UKRAINE: US' Witkoff: Discussions Ongoing, Expect Progress In Weeks Ahead

US Special Envoy Steve Witkoff posts on X: "This week, Ukraine and Russia carried out another prison...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

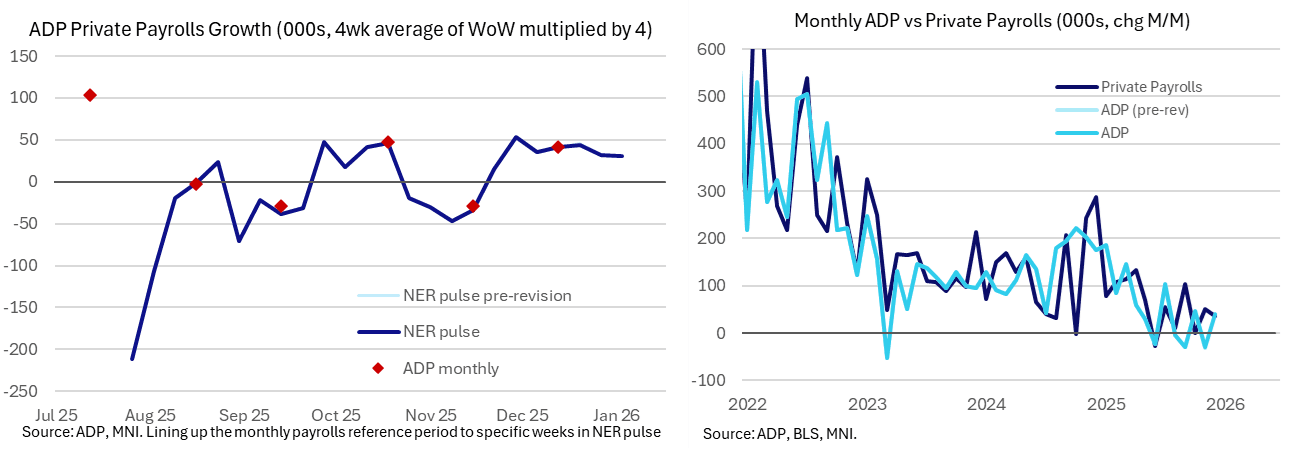

US PREVIEW: ADP Weekly Series Implies Some Downside Risk For January Report

- The government may have re-opened but today sees the key data of the week with the BLS having already postponed JOLTS and Payrolls releases this week (NFPs would have been released in its usual Friday slot before limited shutdown disruption).

- It starts with the ADP private employment report for January at 0815ET.

- Bloomberg consensus looks for a 45k increase in private employment, more optimistic than the 31k equivalent in the ADP’s latest weekly series in the four weeks up to Jan 3. The monthly ADP report’s reference period is the week including the 12th day of the month.

- Unsurprisingly, the breakdown of analyst estimates is skewed lower, with 7 of 27 estimates in the 37-40k range plus 2 at 35k and 2 at 30k.

- The monthly series had been oscillating in recent months between small increases and declines (-3k Aug, -29k Sep, 47k Oct, -29k Nov and 41k Dec) although now appears on track for two modest monthly increases.

- Correlation with BLS private payrolls remains limited, with ADP close in December with just 4k overshoot but a large 79k undershoot in November compared to private payrolls growth of 50k (at least in latest vintages for both).

- Still, the ADP data have provided a useful trend over the past year, moderating in 1H25 before at best limited growth since then (averaged 22k per month through 2H25, but with 104k of the cumulative 131k increase coming in July).

- St Louis Fed's Musalem told an MNI event earlier this month that his economists estimate an overall nonfarm payrolls breakeven pace somewhere between 30-80k per month.

US TSYS: Early SOFR/Treasury Option Roundup: SOFR Puts, Tsys Paired

Overnight SOFR options lean toward downside puts, Tsy options more paired, all on lighter volumes. Underlying futures mildly mixed, inside narrow ranges w/ curves twisting flatter (2s10s -.223 at 69.160). Focus on ADP employment & ISM Services data this morning, Friday's NFP delayed to Monday at the earliest after the short US Gov shutdown ended late Tuesday. Projected rate cut pricing easing slightly vs. late Tuesday levels (*): Mar'26 at -2.6bp, Apr'26 at -6.1bp (-6.4bp), Jun'26 at -17.1bp (-17.9bp), Jul'26 at -24.6bp (-25.9bp).

