BSP: VIEW: Goldman Look For 4.50% Policy Rate At End ‘22

In the wake of yesterday’s BSP decision, Goldman Sachs note that “going forward, as the economy continues to recover, with rising inflation expectations and hawkish monetary board, we now expect the BSP to deliver a 50bp hike in August and consecutive 25bp hikes from September onwards bringing the policy rate to a terminal rate of 4.50% at the end of 2022 (vs. 4.00% in Q123 previously).”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

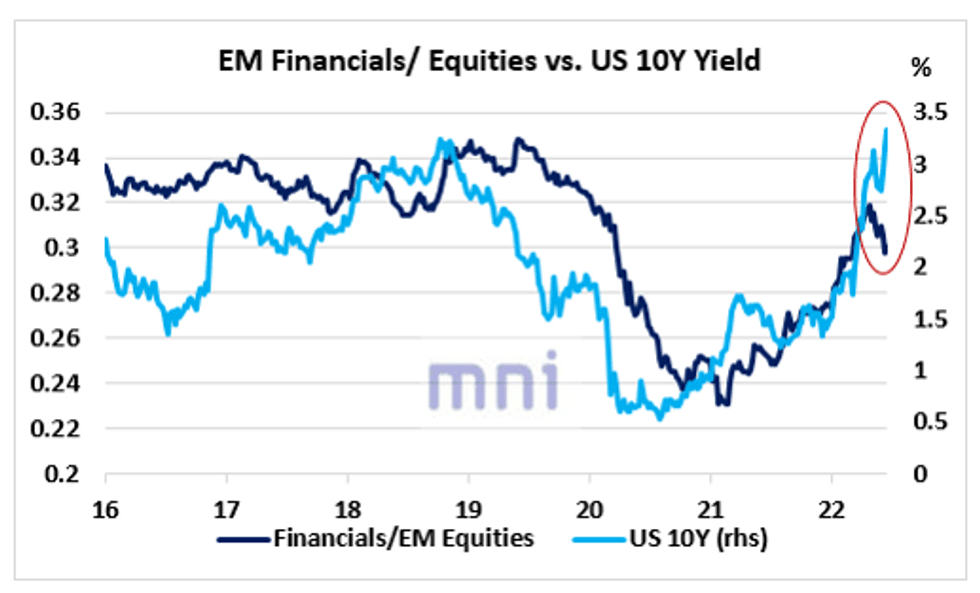

GLOBAL: Worsening Outlook Leaves EM Cyclical Stocks Vulnerable

Executive summary

- Even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields are surging), EM financials have been underperforming the market in recent weeks as global outlook worsens.

- In addition, the fall in China real M1 (in 2021) has been pricing in ‘cheaper’ financials for months.

- Hence, as the global outlook is not about to change anytime soon, the ‘cheap’ EM cyclical sectors may continue to underperform in the near term and defensive allocation should continue to be investors key allocation in the coming months.

EM Financials Underperform As Economic Slowdown Accelerates

The significant liquidity injections following the Covid shock combined with the surge in ST and LT bond yields had been a strong driver of EM financial stocks until the Ukraine invasion.

However, we mentioned after the start of the war in the end of February that the momentum on cyclical stocks was clearly unsustainable as the economic outlook was set to worsen considerably. The chart below shows that even though selling pressure on LT government bonds remain elevated (i.e. LT bond yields continue to surge), EM financials have been underperforming the market in recent weeks.

Source: Bloomberg/MNI

AUSSIE BONDS: 10-Yr ACGB Yield Hits Eight-Year Peak After Continued Tsy Sell-Off

Cash ACGBs have played catch-up with continued sell-off in U.S. Tsy space seen on Tuesday. The curve shifted higher as Sydney trading re-opened, with yields last seen 9.2-10.5bp better off, with belly underperforming. Cheapening impetus pushed 10-Year yield to 4.08% at one point, a fresh eight-year high for that tenor.

- Benchmark futures contracts have been fairly stable in Wednesday's morning trade, YM last deals -8.2 & XM -11.1. Bills run 11-15 ticks lower through the reds.

- Key focus remains on Wednesday's FOMC monetary policy decision, with markets now fully pricing a 75bp hike to the fed funds rate.

- Participants have also been adding hawkish RBA bets. Last night's interview with RBA Gov Lowe played into that dynamic, as the official said higher rates are "necessary" to curb inflation, which can reach +7.0% Y/Y by the year-end.

- Goldman Sachs followed up by revising their RBA call this morning and now expect 50bp hikes to the cash rate target in both August and September.

- In terms of data releases, Westpac Consumer Confidence takes focus today, as participants await Thursday's jobs market report.

NZD: Dips To Fresh Lows Before Stabilizing

NZD fell to fresh YTD lows post the Asia close, dipping just beneath 0.6200. We currently sit slightly firmer at 0.6225.

- Amidst continued broad USD strength, NZD performance has been around middle of the pack compared to the rest of the G10 bloc over the past 24 hours. Outperforming NOK, GBP and JPY but slipping against EUR and CAD.

- Yield momentum continues to move against NZD/USD though, the 2yr NZ-US spread back to lows from July last year. We have moved from a recent high of +86bps back to +39bps.

- Earlier, REINZ house sales printed at -28.4% YoY, versus -35.2% YoY prior. The REINZ house price index fell by 1.6% MoM following declines in April and March. In YoY terms we are now up 3.7%, versus 6.3% in April.

- The Q1 current account deficit printed slightly wider than expected at -6.143bn, versus -5.963bn consensus. The deficit as a share of GDP sits at -6.5% in the 12 months to the end of Q1. Tomorrow Q1 GDP prints.