LOOK AHEAD: US Macro Week Ahead: Backloaded Notable Data Releases

The FOMC decision will command the most attention but there are some notable data releases skewed to...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Approaching Resistance

- RES 4: 186.87 High Jan 23 and a key M/T resistance

- RES 3: 186.36 High Feb 9

- RES 2: 185.05 76.4% retracement of the Feb 9 - 12 bear leg

- RES 1: 184.77 High Feb 25 and a key resistance

- PRICE: 184.36 @ 17:43 GMT Mar 25

- SUP 1: 183.22/181.87 50-day EMA / Low Mar 16

- SUP 2: 180.81 Low Feb 12

- SUP 3: 180.10 Low Dec 5 ‘25

- SUP 4: 179.30 23.6% of the Feb 28 ‘25 - Jan 23 bull cycle

EURJPY continues to recover from its mid-February low. The cross recently breached support at the base of a bull channel - currently at 183.94 - drawn from the Feb 28 ‘25 low. The break highlights a stronger reversal and if correct, opens the next key support at 181.81, the Feb 12 low. Resistance to watch is 184.77, the Feb 25 high. A clear break of this level would instead signal a reversal and the start of a bull cycle inside the channel.

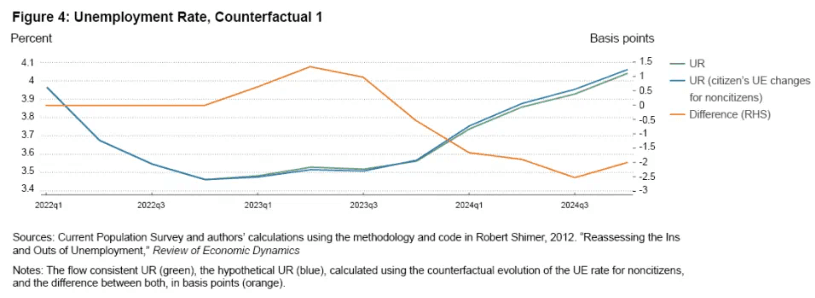

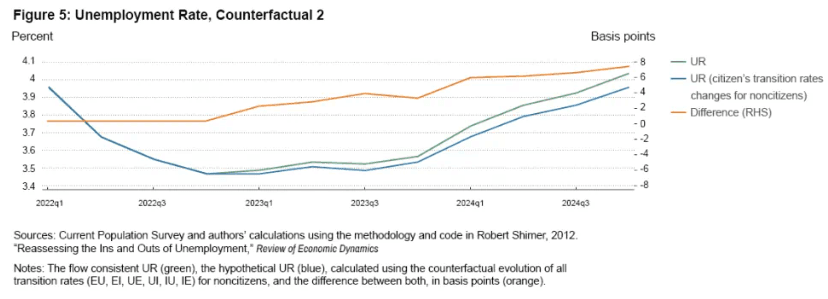

US LABOR MARKET: Little Immigration Impact On Higher U/E Rate In 2023-24

- Seen in light of the significant clampdown on immigration flows in 2025, Cleveland Fed research staff “find no evidence that the higher share of noncitizens in the labor market contributed to the rise in the unemployment rate during 2023 and 2024.”

- “First, noncitizens may have systematically lower job-finding rates than citizens. Second, during slowdowns, noncitizens’ job-finding and other transition rates may deteriorate more rapidly and extensively than those of US citizens.”

- “In other words, the increase in the unemployment rate that we have seen over the last couple of years appears mainly to be the result of macroeconomic conditions affecting all individuals and is not explained by an increased share of noncitizens in the US labor market in the last few years.”

- See the full report, here.

