FED: US TSY 10Y TIPS AUCTION: NON-COMP BIDS $133 MLN FROM $21.000 BLN TOTAL

Jan-22 17:45

- US TSY 10Y TIPS AUCTION: NON-COMP BIDS $133 MLN FROM $21.000 BLN TOTAL

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 1Y-10M FRN AUCTION: NON-COMP BIDS $13 MLN FROM $28.000 BLN TOTAL

Dec-23 17:45

- US TSY 1Y-10M FRN AUCTION: NON-COMP BIDS $13 MLN FROM $28.000 BLN TOTAL

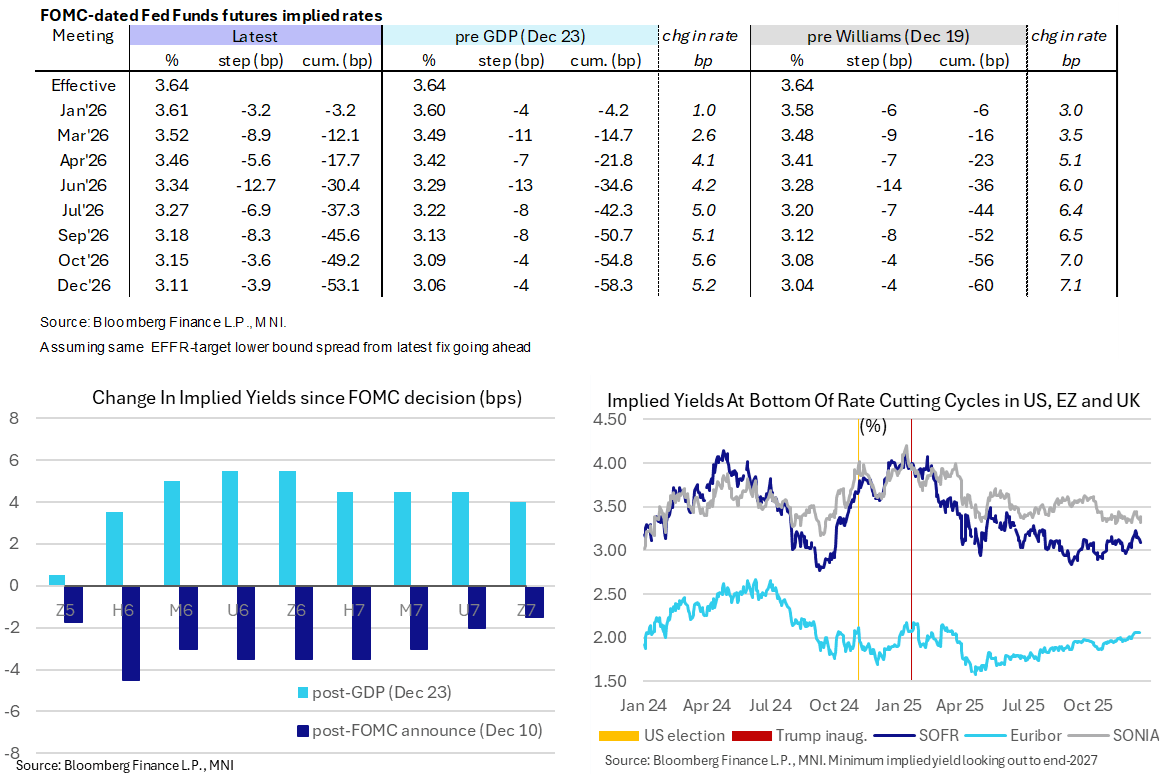

STIR: 2026 Fed Rates Hold Most Of GDP Hawkish Shift

Dec-23 17:43

[A small correction to the earlier post, with the bottom right chart of relative terminal yields now updated]

- US front rates still hold most of their hawkish adjustment on strong Q3 GDP data (real GDP 4.3% vs 3.3% cons, 3.5% GDPNow and PDFP 3.0%), with only a modest paring as the Conference Board’s labor differential deteriorated further in December.

- It goes against longer-dated Treasuries seeing a larger paring of losses, with 10Y yields earlier approaching 4.20% appearing to spur demand.

- Fed Funds futures point to just 3bp of cuts for the Jan 28 FOMC decision, vs 4bp pre-data and 6bp before a more patient sounding Williams on Friday.

- There have been larger hawkish moves for meetings later in 2026, with implied rates 4-5.5bp higher post-0830ET data from April onwards.

- Cumulative cuts from 3.64% effective: 3bp Jan, 12bp Mar, 17.5bp Apr (vs 22bp pre-GDP), 30.5bp Jun, 45.5bp Sep and 53bp Dec.

- It sees a firming up of expectations of the next Fed cut coming in June, the first meeting under a new Fed chair. NEC Hassett's probability has increased a little further on Polymarket today at 63% - he said earlier today that the US is way behind the curve on lowering rates but the comments didn’t draw much immediate reaction.

