ILS: USD/ILS Steadies After Rally Through 50-DMA

USD/ILS is building on a recent streak of gains, which resulted in a convincing breach of the 50-DMA (3.4181) yesterday. The rally has continued despite a correction of the greenback's July gains at the start of the month. The rate last trades at 3.4503, around 30 pips lower on the session, with bears looking for a return below the aforementioned DMA. Bulls keep an eye on the 3.5 figure and the 100-DMA, which intersects at 3.5295.

- The Globes circulated a report attributing shekel losses to renewed concerns about the impact of US tariffs, domestic political turmoil and the evolving security situation.

- Reports of a clash between PM Netanyahu and IDF Chief of Staff Zamir re: occupation of Gaza have been doing the rounds, raising questions about the alignment between the army and political decisionmakers.

- The TA-35 Index sits 0.3% higher on the day after printing multi-week lows earlier in the day.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

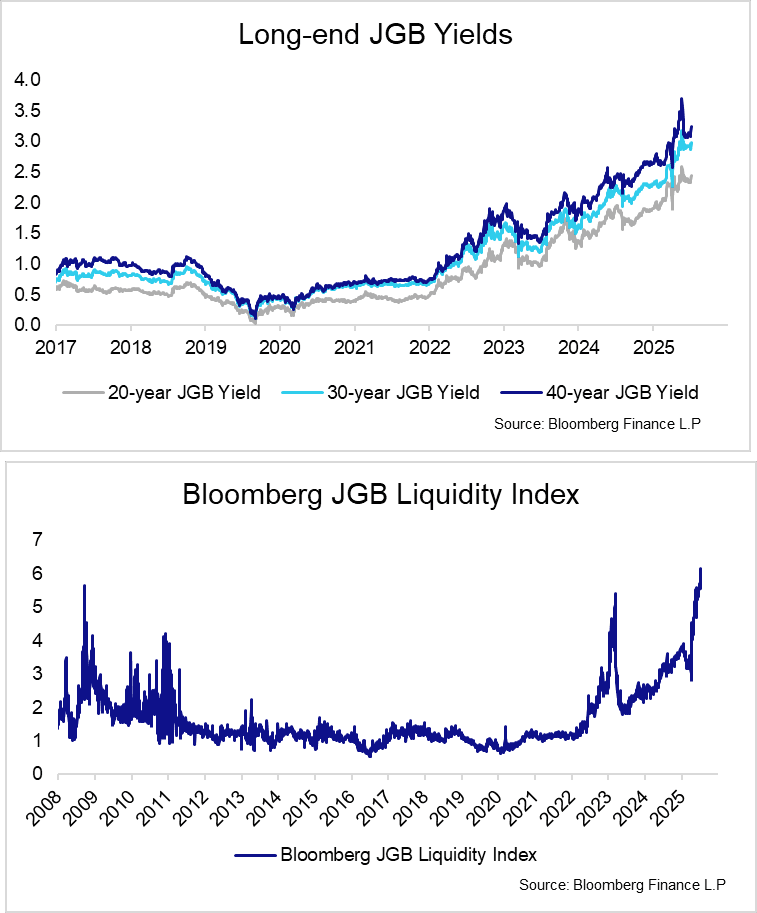

JGBS: Long-end Pressures Resumes Overnight As Election Comes Into View

Long-end JGB yields saw notable upward pressure overnight, with 20-year yields up 6.5bps and 30/40-year yields up 10bps. Yields remain comfortably below the late-May highs, but fiscal risks/concerns appear to be back in focus with the July 20 Upper House election coming into view. After falling by 7bps on Friday amid renewed tariff concerns, 30-year yields are back above last Thursday’s 2.970% high (which came following a mixed 30-year auction).

- May wage data overnight was much weaker-than-expected, with nominal earnings rising 1.0% Y/Y (vs 2.4% cons, 3.0% prior) and real earnings falling 2.9% Y/Y (vs -1.7% cons, -2.0% prior).

- With PM Ishiba’s LDP party already pledging cash handouts of JPY20k as part of its election campaign, the weak wage data may be increasing concerns of more fiscal loosening/household support pledges ahead of the July 20 vote. A reminder that Fitch noted earlier today that while Japanese fiscal risks are contained in the near-term, long-term risks are more significant given ageing-related costs.

- The latest seat projection opinion polling ahead election for the House of Councillors shows PM Shigeru Ishiba's conservative Liberal Democratic Party (LDP) on course to lose a significant number of seats, and potentially for the governing coalition (alongside the Komeito party) to lose its overall majority in the upper chamber of the Japanese National Diet.

- Despite yields remaining shy of year-to-date highs, liquidity at the long-end of the JGB market remains a concern. Bloomberg’s JGB liquidity index is currently at its highest since the series began in 2008 (indicating worse liquidity).

- See our earlier Political Risk post for more colour on current election polling figures.

CROSS ASSET: Headlines Light, Cross-Asset Impetus Dominates

Bond futures move back towards session lows (TY registers a fresh session low).

- Cross-market cues seemingly remain at the fore as crude oil & Euro Stoxx futures move to fresh session highs.

- Crude has shaken off the latest round of speculation OPEC+ production increases, while broader macro headline flow remains relatively limited.

- Little of note on the macro calendar today.

- Trump’s letters surrounding tariff rates (due to be sent at 12:00 NY today) garner much of the interest, although the ongoing fluidity (U.S. willingness to cut deals/moderate tariffs in the past) when it comes to the global tariff backdrop continues to limit visibility on the matter.

GBP: USD Bounce Has Major Pairs Testing Key Levels

- The USD's bounce Monday is providing some relief for the USD Index, which now sits 1% above last week's cycle lows to put the currency on a surer footing. As a result, the major pairs are seeing pressure toward the the post-NFP lows - with EUR/USD and GBP/USD challenging 1.1718 and 1.3586 respectively.

- Rates markets are endorsing USD gains here: the US curve is steeper as the global long-end continues to underperform. This backdrop, allied with any deterioration in trade relations between the US and the RoW remains a key market focus, particularly with the fluidity around Trump's approach to tariffs and the suite of reciprocal trade tariff deadlines looming over markets this summer.

- A correction lower through 1.3563 would be consequential for GBP/USD, and raise the likelihood of a test on the 50-dma support in the near-term. This level has held well and helped define the rally over the course of 2025 - crossing at 1.3477 today. In trend terms, we note that the 50-dma now trades with the largest % premium over the 200-dma since the bounce off lows in 2009. The premium currently sits at ~4.2% vs. the 2009 peak of ~8.2%, mid-Global Financial Crisis.