FED: US TSY 17W BILL AUCTION: HIGH 3.615%(ALLOT 22.85%)

* US TSY 17W BILL AUCTION: HIGH 3.615%(ALLOT 22.85%) * US TSY 17W BILL AUCTION: DEALERS TAKE 44.70% ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: ISM Mfg Prices Paid Fire Warning Shot Before Iran-Driven Energy Impact

[Corrected the line and chart on new orders less inventories]

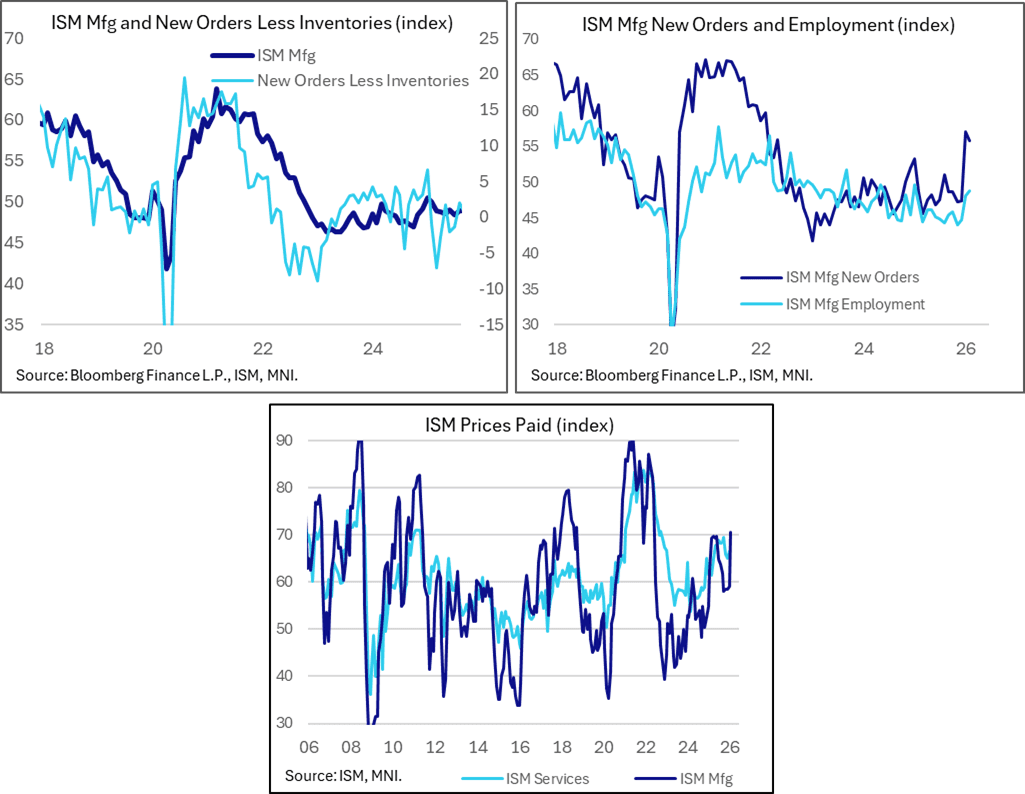

The ISM manufacturing survey held onto more of January's surprise increase than expected as it only inched 0.2pts lower to 52.4 in February after a 4.7pt increase. Other metrics had been mixed, with the S&P Global PMI fully reversing January's increase but the MNI Chicago PMI firming further after a particularly strong increase in January. The most notable aspect of the report was a jump in prices paid to 70.5 (+11.5pts) in Feb for its highest since Jun 2022 in a resurgence of input cost pressure signs after four particularly stable months.

- ISM manufacturing 52.4 (cons 51.5) in February after 52.6 in January.

- Prices paid 70.5 (cons 60.0, 9 responses) in Feb after 59.0 in Jan. The 11.5pt increase is the joint highest since Dec 2020 and leaves the index at its highest since Jun 2022.

- The increase is notable after four months in a particularly narrow range averaged 58.5, with pre-pandemic context being the 49 averaged in 2019 or 61.9 in 2017-19.

- From the press release: "The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods. Higher prices were reported by 45.4 percent of respondents in February, up 16.4 percentage points from January's 29 percent but lower compared to the 49.2 percent in April 2025, which was the highest share since June 2022 (65.2 percent)"

- New orders 55.8 (cons 53.3, 3 responses) in Feb after 57.1 in Jan, which, like the overall index, saw a modest decline after a larger increase back in January, -1.3pts after 9.7pts. The two-month average of 56.5 is the highest since early 2022 having spent most of that time in the contractionary sub-50 region.

- With inventories also increasing from 47.6 to 48.8 (highest since Aug), the more forward-looking metric of new orders less inventories gave back some of January's particularly solid increase to 9.5 and instead eased to 7 to trim some of its implied upside for the near-term.

