FED: US TSY 9Y-10M NOTE AUCTION: HIGH YLD 4.282%; ALLOTMENT 38.89%

* US TSY 9Y-10M NOTE AUCTION: HIGH YLD 4.282%; ALLOTMENT 38.89% * US TSY 9Y-10M NOTE AUCTION: DEALER...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

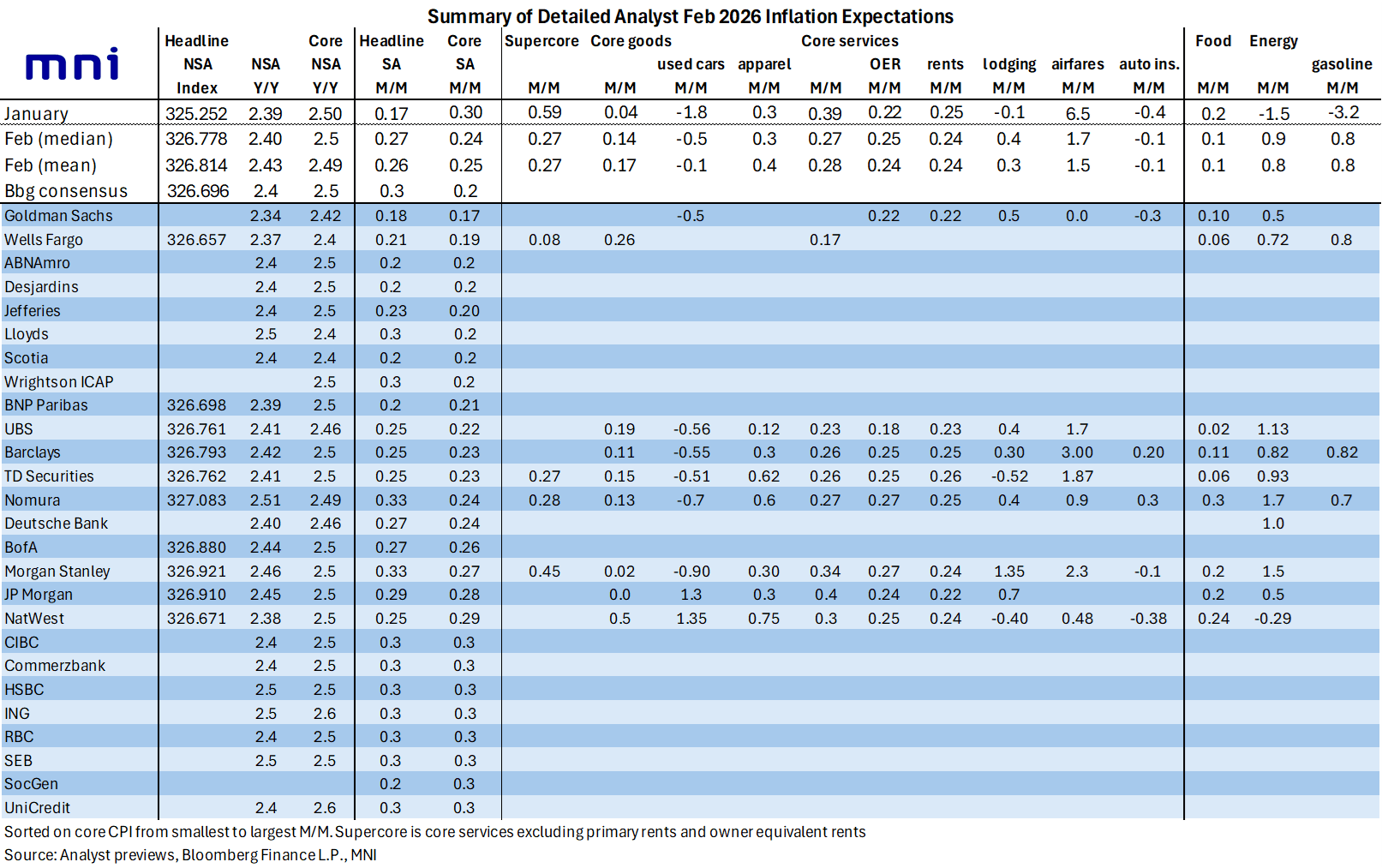

US INFLATION: Expected Sequential Drivers For Core CPI

Analysts expect core CPI M/M moderation in February to primarily come from non-housing services after a strong January increase, which core goods firm (mainly a used cars story) and key rents series firm slightly or are steady:

- On the core goods side, used cars are seen falling by less than the surprisingly large decline of -1.8% M/M in January, with a median of -0.5% and mean of -0.1% (-0.9 to 1.35%).

