EU CONSUMER STAPLES: Walgreen Boots; latest on Sycamore buyout

(WBA: B1 Neg/BB- Stable)

Strong move in $-long end as leaks on debt financing continue. Reminder on the ($26s, $30s, $46s, $50s) we see mention to all three (instead of two) raters requiring downgrade - i.e. includes Fitch, who has not had a rating on it since 2021.

Re. leaks there is again mention of bankers working on $12b in debt funding including $4.5b from private lenders. The new debt will be issued against the individual entities (Sycamore plans to split it up post acquisition) and leaks mention $2.75b in bonds towards financing the UK Boots business/spin-off (may see visit to £/€ HY markets). Reminder leaked equity value is coming in at $10b. If we assume the current $6.25b debt stack will be forced refi, then it implies 40%/$4b in equity financing.

Re. history, Sycamore bought Staples for $6.9b in 2017, reports were $5.7b in debt (17% equity financing). Staples was light on debt with $1b across a Jan-2018 and 2023 bond - both with CoC at 101 under a ratings trigger. The 18s were par callable from Dec-2017 and pulled at 100.42 then. The 23s it launched a tender at $101.25 alongside a consent to remove the CoC clause - it did receive majority, looks like it cleaned up un-tendered (bbg has it marked as called a few months after the tender closed at $118.56). Staples was on the edge of IG but faced a 6-7 notch downgrade on that acquisition unlocking the CoC.

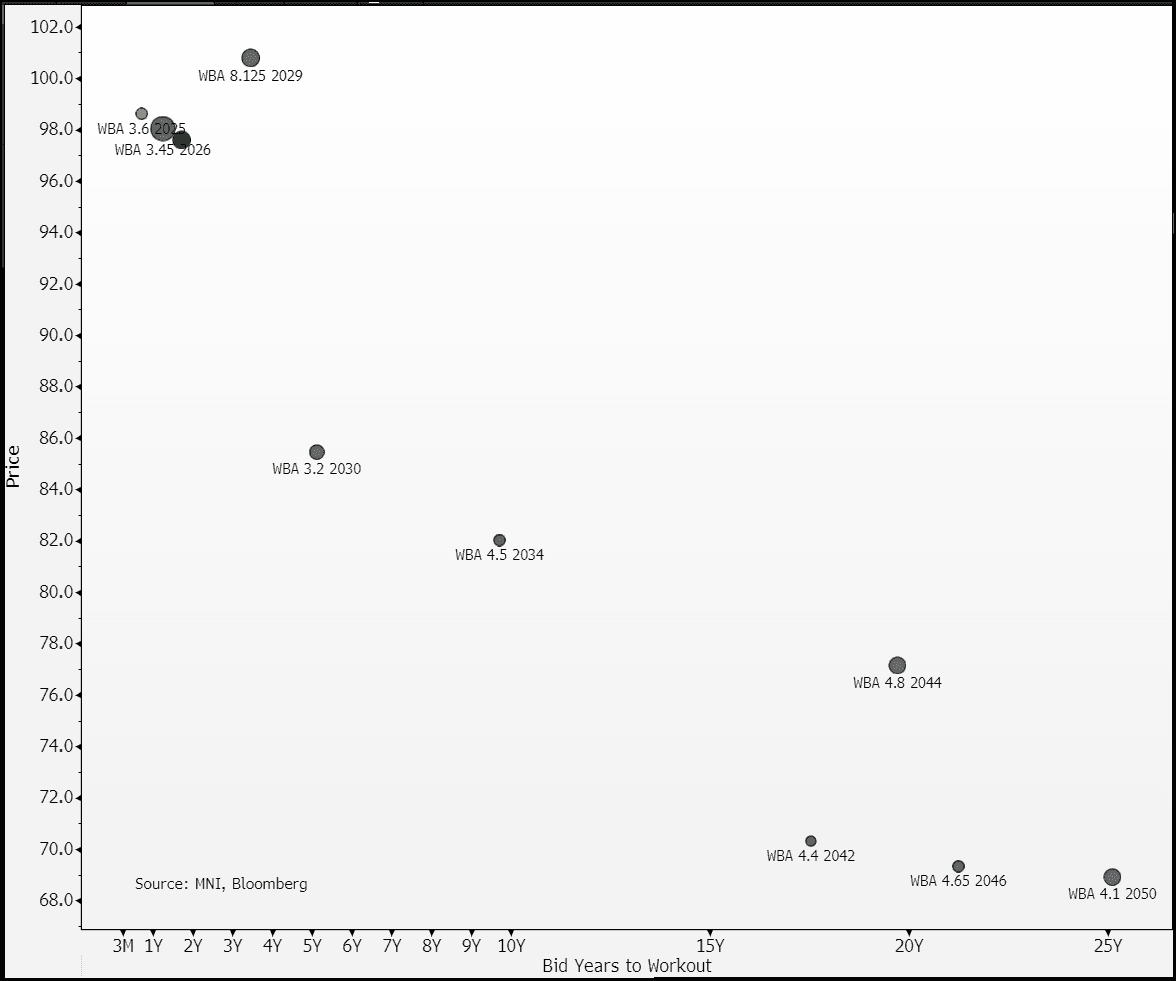

- Equities +5.6% at $10.8 vs. leaked $11.3-11.4 (+5% left)

- $34 +2pts at $83

- $44 +2.6pts at $80

- $46 +5.2pts at $76

- $50 +6.9pts at $76

- 5Y $CDS +550 (+32)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: /SWAPS: J.P.Morgan recommend 10-Year swap spread wideners.

J.P.Morgan recommend 10-Year swap spread wideners.

- They suggest that relative narrowness in the “10-Year swap spread on valuation frameworks likely reflects a combination of: 1) upcoming 10Y syndicated gilt supply in February with a new gilt Mar35 planned for w/c 10 February, and 2) markets pricing in some uncertainty around increased gilt supply at the March OBR forecast update and DMO remit announcements.”

- However, they stress that this is “very much a tactical short-term view as the ongoing BoE APF reduction and likely upward skew to gilt issuance expectations should put narrowing pressure on 10Y swap spreads over the medium term.”

EUROZONE DATA: Upward Revision To Jan Manufacturing PMI, Employment Signals Weak

The Eurozone manufacturing PMI saw a five tenth upward revision to 46.6 (vs 46.1 flash, 45.1 prior), driven by a notable upward revision in Germany to 45.0 (vs 44.1 flash).

- Both new orders and production saw smaller declines than in December, helping the EZ aggregate tick higher. Spain and Greece continued to outperform Eurozone peers.

- Downticks in industrial employment were noted across the four major Eurozone economies. From the EZ release: “Employment levels were cut further at the start of 2025, with the rate of job shedding accelerating fractionally. This marked a twentieth successive month that factory staffing numbers have declined”.

- There was an acceleration in input cost price pressures in January, and business “refrained from passing on higher costs to their customers”, bringing a “four-month sequence of discounting to an end”.

- December industrial production data is due from France (Weds), Germany (Fri) and Spain (Fri) this week.

BUNDS: Curves Steepen Towards Next Upside Levels

The dovish repricing linked to tariff-related growth worry promotes bull steepening on the German curve this morning.

- 2s10s within 0.5bp of the October 21 ’22 high (36.7bp).

- 5s20s ~3bp off the ’24 treble top area (~51.1bp).

- Levels above are based on closing prices.