CANADA DATA: Unexpected August GDP Contraction Roughly Neutral For BOC Outlook

Oct-31 15:32

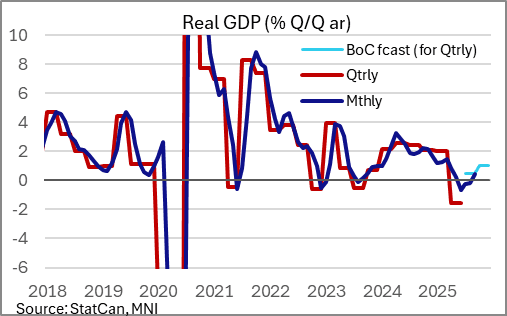

Canadian GDP by industry unexpectedly posted a sharp contraction in August, falling 0.3% (0.0% StatCan advance estimate/consensus). There was some modest mitigation in the report though as July's data was revised up (0.31% M/M unrounded from 0.24%), and September's advance estimate came in at +0.1%.

- But August's reading marked the 4th M/M contraction in 5 months and leaves the level of real GDP (by industry) below January.

- And the 3M/3M annualized rate has now been negative for 3 consecutive months (-0.2% in August), including -0.65% in June which translated to -1.6% for overall GDP in Q2.

- A 0.1% expansion in September in line with the advance estimate would leave GDP by industry up 0.4% on a quarterly annualized basis (we calculate at 0.41%) for the first time since May. That's not far off the BOC's forecast in the latest MPR of 0.5% Q/Q expansion for overall GDP in the quarter. As such we would have to regard this data point as roughly neutral for the BOC policy outlook.

- August's decline was broad-based, with goods-producing industries falling 0.6% M/M and services 0.1%.

- Manufacturing remains in deep contraction (-0.5% M/M for the 4th contraction in the last 6 months, now running at -5.6% 3M/3M SAAR), with wholesale trade contracting the most since April (-1.2% M/M), construction printing the first negative month since February (-0.3%), and mining contracting (-0.7%) after two consecutive increases. That said, the 4.6% decline in air transportation (biggest fall since Jan 2022) that helpec drive a 1.7% fall in the transportation and warehousing sector appears to be a one-off due to an Air Canada flight attendant strike.

- Retail (+0.9%) reversed July's drop (-0.9%), while real estate (+0.1%) posted its 5th consecutive expansion and public administration was basically flat (slightly below 0.0%, unchanged for the last 5 months overall).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W BILL AUCTION: HIGH 3.785%(ALLOT 64.24%)

Oct-01 15:32

- US TSY 17W BILL AUCTION: HIGH 3.785%(ALLOT 64.24%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 27.84% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 6.17% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 65.98% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.32

FED: US TSY 17W AUCTION: NON-COMP BIDS $431 MLN FROM $67.000 BLN TOTAL

Oct-01 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $431 MLN FROM $67.000 BLN TOTAL

