OIL: US OIL: November 14 - Americas End of Day Oil Summary: Crude Higher

US OIL: November 14 - Americas End of Day Oil Summary: Crude Higher

WTI Crude sustained firm gains today, despite late news that the US would allow Lukoil transactions outside of Russia, after regaining ground earlier. Support follows Ukraine’s overnight drone strikes on the Russian oil-loading port of Novorossiysk.

- US allows some Lukoil transactions outside of Russia according to Bloomberg

- US total rig count 549, Baker Hughes said, with the US oil rig count up 3 to 417.

- Reuters reported that CPC had reopened, having only been closed as a precaution due to the state of emergency in Novorossiysk.

- Ukraine drone attacks caused a fire at the Sheskharis oil terminal at Russia’s Black Sea port of Novorossiysk overnight. The blaze has been put out but the damage is unknown. The terminal remains shut according to Reuters.

- Drone debris damaged a reservoir and pier belonging to Chernomortransneft, the Nutep container terminal, and an oil depot at the Sheskharis transshipment complex: Novorossiys’s Mayor.

- Lukoil is holding negotiations on the sale of its international assets with several potential buyers: Interfax.

- QatarEnergy has raised the price of al-Shaheen for January: Reuters.

- Oil demand will grow to 113m b/d in 2040, up from 103.5m b/d in 2024, longer than expected Goldman Sachs forecasts.

- A sharp reduction in Russian exports could push Brent above $85/b, Barclays said.

- Iran seized a Marshall Islands-flagged tanker transiting the Straits of Hormuz Nov. 14.

- Iran’s dark tanker fleet is operating near full capacity, Vortexa said.

- Diesel cracks resumed their uptick today as disruption at Russia’s Black Sea Novorossiysk port adds to ongoing supply concerns. Gasoline crack spreads also regained earlier losses to trade higher today with the US Thanksgiving holiday less than two weeks away.

- WTI Dec futures were up 2.4% at $60.09

- WTI Jan futures were up 2.2% at $59.93

- RBOB Dec futures were up 2.6% at $2.01

- ULSD Dec futures were up 2.7% at $2.53

- US gasoline crack up 0.8$/bbl at 24.35$/bbl

- US ULSD crack up 1.3$/bbl at 46.24/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Hammer Candle Highlights Possible Reversal

- RES 4: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6660/6707 High Sep 18 / 17 and a bull trigger

- RES 2: 0.6629 High Sep 30 & Oct 01 and key short-term resistance

- RES 1: 0.6556 50-day EMA

- PRICE: 0.6519 @ 16:00 BST Oct 15

- SUP 1: 0.6440 Low Oct 14

- SUP 2: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6357 Low May 12

A bear theme in AUDUSD remains intact. However, yesterday’s recovery highlights a possible reversal pattern - a hammer candle formation. If correct, it signals the end of the bear leg that started Sep 17. Note too that MA studies have remained in a bull-mode position during the latest bear leg, and this highlights a dominant M/T uptrend. Initial resistance is 0.6556, the 50-day EMA. A resumption of weakness would open 0.6415, the Aug 21 and 22 low.