- SOFR Options:

- 2,000 SFRJ6 96.43 puts, 2.5 ref 96.52

- -10,000 2QH6 96.37/96.50 put spds, 3.0 ref 96.605/0.10%

- 2,000 SFRK6 96.37/96.50/96.62 iron flys, 9.5 ref 96.52

- +2,000 SFRK6 96.43/96.50/96.56/96.62 call condors, 1.5 ref 96.525

- +1,000 SFRH6 96.31/96.37/96.50 2x3x1 broken put flys, 3.5 ref 96.36

- -2,000 SFRH6 96.37 puts, 3.75

- -7,750 SFRM6 96.43 puts, 5.0 ref 96.52

- +2,000 0QZ6 97.25 calls, 10.5 ref 96.65

- Treasury Options:

- +3,500 Wednesday wkly 111/111.5/112 call flys, 23 (exp today)

- 1,000 USH6 111/113 put spds ref 114-20

- 1,600 TYH6 110.75 puts, 5 ref 111-18

- +1,500 TYH6 110 puts, 2 vs. 111-12/0.05%

- -2,000 FVH6 109/110.5 1x2 call spds, 5.5 ref 108-22.75

- +2,000 TYH6 113/114.5 call spds, 3 ref 111-24/0.08%

- +3,000 Wednesday wkly 111.75/112 1x2 call spds, 2 vs. 111-23.5/0.08%

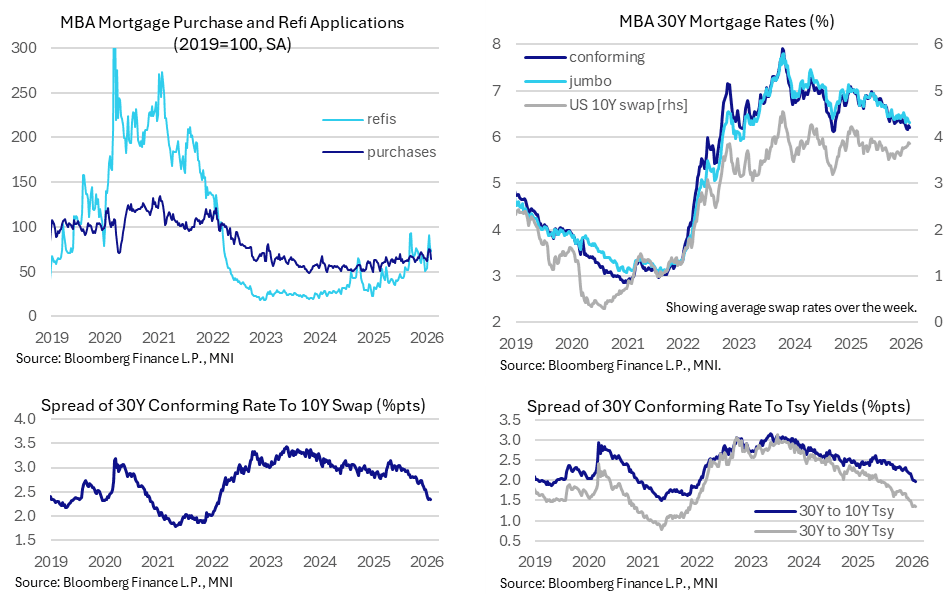

US DATA: New Purchase Mortgage Applications Fell Sharply Last Week

Hopes of higher new purchase mortgage activity as a sign that home sales could be set to pick up was dashed in latest mortgage application data, as new purchase applications saw one of the largest weekly declines in the past ten years.

- Composite mortgage applications fell -8.9% (sa) last week, extending the -8.5% decline in the previous week as they continued to reverse strong increases seen earlier in January to highs since Apr 2022.

- Having last week written on housing activity green shoots implied by a trend increase in new purchase applications, this sharply reversed with a -14.4% drop (largest decline since one week in Mar 2020 and before that 2015) in a reminder of how volatile the data can be.

- Refis meanwhile fell -4.7% after -15.7% following a 69% two-week increase before that.

- Levels relative to 2019 averages: composite at 69%, new purchases at 64% and refis at 73%.

- The 30Y conforming rate fell 3bps to 6.21% to chip away at an 8bp increase in the week prior. The 6.16% in the week to Jan 16 was its lowest since Sep 2024 and before that Sep 2022.

- Mortgage swap spreads reversed about half of the previous week’s widening and are back close to multi-year lows. The 30Y rate to the average 10Y swap rate over the week was 235bp vs a recent low of 233bp (it compares with a peak of 315bp in May in post-tariff disruption, an average 285bp in 1Q25 and 302bp in 2024).

- Compared to August when US Tsy Sec Bessent talked on wanting to see flat or lower mortgage spreads, this swap rate spread has narrowed nearly 60bp, or 43bps to 198bps for the 10Y Treasury yield equivalent.

- Narrowing has been supported by Fannie Mae and Freddie Mac increasing their retained portfolios ahead of a potential IPO, with MBS spreads then tumbling early in January after Trump ordered $200bn in MBS purchases.