FOREX: USD - BBDXY Trying To Build Momentum Above 1190

The BBDXY has had a range today of 1190.35 - 1192.29 in the Asia-Pac session; it is currently trading around 1192. The USD extended its rebound higher having broken above 1187. The market is very bearish the USD so it is interesting to see a bounce like this ahead of some crucial events. Moves like this can sometimes be an early warning, the Supreme court is to sit today and twice next week so the chance of Tariffs being ruled on should be front and centre. The risk of a war or now a limited strike in Iran is something the market will also need to price going into the weekend. On the day, the first resistance is toward 1193 and then the 1195-1200 area where I suspect we could see sellers return initially. Initial support is back toward the 1187-1189 area.

- EUR/USD - Asian range 1.1754-1.1778, Asia is currently trading 1.1760. Price action is becoming a little concerning for the bulls. On the day, the first support is toward 1.1700-1.1730 a sustained move back below the 1.1700 area could signal the potential for a deeper pullback. Focus remains on further Dollar shorts being pared back as the Event risk toward the weekend increases.

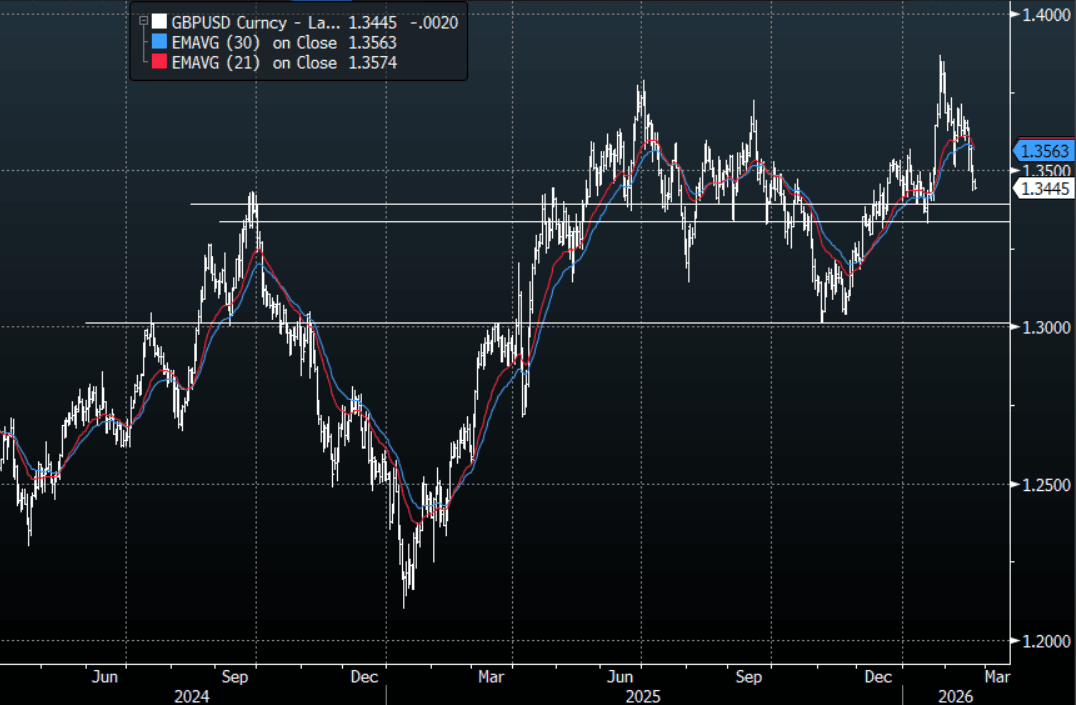

- GBP/USD - Asian range 1.3435-1.3473, Asia is currently dealing around 1.3445. GBP continues to trade under pressure, its headwinds just increasing as the USD rebounds. This 1.3450 area looks important for the bulls and is currently being strongly challenged; a sustained move through here could signal a deeper pullback toward the pivotal 1.3300 area. On the day, look for sellers on a bounce back toward the 1.2500-1.2530 area initially with all eyes on how far this USD bounce can extend.