- SOFR futures are currently as much as 4.5 ticks lower on the day, concentrated in M6-Z6 with losses tapering to -0.02 out in the Z7. The terminal implied yield of 3.165% (Z6) would be its highest close since Dec 10.

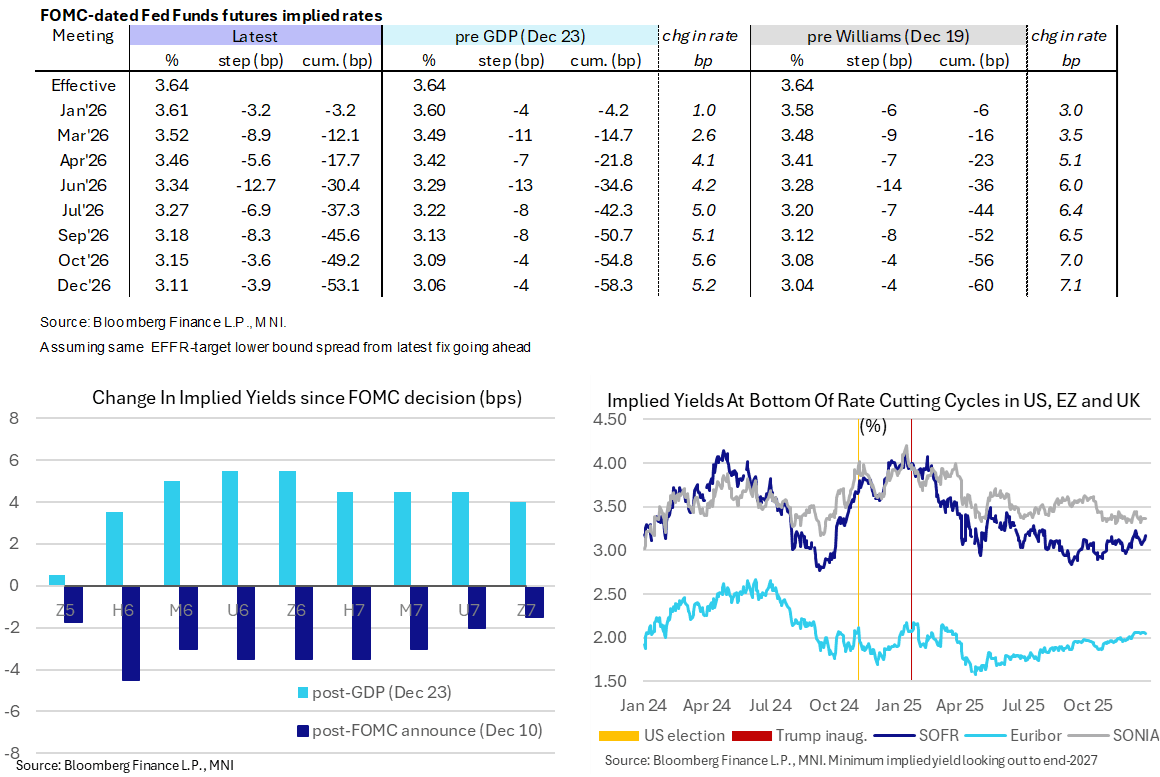

STIR: 2026 Fed Rates Hold Most Of GDP Hawkish Shift

Dec-23 17:36

- US front rates still hold most of their hawkish adjustment on strong Q3 GDP data (real GDP 4.3% vs 3.3% cons, 3.5% GDPNow and PDFP 3.0%), with only a modest paring as the Conference Board’s labor differential deteriorated further in December.

- It goes against longer-dated Treasuries seeing a larger paring of losses, with 10Y yields earlier approaching 4.20% appearing to spur demand.

- Fed Funds futures point to just 3bp of cuts for the Jan 28 FOMC decision, vs 4bp pre-data and 6bp before a more patient sounding Williams on Friday.

- There have been larger hawkish moves for meetings later in 2026, with implied rates 4-5.5bp higher post-0830ET data from April onwards.

- Cumulative cuts from 3.64% effective: 3bp Jan, 12bp Mar, 17.5bp Apr (vs 22bp pre-GDP), 30.5bp Jun, 45.5bp Sep and 53bp Dec.

- It sees a firming up of expectations of the next Fed cut coming in June, the first meeting under a new Fed chair. NEC Hassett's probability has increased a little further on Polymarket today at 63% - he said earlier today that the US is way behind the curve on lowering rates but the comments didn’t draw much immediate reaction.

- SOFR futures are currently as much as 4.5 ticks lower on the day, concentrated in M6-Z6 with losses tapering to -0.02 out in the Z7. The terminal implied yield of 3.165% (Z6) would be its highest close since Dec 10.