MNI US Payrolls Preview: Softer, With Many Moving Parts

Mar-04 16:11By: Chris Harrison

Employment+ 4

Download Full Report Here

Executive Summary

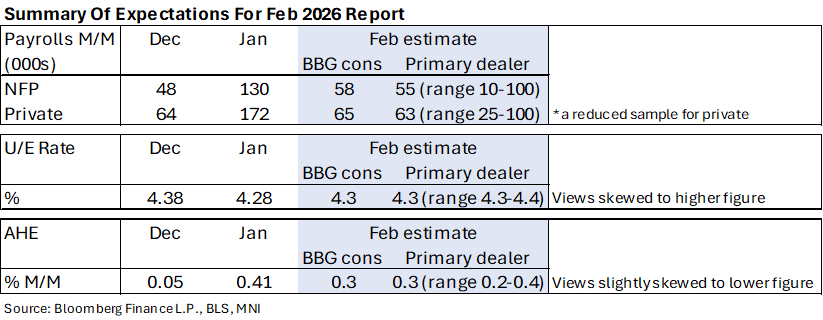

- Nonfarm payrolls are expected to increase 58k in February with gains coming entirely from the private sector, pulling back from a surprisingly strong January.

- One temporary impact known in advance was an additional 31k of striking workers over the payrolls reference period, the highest rise since late 2024. 32k workers will return in the March payrolls count.

- Beyond that, there are questions over the extent to which healthcare jobs pull back after a potential boost from a severe January flu season, with Scotiabank, at the low end of consensus, again eyeing a drag from ACA subsidies expiring at the end of the last year.

- Some cite a colder than usual February as a potential drag after a potential boost in January. Severe winter storms hit in late January, disrupting the actual collection of last month’s household survey.

- On this front, the household survey response rate was its third lowest on record in January, with only the two prior readings lower, increasing scope for volatility.

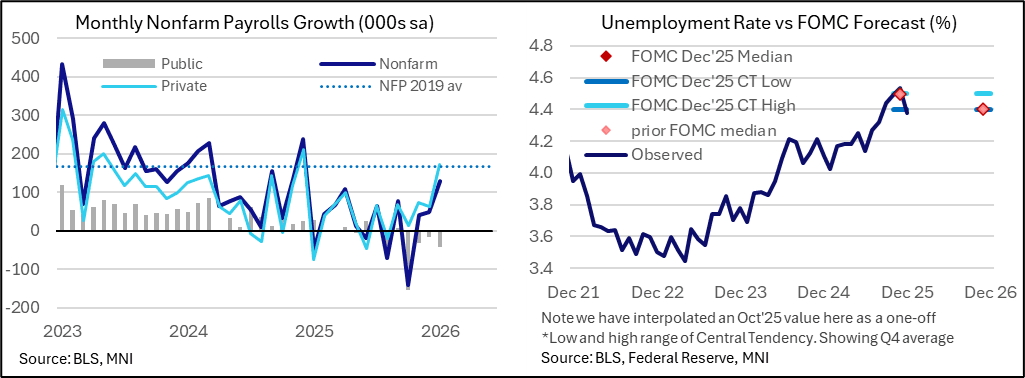

- The unemployment rate, expected to round to 4.3% again after the 4.28% in January was surprisingly its lowest since July, should be assessed with this data quality issue in mind.

- The household survey will also see a delayed population control adjustment, which should markedly lower the level of various metrics such as household employment and labor supply but have limited impact on ratios such as the unemployment rate. Wells Fargo see downside risk on the u/e rate though.

- This will be the last payrolls report before the Mar 17-18 FOMC meeting, with the February CPI report also landing before then on Mar 11. Unusually, the NFP report lands alongside the delayed Jan retail sales report which could complicate reaction to the data.

- These reports are unlikely to alter the Fed’s March decision itself, with just 0.5bp of cuts priced and with a next Fed cut currently not priced until September following a surge in energy prices in the aftermath of US-Israel strikes on Iran. Nevertheless, they can help shape the revised quarterly projections.