LOOK AHEAD: US Macro Week Ahead: Nonfarm Payrolls On Friday

May-01 20:00

* Consensus for Friday's nonfarm payrolls report currently eyes a somewhat resilient 60k monthly i...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Market Static/Leaning Toward Risk-On Ahead Trump Address on War Tonight

Apr-01 19:50

- Treasuries look to finish near session lows after trading stronger late overnight. Focus on Pres Trumps address to nation tonight re: Iran war.

- Recent pivot in messaging suggests the White House is looking to build an off-ramp to the war. It is unclear what Trump intends to say, but evidence is mounting that Trump is edging towards declaring a military victory that could lay the groundwork for a demobilisation of US forces.

- Limited market reacting to the "letter to Americans" from Iranian President Pezeshkian: Iran "NEVER PURSUED 'AGGRESSION' .. HARBORS NO ENMITY TOWARD ORDINARY AMERICANS .. TELLS AMERICANS TO LOOK PAST RHETORIC" Bbg. Full text is here

- March's ISM Manufacturing Report posted another solid set of activity readings, but came with another indication of soaring inflation. The data and anecdotal commentary provide some evidence that the conflict in the Middle East is already hampering supply chains and pushing up input costs.

- TYM6 currently -4.5 at 110-29 vs. 110-27.5 low / 111-14.5 high. The bear trigger is 109-24, the Mar 27 low. A break would resume the downtrend.

- Cross asset update: Bloomberg US$ index weaker (BBDXY -3.32 at 1212.13); equities near highs: SPX emini +.91%, Nasdaq +1.3%, DJIA +0.7%, WTI crude -1.87% below $100/bbl.

- LOOK AHEAD: Thursday Data Calendar: Wkly Claims, Trade Bal, Imp/Exp, Fed Speak

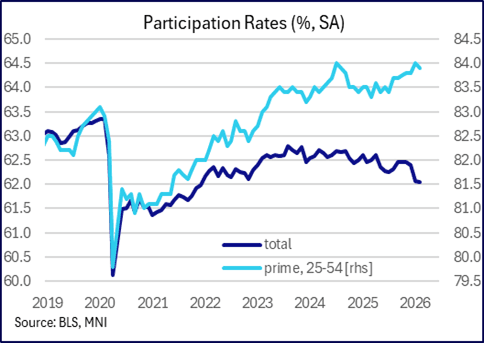

US LABOR MARKET: Participation and Underemployment Rates Also Watched

Apr-01 19:41

- This month’s household survey should be a somewhat cleaner read than February, which owing to a delay stemming from last year’s government shutdown unusually included a revision for the population control back on January levels.

- Indeed, understanding February dynamics depends largely on figuring in the annual revisions, though overall February's household report looked largely weak.

- We’ll watch participation rates, with the overall rate expected to edge up to 62.1% from 62.05% in Feb, after a marked downward revision to 62.1% back in January from the 62.5% first reported (due to revised demographics) which meant the lowest since late 2021 as opposed to a nine-month high.

- Elsewhere, we watch the underemployment rate which puzzled in February as it fell for a third consecutive month to 7.9% for its lowest since Jul 2025, most recently helped by the largest drop in those working part-time for economic reasons since mid-2022.

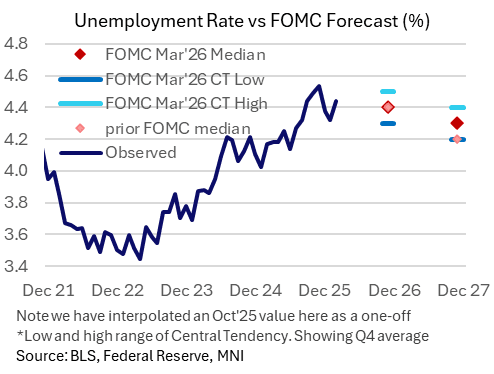

US LABOR MARKET: Unemployment Rate Seen Continuing Trend Stabilization

Apr-01 19:31

- The unemployment rate meanwhile is expected to hold at 4.4% in March although with a skew towards 4.5%, unsurprising considering it was 4.44% in February.

- Average the mixed January and February reports and the 4.38% sits between the heavily caveated 4.47% averaged in Q4 (government shutdown disruption) and 4.34% in Q3.

- That broad stability, both realized and expected, continues to defy a scenario that the most dovish FOMC members had envisaged back in the December SEP (seven members pencilled in 4.6-4.7% in 4Q25).

- More timely forecasts from the updated March SEP continue to show little additional deterioration expected to end-2026 however, with a median FOMC member pencilling in 4.4% in 4Q26. Thirteen of nineteen members eye 4.4-4.5%, whilst four see 4.2-4.3% and two 4.6-4.7%.

Trending Top

May-01 21:26