policy challenges such as an elevated fiscal deficit, rising debt burden, and durable increase in borrowing costs, thus leading to a more rapid weakening in France's key fiscal metrics than we currently expect."

- Both S&P and Fitch have already downgraded France’s sovereign rating to the single-A bucket this year.

USDCAD TECHS: Corrective Pullback

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4167 50.0% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.4111 High Apr 10

- RES 1: 1.4080 High Oct 16 and the bull trigger

- PRICE: 1.4016 @ 16:33 BST Oct 24

- SUP 1: 1.3979/3907 20- and 50-day EMA values

- SUP 2: 1.3829 Bull channel base drawn from the Jul 23 low

- SUP 3: 1.3769 Low Sep 19

- SUP 4: 1.3727 Low Aug 29 and a bear trigger

USDCAD has pulled back from its recent highs. The trend condition is bullish and a move lower is considered corrective. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4111, the Apr 10 high, and further out, scope is seen for an extension towards 1.4167, a Fibonacci retracement. First key support lies at 1.3907, the 50-day EMA. Support at the 20-day EMA lies at 1.3979.