- Apparel is expected to see another solid 0.3% M/M increase although there’s a reasonably wide range from 0.12% to 0.75%. That would be the third consecutive 0.3% rise since average declines of -0.2% M/M in Oct-Nov in government shutdown disruption.

- Core services are seen moderating, driven by non-housing with supercore roughly expected at 0.3% M/M in a sample of admittedly only four analysts after a strong 0.6% M/M in January.

- This is however concentrated in the non-PCE relevant airfares category, still expected to see a solid increase (median 1.7, mean 1.5) but after a far stronger than expected 6.5% M/M in January.

- Some other non-housing services could see a sequential firming (lodging 0.3/0.4% vs -0.1 in Jan, vehicle insurance -0.1% vs -0.4%) with medical service components are harder one to summarize.

- Rental inflation on the other hand is expected to firm slightly, with an average estimate of 0.25% for OER (range 0.18-0.0.27) after 0.22% and tenants’ rents at 0.24% (range 0.22-0.26) after 0.25%.

FOREX: Risk Recovery Prompts Greenback Turnaround, AUD and NZD Now Outperforming

- Energy prices have reversed substantially from their intra-day highs on Monday, bolstering broader risk sentiment in tandem. Despite the initial price spikes to $120/bbl for crude futures, both Brent and WTI are trading closer to $95/bbl as we approach the APAC crossover. While FX volatility has been relatively contained, initial support for the USD has waned, with risk sensitive currencies now outperforming in late trade.

- AUD and NZD are up close to 0.5% amid the dynamic, while the likes of EUR, JPY and GBP have been steadily edging towards unchanged levels on the session after initial pressure had seen them underperforming early Monday.

- For EURUSD and GBPUSD , lows of 1.1507 and 1.3283 respectively were fairly short lived, with both pairs now pressing back towards 1.16 and 1.34. Sensitivity to Iran developments and energy prices remains a focus point, and potential coordinated measures on stock releases appears to be stoking the tepid optimism. We note that the production/flow outlook in the Gulf region does not suggest the most acute pressure in oil/gas markets is behind us.

- USDJPY reached a 158.90 high overnight, falling just shy the Jan 14 high and bull trigger which stands at 159.45. The pair has since slipped back below 158.30 and eyes a move to 157.78 to similarly bridge the opening gap. Market participants will be monitoring USDJPY closely as we have re-entered levels where prior rate checks from both the BOJ and Fed were reported to have taken place in January.

- Elsewhere, EURCHF moved below 0.9000 for the first time since 2015 with domestic sight deposit data suggesting the SNB has not attempted to curb franc strength last week. 0.8981 has been the printed low so far before the pair has recovered to the 0.9030 region. Should downside in the cross persist, 0.8913 would be a target based on a Fibonacci projection.

- Final Japan GDP readings are due overnight, as well as China trade data. US Weekly ADP highlights a quiet economic calendar Tuesday before Wednesday’s release of US CPI.

SECURITY: Ukraine Peace Talks Postponed At Request Of US - Zelenskyy

Ukrainian President Volodymyr Zelenskyy said in a statement on X that a planned trilateral meeting with Russian and US negotiators has been postponed in light of the war in the Middle East, accusing Russia of trying to "manipulate" the conflict "in favor of their aggression." The statement supports a prevailing view that the war in Iran is likely to significantly decrease the prospect of a diplomatic breakthrough in Ukraine.

- Zelenskyy said, "At the moment, the partners’ priority and all attention are focused on the situation around Iran, and because of this the meeting that had been planned for this week is being postponed at the proposal of the American side.... However, Ukraine is ready for a meeting at any moment, in a format that can help and that will be realistic in terms of ending the war..."

- Zelenskyy continued, "We see that the Russians are now trying to manipulate the situation in the Middle East and the Gulf region in favor of their aggression, and also to effectively turn the Iranian regime’s strikes against its neighbors and American bases into a second front of Russia’s war against Ukraine and, more broadly, against the entire West."

- Responsible Statecraft noted earlier today, "The conflict in Iran probably won’t alter the long-term trajectory of Russia’s special military operation. It will, however, prolong the fighting and make it harder to reach a ceasefire."

- Zelenskyy confirmed yesterday that Ukrainian operatives have been dispatched to the Gulf to advise on counterdrone operations, which Kyiv sees as potentially increasing leverage in future arms tranfers.