FED: US TSY 5Y AUCTION: NON-COMP BIDS $154 MLN FROM $70.000 BLN TOTAL

May-27 16:45

* US TSY 5Y AUCTION: NON-COMP BIDS $154 MLN FROM $70.000 BLN TOTAL...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 13W AUCTION: NON-COMP BIDS $1.802 BLN FROM $89.000 BLN TOTAL

Apr-27 16:45

- US TSY 13W AUCTION: NON-COMP BIDS $1.802 BLN FROM $89.000 BLN TOTAL

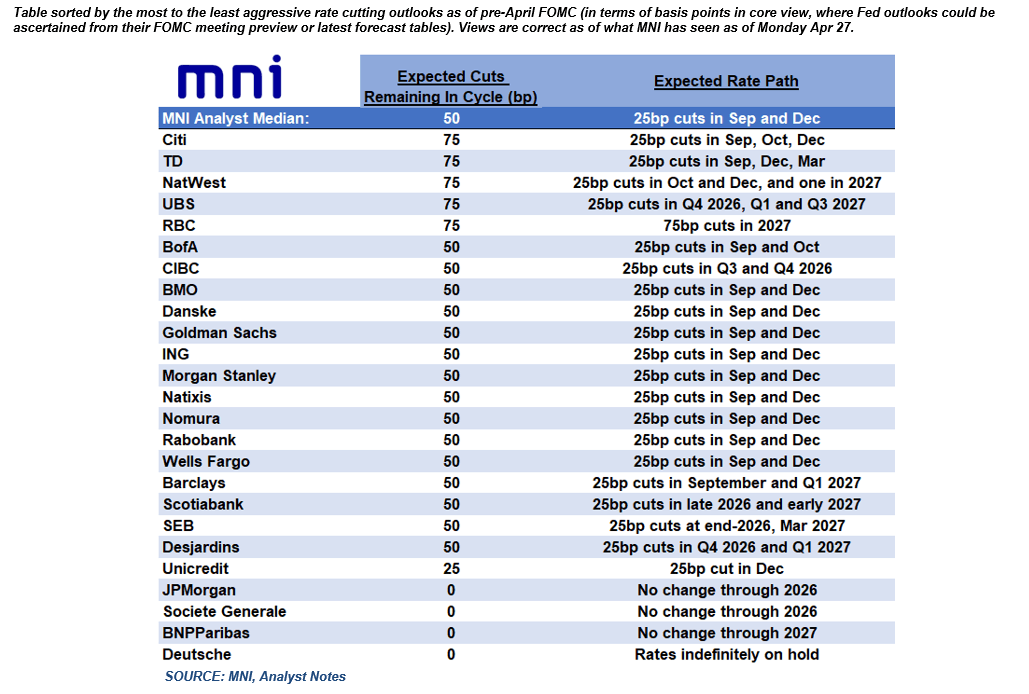

FED: MNI Fed Preview - April 2026 FOMC Analyst Views: Hawkish Guidance Risks

Apr-27 16:37

Our updated Fed preview includes analyst expectations - starting page 34 - Download Full Report Here

All analysts (among 30 previews seen by MNI) expect the FOMC to hold the Fed funds rate at 3.50-3.75% at its April meeting, but opinions differ over possible communications shifts. General consensus is that the risks are that the post-meeting communications lean more hawkish vs expectations as opposed to more dovish, with most focus being on the Statement.

- While the vast majority of analysts expect the FOMC to retain its implied easing bias in the Statement, many see risks that forward guidance (“In considering the extent and timing of additional adjustments to the target range”) shifts hawkishly to a more balanced/two-sided phrasing. A couple (Barclays and Wells Fargo) have a change in guidance as their base case for this meeting.

- Wells Fargo: “The Committee is likely to emphasize optionality in its statement. We expect it to note that higher energy costs are keeping inflation elevated and to soften forward guidance, replacing language around “the extent and timing of additional adjustments” with more open‑ended phrasing that references “future adjustments” to the policy rate.” Barclays: “by removing in the statement the word “additional” when referring to upcoming rate adjustments, the FOMC would signal that it no longer views the next policy rate change as necessarily continuing the recent cutting cycle. This would suggest that it has a more balanced view about its next rate move and would reinforce expectations of policy on hold for the rest of the year.”

- In a variation of these risks, UBS analysts – who see “close to even odds” that the guidance becomes two-sided at this meeting – notes a hawkish incremental shift could revolve around the risks (2nd) paragraph, eg the Iran war “has increased the risks inflation remains elevated.”

- Tweaks are seen possible to the opening paragraph describing economic conditions, with some eyeing economic activity now described as “moderate” vs the prior “solid”, and/or job gains to “modest” vs the prior “low”, though inflation is expected to still be described as “somewhat elevated”.

- Overwhelming consensus is that Gov Miran will dissent again in favor of a 25bp cut, but will not be joined by others.

- Future action: There is consensus among analysts that the Fed has a bit further to go on cuts, though a few see the easing cycle as having already concluded. The median analyst sees 50bp of further cuts, with 25bp easings seen in September and December. Citi is the most dovish on the rate outlook, seeing 75bp of cuts delivered by year-end, though 4 other analysts see that amount of easing by 2027.

MNI EXCLUSIVE: Former Richmond Fed Economist On Monetary Policy Outlook

Apr-27 16:32

MNI interviews former Richmond Fed economist on monetary policy -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Trending Top

May-29 20:10