LOOK AHEAD: US Macro Week Ahead: ISM Mfg and Services Reports Before Payrolls

May-29 20:00

The May nonfarm payrolls report follows two surprisingly strong reports for March and April in devel...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

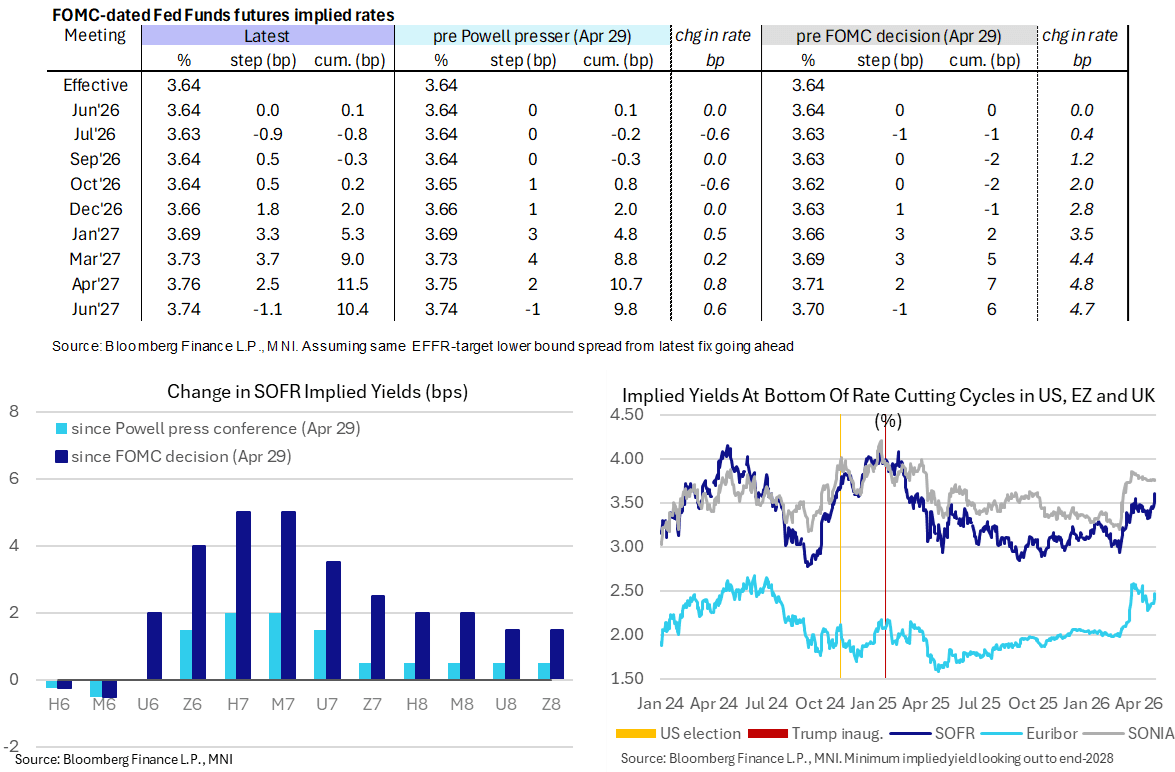

STIR: Fed 1H27 Hiking Bias Slightly Extends With Powell Presser

Apr-29 19:41

- US rates have seen a slight hawkish extension with Powell’s final press conference, again led by 1H27 contracts, but it's small compared to the day’s shift on surging crude oil futures (WTI 1st +7.5%).

- SFRM7 is -0.02 since Powell took to the podium, -0.05 since the decision itself and -0.155 on the day.

- Currently at 96.200 off an earlier low of 96.175, SFRM7 came close to the recent low of 96.165 early on Mar 27 having last been lower in Feb 2025.

- The terminal implied yield of 3.605% (H8, +9bp) is on track for comfortably its highest close of the Middle East conflict. It has seen a range of 3.075% (Mar 2) - 3.55% (Mar 26) for closes since first US-Israel strikes on Iran on Feb 28.

- FF cumulative moves from 3.64% effective: 0bp Jun, -1bp Jul, -0.5bp Sep, 0bp Oct, +2bp Dec before +9bp Mar 2027 and +10.5bp Jun 2027.

FED: Rough Transcript of Fed Chair Powell's Press Conference

Apr-29 19:36

See link below for a rough transcript of Fed Chair Jerome Powell's April 29 press conference (PDF):

FOMC Press Conference April 2026

BOC: Analysts Still Overwhelmingly See No Hikes In 2026

Apr-29 19:32

TD appears to have been alone among Canadian analysts in changing their BOC outlook following April's meeting (reducing its end-2027 overnight rate view to 2.75% from 3.00%). Other reactions alongside expected BOC rate paths, in alphabetical order of institutions (which, excluding TD, also happens to be from most dovish to most hawkish):

- BMO (Hold through 2026 and 2027): "There remains a huge number of unknowns for the outlook, with oil and trade looming largest. Until we get more clarity, the BoC is likely going to stay on hold. However, it is apparent that policymakers want to push back on any second round inflation effects, so CPI data over the next few months will be watched closely if energy prices don't retreat."

- CIBC (Hold through 2026, 50bp hikes in 2027): "The Bank of Canada will be standing on guard for thee, but that’s not just against elevated inflation, but also sluggish growth and excessive slack, a two-way risk that is keeping interest rates frozen in place...We don't have reason to alter our call for the Bank of Canada to be on hold this year..Our core inflation outlook is sufficiently benign to make a rate hike unwise. We're a few ticks faster than the Bank in our outlook for 2027 growth, enough to envisage a couple of quarter point hikes next year as the output gap narrows, but that's contingent on seeing USMCA talks prevent further trade barriers and provide some small relief from existing sectoral duties imposed on Canada."

- Desjardins (Hold through 2026, 50bp hikes in H1 2027): "Given the two-sided risks to the inflation outlook, the Bank of Canada appears comfortable leaving rates on hold, unless oil prices remain higher for longer. We remain of the view that the Bank of Canada will keep the policy rate unchanged for the rest of the year."

- National (Hold through 2026, 50bp hikes in 2027): "Their growth path is consistent with eventual rate hikes, though the timing remains uncertain. The current OIS-implied rate path, implying a hike or two by year-end, is far more realistic than the >75 bps of 2026 tightening that were (briefly) priced last month. But while a Q4 hike is plausible, we continue to expect the Bank to wait until 2027 before starting to move back toward neutral (i.e., 2.75%). Overall, this was a largely as expected rate decision. The Bank will remain comfortably on the sidelines for now, but their base case outlook is consistent with eventual hikes, not cuts."

- RBC (Hold through 2026, 100bp hikes in 2027): "Overall, both the BoC and we expect moderate economic growth this year to lead to a gradual absorption of economic slack over time. We continue to expect no change in the overnight rate in 2026 before it edges higher in 2027, alongside a narrowing output gap and downdrift in the unemployment rate."

- Scotiabank (50bp hikes in Q3, 25bp hike in Q4 going into BOC meeting): "The post-communications market reactions are mixing market pricing of oil impacts and BoC communications while treating the latter as stale on arrival. July is now 50–50 priced for a BoC hike. June is not a base case at this point, but is underpriced in my opinion; six more weeks of this and it will be harder for Macklem & Co to sit tight and the BoC doesn’t have to have an MPR to move. Volatile markets are swinging between pricing about 55–70bps of our 75bps of forecast hikes by year-end. Our 2026H2 hike forecast that we’ve had since November and that we added to in March has made money for clients who listened."

Trending Top

May-29 20:10