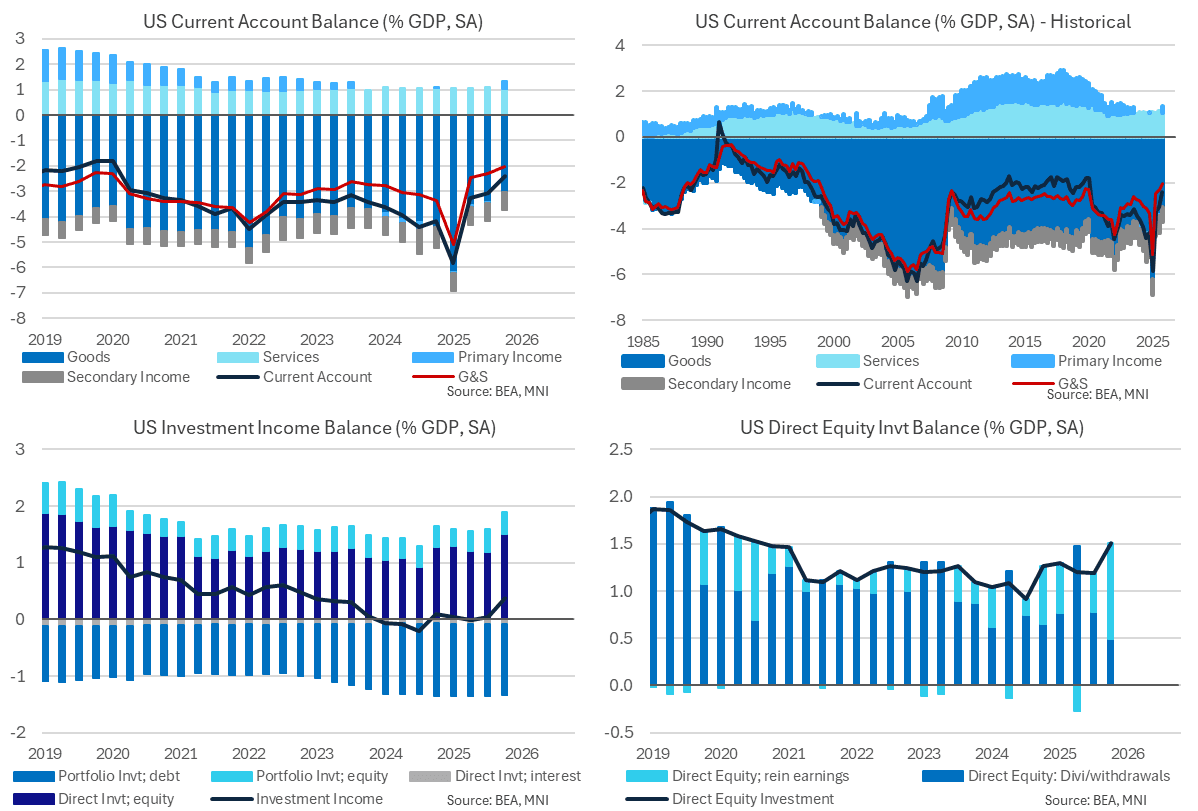

US DATA: Narrowing Current Account Deficit Owes To Reinvested Earnings Jump

The US current account deficit narrowed sharply in Q4 2026, with the $190.7B smaller than the $208.5B expected and the $239.1B in Q3 (upwardly rev from $226.4B). It was the smallest C/A deficit since Q1 2021 in nominal terms, and the smallest in % of GDP terms (2.4%) since 2020.

- A major component in the narrowing was the goods and services deficit dipping to the smallest since Q2 2020, at $160B ($179B prior).

- But even more important from a sequential perspective was the primary income account: it posted a $23.9B surplus, a reversal from -$2.5B prior for the highest since Q4 2022 (it had been in deficit for 7 of the prior 8 quarters).

- In turn this was entirely due to soaring net direct equity investment: $119.6B, up from $92.4B prior, for the highest going back to at least the late 1990s, and driven by reinvested earnings. That was worth 1.5% of GDP in the quarter, largely offsetting the 2.0% of GDP goods and services trade deficit.

- For the year, the current account deficit fell by $69.3B to $1.12T, falling to 3.6% of GDP from 4.0% in 2024. It was a volatile year though, with Q1 seeing pre-tariff volatility as gold and pharmaceutical imports jumped, which then largely reversed in 2H.

- Coming into 2026, consensus is for a smaller current account deficit for the full year (3.3% of GDP).