KRW: USD/KRW Lower On Samsung Earnings Beat, Current Account Back Into Strong Surplus

Friday trade has started with spot USD/KRW on a softer footing. The pair was last near 1379.5, around 0.10% stronger in won terms (we ended extended Thursday trade at 1381.05). Earlier lows were just under 1378. The 1 month USD/KRW is also lower, near 1377.

- Early positive impetus is coming from the stronger local equity tone. The Kospi is up 0.60%, leaving the index at fresh highs back to early 2022. An earlier Samsung profit beat for the tech bellwether is aiding local stock optimism.

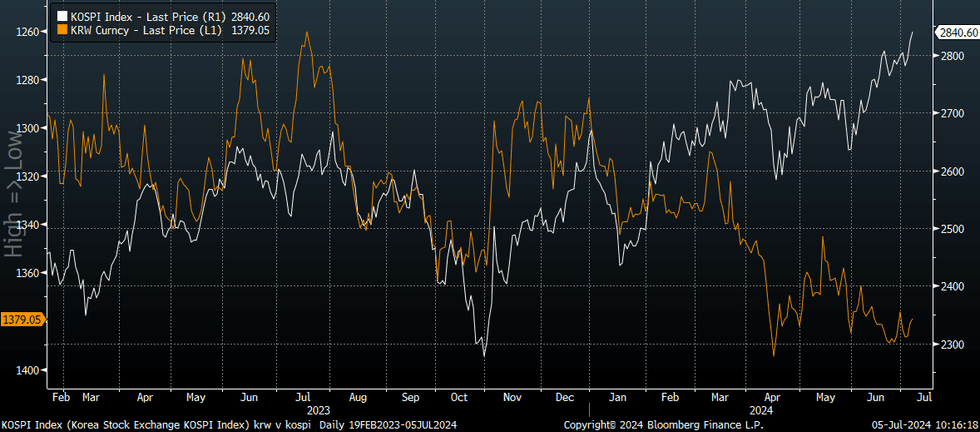

- The chart below plots USD/KRW (which is inverted on the chart), against the Kospi index. While there is decent levels wedge between the two series, a degree of direction correlation remains.

- For spot USD/KRW downside focus is likely to rest on a potential test of 1373.23, which is the 50-day EMA support zone. We are sub the 20-day (near 1381). Highs so far in July rest just under 1392.

- Earlier data showed a strong goods balance surplus for May, while the current account surplus rose to above $8.9bn, fresh highs back to Q3 2021. The sharp swing back into surplus for investment income (after April's dividend related outflows caused a deficit) but a clear positive.

Fig 1: USD/KRW (Inverted) Versus Kospi Equity Index

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Yen Pares Some Of Tuesday's Gain, Aust GDP Later

The USD is firmer against the yen in the early part of Wednesday trade. The BBDXY USD index is close to unchanged at 1252.5.

- USD/JPY has climbed to 155.35/40, up a little over 0.30% versus end NY levels from Tuesday. We are still comfortably sub early Tuesday highs near 156.5 though.

- April wage outcomes delivered a mixed bag, with headline measures firmer than forecast, as negotiated annual wage outcomes started to impact the data. Still, a same base y/y measure was softer at 1.7% y/y (versus 2.1% forecast) (see this link).

- In the cross asset space, the early trend is a tick higher in USD yields, moves aren't much beyond +0.5-1bp at this stage. US equity futures are marginally higher, while regional equity trends are mixed.

- AUD/USD sits down a touch, last near 0.6645. RBA Governor is before parliament this morning, but is sticking to the well-worn line of not ruling anything in or out from a policy standpoint. The RBA will update its forecast profile in August.

- NZD/USD is also down a touch, last near 0.6170. The Q1 terms of trade rose +5.1% (+3.2% was the forecast).

- Coming up we have Q1 Australian GDP, +0.2% q/q is the forecast. Shortly after we get the Caixin Services PMI out of China.

JAPAN DATA: Headline Wages Rise As Negotiated Increases Start To Impact Data

Japan April wage outcomes were firmer than forecast in terms of the headline results. Labor cash earnings rose 2.1% y/y (against a 1.8% forecast and a revised 1.0% March gain). Real earnings were -0.7%y/y, against a -0.9% forecast and -2.1% in March.

- Scheduled pay (not on a same sample basis) rose 2.3% y/y, up from 1.7% in March.

- The Japan authorities will be looking for further improvement in real wage outcomes (trending back above 0%), which is a key policy objective to ensure a recovery in consumption spending and sustainably achieving the 2% inflation target.

- It was a bit more mixed in terms of cash earnings on a same sample base. In y/y terms we rose 1.7%y/y, versus 2.1% forecast and 1.9% prior (which was revised down from 2.2% initially reported). The trend looks a little softer for this metric, but remains above 2023 lows.

- Scheduled full time pay on a same base basis rose 2.1%y/y, in line with expectations and unchanged from March.

- The recently negotiated wage outcomes, where workers secured a +5% wage gain will have impacted today's data. The BoJ suggests around 40% of the annual gain will be reflected in the April data, while 80% will factored in by July (see this BBG link).

JGBS: Futures Stronger Overnight With US Tsys, Cash Earnings Beat Expectations

In post-Tokyo trade, JGB futures are sharply stronger, closing +26 compared to settlement levels.

- April’s Labor and Real Cash Earnings beat expectations printing +2.1% y/y (+1.8% est and a revised +1.0% prior) and -0.7% y/y (-0.9% est and a revised -2.1% prior) respectively.

- Overnight, US tsys rallied for the fourth successive day following softer-than-expected US labour market data. JOLTS Job Openings printed 8.059M vs. 8.350M est and 8.488M prior. The result was the lowest since Feb 2021.

- However, US tsys did finish slightly off session highs amid late position squaring ahead of today’s ADP private employment data risk, a precursor to Friday's headline employment report.

- Meanwhile, Factory Orders were a little stronger (0.7% vs. 0.6% est, 0.8% prior rev), Ex Transportation (0.7% vs. 0.5% est, 0.4% prior rev); Durable Goods Orders in-line/firmer (0.6% vs. 0.7% est), Ex Transportation (0.4% vs. 0.4% est); Cap Goods Orders Non-def Ex Air softer (0.2% vs. 0.3% est).

- US tsys were also supported by oil prices, down around 1% after the 4% tumble on Monday following OPEC+’s plans to loosen its production curbs as early as October.

- US late-year rate cut projections continued to gain vs. late Monday levels: Sep'24 cumulative -19.3bps (-17.2bps), Nov'24 cumulative -27.8bps (-25.3bps), Dec'24 -44.3bps (-40.6bps).

- The local calendar will also see Jibun Bank Composite & Services PMI data today.