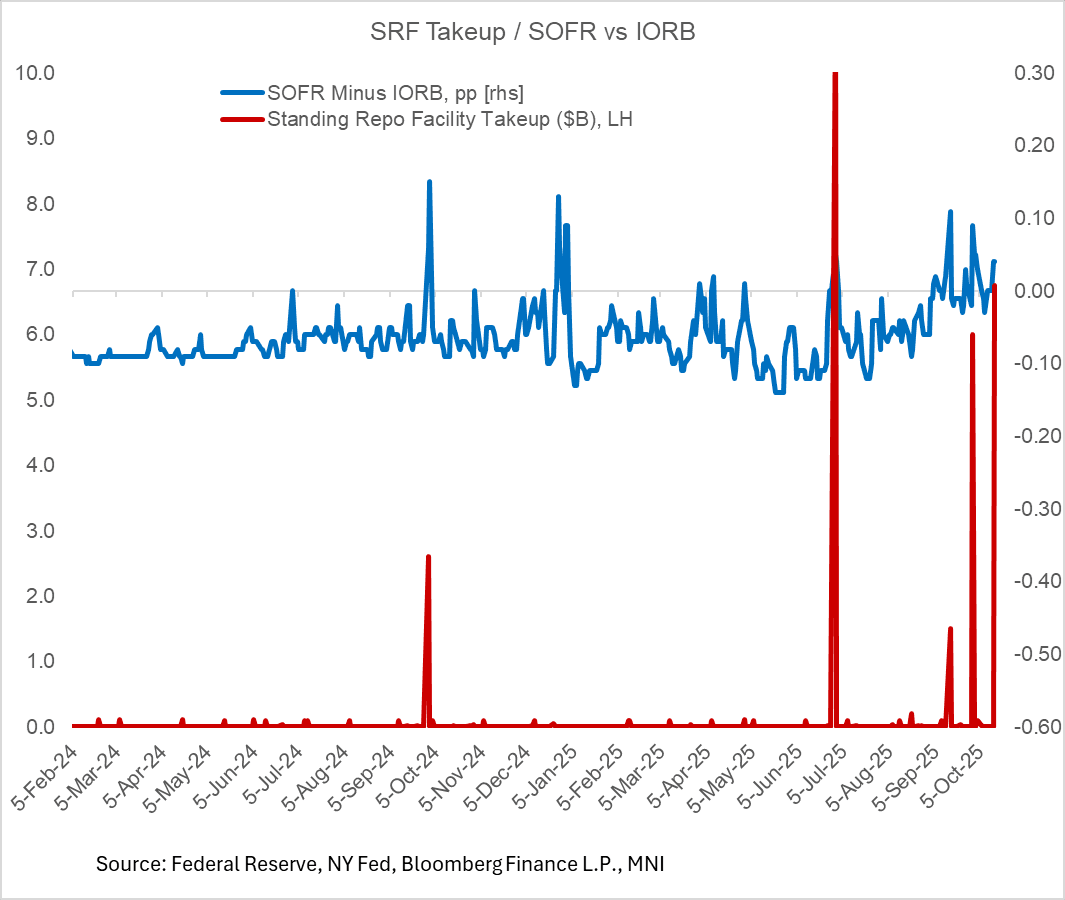

US TSYS/OVERNIGHT REPO: Fed Standing Repo Takeup Jump Part Of Wider Pressure

The Fed's Standing Repo Facility (SRF) saw its highest takeup this morning since the quarter-/month-end date of June 30.

- The $6.8B usage of the facility comes as SOFR printed 4bp above IORB (4.19% vs 4.15%) yesterday, with a variety of other indicators suggesting mounting funding market pressures. It compares with the $6.0B takeup at the last month-/quarter end date of September, and is the 2rd-highest takeup (after June 30) since Q2 2020. (The SRF was made permanent in 2021).

- Even so this rise should be put into perspective; takeup was many times larger in 2019 during a previous episode of funding pressures that led to the Fed restarting asset purchases. And per the September meeting minutes, "a few participants noted that the SRF would help keep the federal funds rate within its target range and ensure that temporary pressures in money markets would not disrupt the ongoing reduction in Federal Reserve securities holdings to the level needed to implement monetary policy efficiently and effectively in the Committee’s ample-reserves regime"

- Even so, there's a variety of factors contributing to the rise in takeup. Based on various measures we (and the Fed) look at, some funding market pressure has been building up for a few weeks now as reserves fell below $3T - the pressures are still on the light side but enough to get the Fed thinking about slowing runoff (as evidenced by Chair Powell's speech Tuesday in which he suggested QT could end in the coming months).

- Today's pressures may be related to a tax date and decently large coupon settlements (just under $40B, sandwiched between $52B in bills combined over Tuesday and Thursday) removing reserves from the system.

- SOFR was 4.19% Tuesday so it wouldn't be surprising if it weren't far below the 4.25% SRF rate today, making it a closer-than-usual tradeoff.

BONDS: EGBs-GILTS CASH CLOSE: OATs' Continued Gains Buoys Broader Space

European curves continued to bull flatten Wednesday, with French outperformance continuing.

- Longer-end yields gapped lower on the open and continued lower for most of the session, buoyed by comments after Tuesday's cash close by Fed Chair Powell pointing to a possible end to QT in coming months, as well as a perception of easing French political risks.

- In a light session for data (including some final national-level Eurozone September inflation readings), Euro area industrial production shrank less than expected in August but all four of the largest countries saw declines.

- On the day, Gilts twist flattened with Bunds bull flattening. UK 2s10s had their flattest close since early July; for Germany, March.

- Periphery/semi-core EGB spreads closed tighter, led by Italy and France.

- Thursday's scheduled highlight is UK monthly activity data, while we get multiple central bank speakers including BOE's Mann and Greene, and ECB''s Wunsch, Kocher, Lane, and Lagarde. On the French political front we also get no-confidence motions on the government.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 1.3bps at 1.922%, 5-Yr is down 3.6bps at 2.166%, 10-Yr is down 3.9bps at 2.571%, and 30-Yr is down 4.6bps at 3.146%.

- UK: The 2-Yr yield is up 0.1bps at 3.902%, 5-Yr is down 3.7bps at 4.001%, 10-Yr is down 4.7bps at 4.543%, and 30-Yr is down 5.1bps at 5.343%.

- Italian BTP spread up 2.6bps at 80.9bps / French OAT down 2.3bps at 77.5bps