MNI EXCLUSIVE: BoJ Is Looking For Signs Of Slowing Inflation

The BOJ is looking for signs of slowing inflation amid sluggish private consumption. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: S&P(ESZ5) - Takes A Breath And Stalls Toward 6700 Ahead Of FOMC

The S&P(ESZ5) overnight range was 6661.25 - 6696.75, SPX closed -0.13%, Asia is currently trading around 6666. The S&P move higher finally paused and took a breath with the FOMC approaching, the market seems to be pricing in a goldilocks scenario regarding what the potential upcoming cutting cycle could look like. This morning US futures are trading pretty flat, E-minis(S&P) -0.02%, NQU5 +0.01%. The stock market continues to look way overdone and is in what is supposed to be a difficult seasonal period, but it remains in an uptrend and there does not look to be any imminent signs of a correction yet as it continues to grind higher, dragging an underweight institutional market back in.

- Lance Roberts(RIA) - “With the markets well deviated above the 4-year moving average, with complacency high, and the market overbought on many levels, reversions previously occurred. Will this time be different? It is always possible, but the odds of such an outcome seem spectacularly low.”

- Bloomberg "US Stock Buyback Boom’s End Is Near After Massive Capex. The buyback boom, one of the main supports of the equity rally in recent quarters, is likely on its last legs. Stock repurchases will soon face headwinds from huge capital expenditures and strained free cash flow, which is likely to lead to positive net equity supply. The previous times that has happened – 2000, 2009 and 2020 – have coincided with poor stock-market returns.”