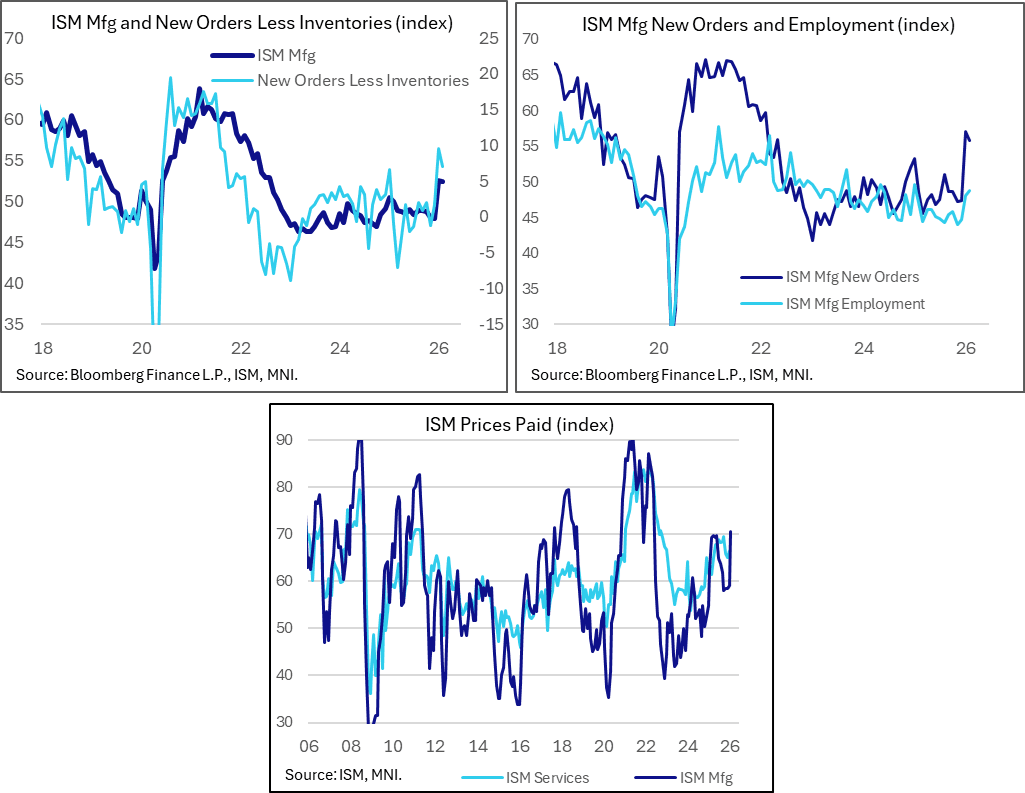

- Employment 48.8 (cons 48.3, 3 responses) in Feb after 48.1 in Jan, a new high since Jan 2025 but still having been below 50 since Sep 2023.

EQUITY OPTIONS: Large Estoxx Put Fly

SX5E (20th Mar) 5800/5700/5600p fly, bought for 5.5 in 12k.

US DATA: ISM Mfg Prices Paid Fire Warning Shot Before Iran-Driven Energy Impact

The ISM manufacturing survey held onto more of January's surprise increase than expected as it only inched 0.2pts lower to 52.4 in February after a 4.7pt increase. Other metrics had been mixed, with the S&P Global PMI fully reversing January's increase but the MNI Chicago PMI firming further after a particularly strong increase in January. The most notable aspect of the report was a jump in prices paid to 70.5 (+11.5pts) in Feb for its highest since Jun 2022 in a resurgence of input cost pressure signs after four particularly stable months.

- ISM manufacturing 52.4 (cons 51.5) in February after 52.6 in January.

- Prices paid 70.5 (cons 60.0, 9 responses) in Feb after 59.0 in Jan. The 11.5pt increase is the joint highest since Dec 2020 and leaves the index at its highest since Jun 2022.

- The increase is notable after four months in a particularly narrow range averaged 58.5, with pre-pandemic context being the 49 averaged in 2019 or 61.9 in 2017-19.

- From the press release: “The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods. Higher prices were reported by 45.4 percent of respondents in February, up 16.4 percentage points from January’s 29 percent but lower compared to the 49.2 percent in April 2025, which was the highest share since June 2022 (65.2 percent)”

- New orders 55.8 (cons 53.3, 3 responses) in Feb after 57.1 in Jan, which, like the overall index, saw a modest decline after a larger increase back in January, -1.3pts after 9.7pts. The two-month average of 56.5 is the highest since early 2022 having spent most of that time in the contractionary sub-50 region.

- With inventories also increasing from 47.6 to 48.8 (highest since Aug), the more forward-looking metric of new orders less inventories gave back some of January’s particularly solid increase to 9.5 and instead eased to 7 whilst pointing to little in the way of upside for the headline index.

- Employment 48.8 (cons 48.3, 3 responses) in Feb after 48.1 in Jan, a new high since Jan 2025 but still having been below 50 since Sep 2023.