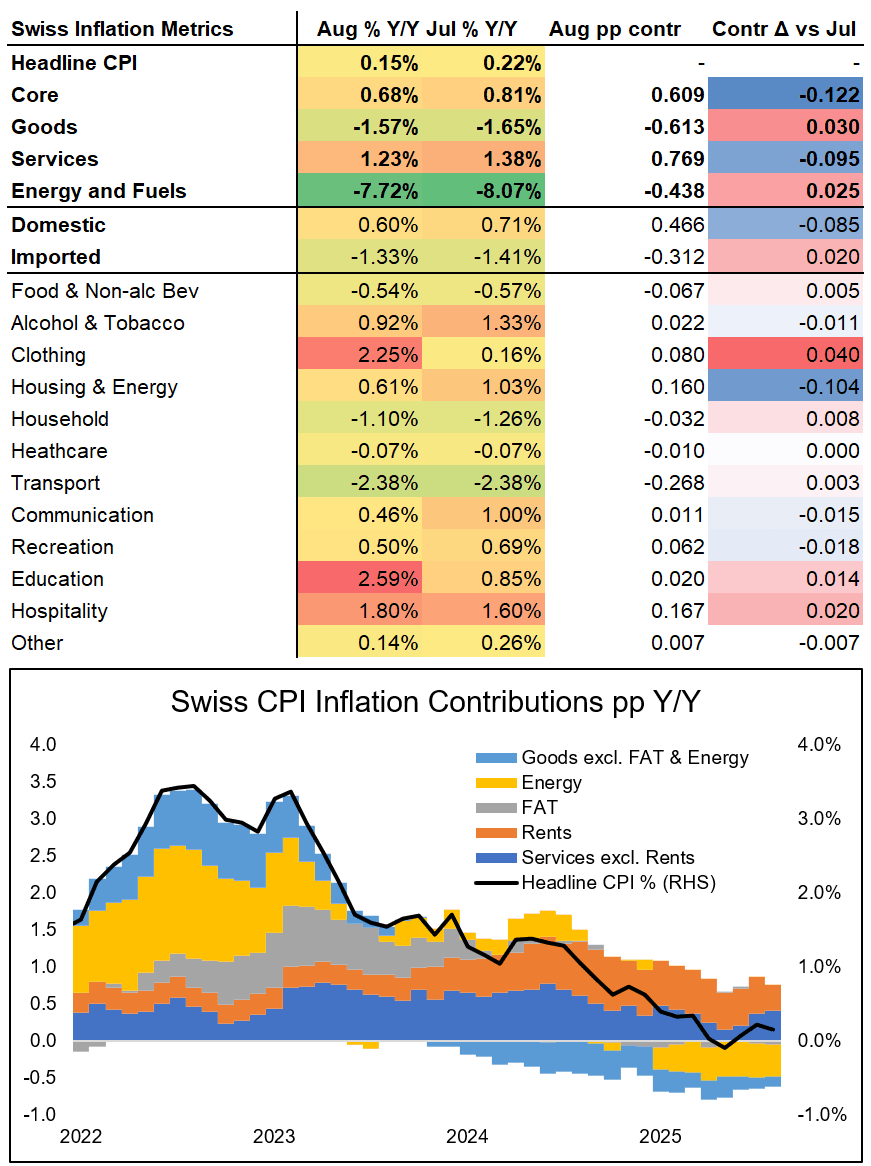

SWITZERLAND DATA: CPI Scheduled For Tomorrow 07:30 BST / 08:30 CEST

Oct-01 15:13

Swiss September CPI is scheduled for release tomorrow, October 2, 07:30 BST / 08:30 CEST, with consensus for a marginal acceleration in the headline Y/Y rate to 0.3% (0.2% August). Core CPI meanwhile is seen to remain unchanged at 0.7% Y/Y this time.

- A consensus reading would keep inflation within the SNB's defined target of price stability, and bring the average Q3 print to around 0.2%, in line with the SNB forecast for the quarter from last week. Market pricing remains for a mere 10bps of easing being priced through the June 2026 meeting, and it seems that substantial downside momentum in Swiss CPI would be needed to materially shift these expectations into a dovish direction. For a review of Thursday's SNB meeting, see here.

- Assuming such downside momentum unexpectedly should materialize at tomorrow's print, apart from headline inflation, focus should specifically be on domestic and services CPI, categories which the SNB historically seemed to look at when judging for underlying inflationary pressures. See chart / table below for recent figures.

- For tomorrow's release, UBS sees headline at "0.25% y/y, indicating upside risk to our rounded estimate of 0.2% y/y. At the component level, we expect our definition of core inflation (headline excluding energy and food) to edge up 0.1pp to 0.8% y/y largely due to a rebound in services related to transportation and package holidays, which were weaker than we anticipated in August. Outside of core, we expect energy inflation to rise 1.6pp to -6.1% y/y, while food inflation is expected to edge down 0.1pp to -0.6% y/y. Looking ahead, we forecast inflation to pick up in Q4 to an average of 0.4% y/y."