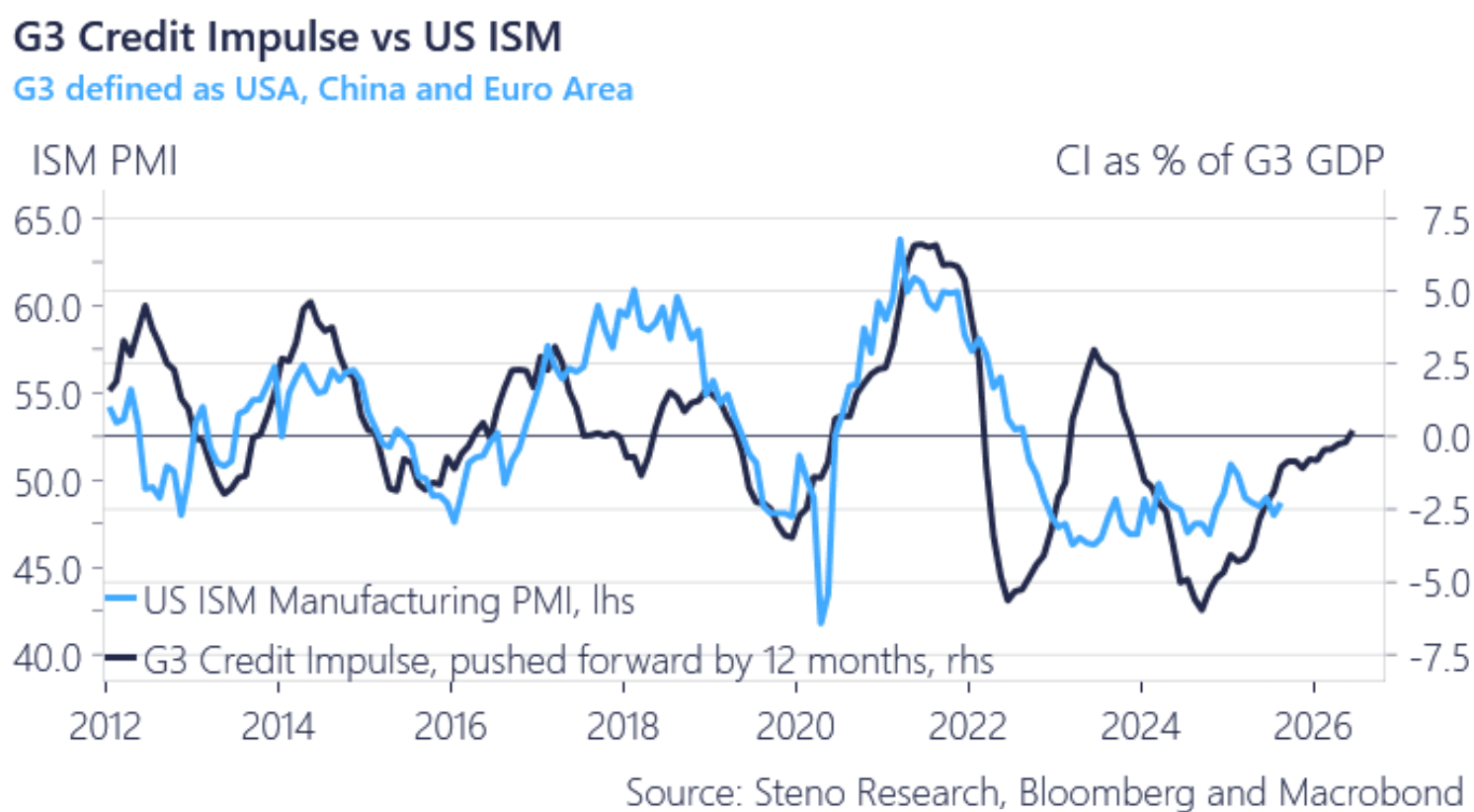

- Andreas Steno Larsen on X: “The credit impulse is turning positive. That is not what you see in a slowdown folks.” See Graph Below

- Holger Zschaepitz on X: "AI is eating the world. The 109 AI stocks in the Goldman Sachs TMT AI Basket are now worth $29.2tn, almost as much as the annual economic output of the US."

Fig 1: Credit Impulse vs US ISM

Source: MNI - Market News/@AndreasSteno

AUSTRALIA: Unchanged Unemployment Rate Expected On Thursday, Analysts Split

August labour market data are released on Thursday and remain a point of focus. Employment is forecast to rise 21k after July’s +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- Bloomberg consensus is expecting job gains to print above both the 3-month and 6-month averages at +7.5k and +13.3k respectively. The data is notoriously volatile.

- Analysts estimates are ranged between +9.5k and +32.5k with most around 15k-30k.

- ANZ is at the upper end forecasting 32.5k new jobs due to vacancies, surveys and orders signalling solid demand for labour. NAB and CBA are around consensus at +25k and +20k respectively. Westpac is below consensus at +15k due to signs of a slowing in job growth as care-related hiring softens.

- Economists are split between the unemployment rate being unchanged at 4.2% (14 analysts on Bloomberg) or rising 0.1pp to 4.3% (11 analysts). This is reflected amongst the big 4 local banks with ANZ and CBA projecting 4.2% and NAB and Westpac 4.3%. It is currently 0.8pp above the October 2022 trough.

- The participation rate is expected to be steady at 67.0%.

LNG: Gas Prices Higher On Demand Outlook

Natural gas took direction from oil on Tuesday with prices trending higher driven by concerns that geopolitical issues could impact global fossil fuel supplies. European prices rose 0.8% to EUR 32.42, close to the intraday high, after a low of EUR 31.62 early in the session. They are now 2.5% higher this month.

- European gas fell on Monday driven by forecasts for a significant increase in wind-generated power but that is now expected to moderate towards average. Bloomberg reported that 60% of British power yesterday morning was from wind.

- After numerous Ukrainian attacks on Russian oil infrastructure over the weekend, it struck another refinery early in the week. US-EU talks continue on options to reduce the revenue Russia earns from energy exports. Restrictions on companies in India and China involved in oil trade with Russia were delayed by the EU.

- US gas rose 2.4% to $3.117 to be up 4% in September and 6% this week. It has found support from expectations that there will be increased cooling demand in the second half of September as higher temperatures are projected. There are also thoughts now that this warmer weather may mean a delay to the start of heating demand.

- There is also work on a Permian basin pipeline reducing flows, according to EBW AnalyticsGroup.

- Asian LNG demand looks to be picking up as countries take advantage of favourable prices.