OIL: US OIL: October 16 - Americas End of Day Oil Summary: Crude Lower

US OIL: October 16 - Americas End of Day Oil Summary: Crude Lower

WTI crude prices sold off late morning devoid of an outright headline but sustaining weakness following the delayed EIA report amid a crude stock build. Oil markets are under pressure from demand concerns due to US-China trade tensions and as IEA raised its forecast of a record surplus.

- EIA: Crude oil stocks ex SPR +3.52m to 423.8m; Distillate stocks -4.53m to 117.0m; Gasoline stocks -0.27m to 218.8m; Refinery utilization week change -6.7% to 85.7%

- US President Trump suggested that India’s PM Modi pledged to stop buying Russian oil, which would increase demand for non-Russian supplies, but it will take time for India to switch.

- Trump said in a Truth Social post that he had concluded a call with Russian president Putin, saying “great progress was made.” They agreed to a meeting of high level advisors next week followed by the two leaders in Budapest.

- US Treasury Secretary Scott Bessent said that he told Japanese Finance Minister Katsunobu Kato that the US expects Japan to stop importing Russian energy.

- China was the largest buyers of discounted Russian crude in August, according to CREA, followed by India, Turkey and the EU. Trump has said he will now work to persuade China to stop its Russian oil purchases.

- The US and Canada are considering reviving the Keystone XL oil pipeline as part of ongoing trade negotiations, the FT reports.

- Central Europe's non-Russian supply chain faces a significant stress test with TAL works forcing the Czech Republic to tap strategic reserves and highlights the fragility of the new supply route, Kpler said.

- Turkey is set to maintain its imports of Russian Urals crude oil in October at around 280k b/d, unchanged from September, according to LSEG data and market sources cited by Reuters.

- Floating storage of Iranian oil grew after the US sanctioned a key Chinese import terminal last week exacerbating the impacts of weakened demand from teapots, Bloomberg reports.

- A bearish theme in WTI futures remains intact and Tuesday’s fresh cycle low reinforces current conditions. The move down last week resulted in a break of support at $60.40, the Oct 2 low. This highlights an extension of the bearish price sequence of lower lows and lower highs and the move down opens $57.50 next, the May 30 low. On the upside, key resistance is at $66.42, the Sep 29 high. First resistance is at $62.30, the 50-day EMA.

- Cracks have risen amid disruption following product stock draws in the EIA data and amid further Ukrainian strikes on Russian refineries in recent days.

- WTI Nov futures were down 1.4% at $57.46

- WTI Dec futures were down 1.4% at $57.05

- RBOB Nov futures were down 1.2% at $1.81

- ULSD Nov futures were down 1% at $2.15

- US gasoline crack up 0.4$/bbl at 18.66$/bbl

- US ULSD crack up 0.4$/bbl at 32.95/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Macro Developments Since July Support Resumption Of Easing Wednesday (1/2)

Summarizing our Bank of Canada preview out earlier today - link here: the BOC is widely expected to cut its benchmark overnight rate by 25bp to 2.50% on Wednesday September 17. This comes after three consecutive holds, amid a period in which activity and labour market data proved more resilient than expected in the face of the US-Canada trade conflict.

- We’ve heard almost nothing from BOC leadership since the July meeting, save for a speech on central bank independence and flexible inflation targeting delivered by Gov Macklem at a Banco de Mexico conference in August. That leaves us with the data to determine the Bank’s likely course of action – and it’s been almost unambiguous in arguing for the resumption of cuts. In our meeting preview we go through the major data releases since the July BOC meeting.

- July’s rate decision noted that “With still high uncertainty, the Canadian economy showing some resilience, and ongoing pressures on underlying inflation, Governing Council decided to hold the policy interest rate unchanged. We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs related to tariffs and the reconfiguration of trade. If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate.”