- Cross asset : SPX +0.20%, Gold $4995, US 10-Year 4.065%, BBDXY 1192, Crude Oil $66.74

- Data/Events : France HCOB France PMI’s, Spain Home sales, EZ HCOB Eurozone PMI’s/Negotiated Wages, Germany PPI/HCOB Germany PMI’s

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Calm Returns After Yesterday's Carnage, New Oct-37 Bond Priced

ACGBs (YM +2.0 & XM +1.0) are modestly richer as relative calm returns to global bonds after yesterday’s carnage.

- (Bloomberg) “Japanese bonds rebound following Tuesday’s rout as Finance Minister Satsuki Katayama calls for calm among market participants. Treasury Secretary Scott Bessent said he had spoken with his Japanese counterpart amid a selloff in Japan’s government bonds that he said had fed through to affect the Treasuries market.”

- Cash US tsys are 1-2bps richer, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +50bps.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 29% for February to 91% by June and 159% by December 2026.

- Tomorrow, the local calendar will see December jobs data. Bloomberg consensus expects November's 21.3k decline to be fully unwound with a 27k rise in employment but that the unemployment rate should tick up 0.1pp to 4.4%.

- The AOFM announced that the issue by syndication of the new 4.75% 21 October 2037 Treasury Bond has been priced at a yield to maturity of 4.87%, with an issue size is $15bn in face value terms. There was a total of $66.97 billion of bids at the final clearing price.

Bloomberg Finance LP

BONDS: NZGBS: Heavy Session Outright & Relatively, Election To Be Held Nov 7

NZGBs closed 3-4bps cheaper, underperforming its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3bps and 6bps higher, respectively.

- Today's move leaves the 2-year and 10-year yields 20bps and 16bps higher, respectively, over the past four days (see chart).

- (Dow Jones) NZ Prime Minister Christopher Luxon said the country will hold elections on Nov. 7. "Continuing the recent tradition of announcing the election date early in the year ensures New Zealanders have certainty," Luxon said in a statement on Wednesday. – via BBG

- NZGBS held by foreigners fell to 59.0% in December from 59.5% in November.

- Swap rates closed 1-3bps higher, with the 2s10s curve steeper.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, but December 2026 assigns 48bps. Notably, market pricing is 10-40bps firmer than levels seen prior to November’s RBNZ decision.

- Tomorrow, the local calendar will see December Card Transactions and November Net Migration tomorrow. Card Transactions rose sharply in November due to discounting and so there could have been some payback last month.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.50% May-35 bond.

Bloomberg Finance LP

EURUSD: Contrarian Viewpoint

The EUR/USD has exploded higher as the market juggles with ways to express a USD short. The USD’s difficulties are mounting and it is very much becoming a consensus view that it trades lower. So it is always good to hear the other side of the trade, Valentin Marinov, head of G10 FX research at CIB has written on why he thinks the EUR/USD trades lower on LinkedIn. Some excerpts below:

- “My thesis is that the EUR has become one of the biggest victims of the latest geopolitical developments, targeting 1.10 in EUR/USD this year: “

- “1️. The US-China standoff has left the European economies very vulnerable to further disruption to the supply of strategic inputs like chips and rare earth minerals.”

- “2. The US trade policies have already hurt the US-EU trade and further saw the Chinese trade surplus with Europe ballooning to levels last seen during the pandemic.”

- “3. Continuing US-Iran tensions could result in a major energy supply disruption that could lead to a negative terms of trade supply shock for Europe. The US-EU spat over Greenland could delay the end of the war in Ukraine, in a blow to business confidence and private investment on the continent.”

- “4. Fiscal stimulus in general and military spending in particular are now seen as key drivers of growth in Europe. Yet, these could also lead to worsening net exports - due to growing imports of weapons and raw materials in particular.”

- “FX is all about flows in the end and the above considerations make me expect less net portfolio inflows into the Eurozone (less repatriation) and less net EUR buying by corporates (worsening net exports).”

- “European investors may want to hedge some of their huge US holdings but this would necessitate aggressive Fed cuts and/ or aggressive further USD losses. Both seem unlikely to me this year.”