- Since then, those criteria for a cut appear to have played out in the data:

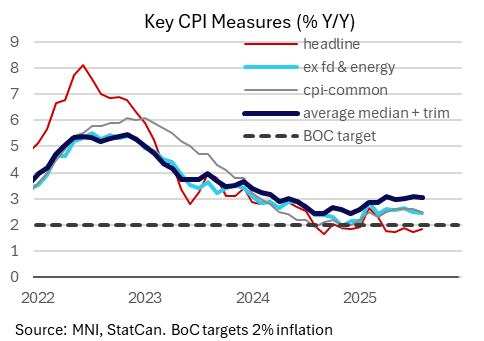

- Inflation Pressures Moderating: August's Canadian CPI data out Tuesday continued July’s theme of steady-to-moderating core inflation after an uncomfortably hot period, and will not present an obstacle to the BOC cutting its benchmark rate Wednesday. This was an important development as the resilience of core inflation was a key component to the BOC’s decision to hold rates through the summer’s trade-related uncertainty. Another factor since that will have helped ease concerns was Canada’s decision to end counter-tariffs on the US at the start of September, taking some of the upside pressure off import prices.

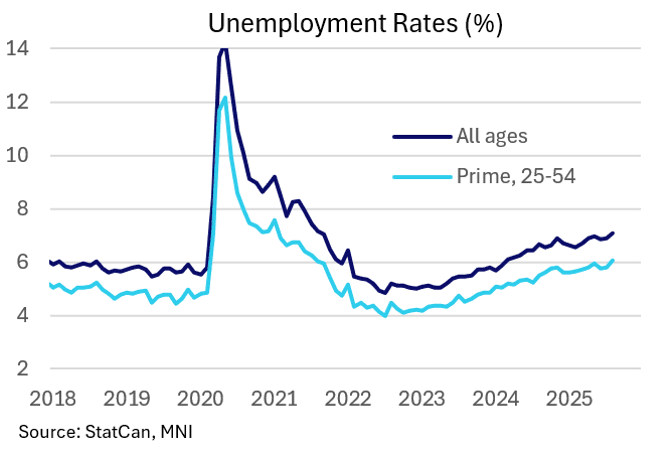

- Jobs Market Softening: The BoC's July meeting deliberations noted "some members expressed concern about the risks of further increases in the unemployment rate and the implications for households if the trade conflict were to escalate or the effects were to spread through the economy more broadly." Data since then will only have increased those concerns. August's Labour Force Survey was unambiguously weak, and in several aspects marked a deterioration from the poor July report, from the fall in employment to the rise in the unemployment rate. Weakness appeared broad-based, including by industry, with continued signs that US-Canada trade tensions are weighing on the labor market. It saw the first back-to-back fall in employment ex-pandemic since 2019, with the unemployment rate rising above 7% (unrounded) since September 2021.

- Growth Recovery Is Limited: The first half of the year concluded on a sour note for growth as Q2 GDP printed -1.6% Q/Q annualized, worst in 5 years, albeit close to the Bank of Canada's "current tariff scenario" of -1.5% and lower than -0.8% consensus expected. That said, the BOC noted in July that in its "current tariff" scenario, "GDP growth picks up to about 1% in the second half of this year as exports stabilize and household spending increases gradually." That's still a plausible outcome, but Bloomberg consensus is now at only 0.2% with a major slowdown in household consumption (0.5% after 4.5%), so at best the recovery looks to be in line with the BOC's previous outlook.

COMMODITIES: Crude Extends Gains, Gold Edges Higher

- Crude has seen support today from a report that Russia may be forced to cut production owing to recent Ukrainian strikes on its energy infrastructure.

- Russia’s oil pipeline monopoly Transneft warned producers they may have to cut output following drone strikes on critical export ports and refineries, Reuters reported, citing three industry sources.

- WTI Oct 25 is up by 2.2% at $64.7/bbl.

- Meanwhile, the market is monitoring sanction developments on Russia, alongside concern about the projected surplus for 2026. The US has said it will follow any new restrictions that the EU imposes against Russia, but only if it stops its own imports of Russian oil.

- The trend condition in WTI futures remains bearish and short-term gains are considered corrective. Initial resistance to watch is $66.03, the Sep 2 high, with key short-term resistance defined at $69.36, the Jul 30 high.

- Initial support is at $61.29, the Aug 13 low and the bear trigger.

- Meanwhile, spot gold is currently up by 0.2% at $3,688/oz, having risen to a fresh all-time high of $3,703 earlier in the session.

- The sharp rally in gold since mid-August has been a combination of Fed independence concerns and expectations for the resumption of Fed easing tomorrow. These tailwinds come alongside a backdrop of persistent central bank demand.

- Gold remains in clear bull cycle, and a clearance of $3,700 would expose Fibonacci projection levels of $3,705.2 (1.382 proj) and $3,744.2 (1.500 proj).

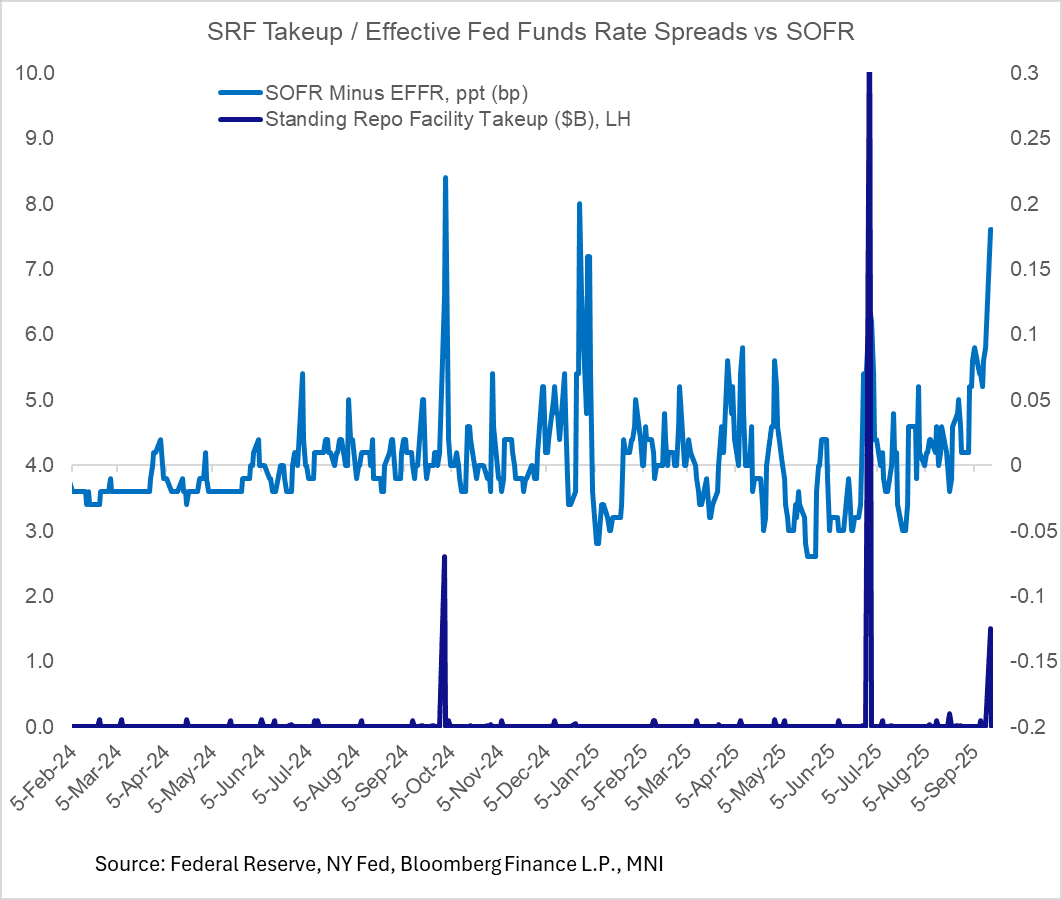

US TSYS/OVERNIGHT REPO: Repo Market Pressure Ahead Of Possible FOMC QT Talks

Secured rates rose sharply Monday, with SOFR rising 9bp to 4.51%. That was the highest rate outright and biggest spread to EFFR of 2025 so far (last exceeded in December 2024).

- It's also notable that we saw the biggest takeup of the Fed's standing repo facility ($1.5B) Monday since end-June (which was a month- and quarter-end). That's reversed today with barely any SRF takeup.

- Monday's pressures were partly a result of an important tax date. It was probably also exaggerated by a net $78B Treasury coupon settlement, which should reverse to some extent Tuesday with just under $50B of net TBill paydowns due.

- Amid the funding market pressures as reserves wind down, however, attention turns to Wednesday's FOMC press conference, with some expectations that Powell could acknowledge that the Committee discussed ending QT in its 2 day meeting starting today (Goldman Sachs sees QT ending at the October meeting).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.51%, 0.09%, $2877B

* Broad General Collateral Rate (BGCR): 4.50%, 0.1%, $1136B

* Tri-Party General Collateral Rate (TGCR): 4.50%, 0.1%, $1097B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $91B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $181B