LOOK AHEAD: UK Timeline of Key Events (Times GMT)

Nov-25 06:23

| Date | Time | Period | Event |

| 28-Nov | 1530 | ---- | DMO Q1 Consultation Meetings |

| 29-Nov | 0930 | Nov | BOE Lending to Individuals / M4 |

| 30-Nov | 0001 | Nov | BRC Monthly Shop Price Index |

| 30-Nov | 0730 | ---- | DMO Publishes Q3 Issuance Calendar |

| 01-Dec | 0930 | Nov | S&P Global/CIPS UK Manufacturing PMI (final) |

| 05-Dec | 0930 | Nov | S&P Global/CIPS UK Services PMI (final) |

| 06-Dec | 0001 | Nov | BRC-KPMG Shop Sales Monitor |

| 06-Dec | 0930 | Nov | S&P Global/CIPS UK Construction PMI |

| 08-Dec | 0001 | Nov | RICS House Price Balance |

| 09-Dec | 0930 | Nov | BoE/Ipsos Inflation Next 12 Months |

| 12-Dec | 0001 | Dec | Rightmove House Prices |

| 12-Dec | 0700 | Oct | UK Monthly GDP/Trade/Production/Services/Construction |

| 13-Dec | 0700 | Oct | Labour Market Data |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: What to watch

Oct-26 06:16

- The Times reported overnight that PM Sunak will meet Chancellor Hunt today to discuss options over the timing of the Medium Term Fiscal Statement which is currently due 31 October. A delay of a couple of days (to still be ahead of the BOE meeting) is said to be under consideration as well as a more substantive delay further into November to turn the event into a full Budget. The OBR was due to deliver the final forecasts to the Chancellor tomorrow under it's original timeline which would mean that PM Sunak would have almost no time to make any tweaks to Hunt's policies. Given the importance of the fiscal plans, a delay seems very possible. The OBR's original timetable is available here.

- The BoC is seen hiking another 75bps this afternoon as still stubborn inflation and short-term consumer inflation expectations plus a depreciating CAD help warrant continued aggressive tightening. It’s not a done deal though, especially after BoC surprises this year: recent data have been mixed, including a sharp decline in business sentiment and less sharp fall in business inflation expectations. The market currently prices ~69bps for the meeting. Our base case is for the Bank to indicate further hikes ahead with a hawkish tone whilst trying to maintain optionality for a stepdown in the pace of rate hikes come the December meeting should data warrant it. For the full MNI BoC Preview click here.

- The market will also continue to look ahead to tomorrow's ECB meeting where a 75bp hike is expected. The full MNI ECB Preview is available here while the MNI Policy team published a story yesterday noting that changes to the TLTRO interest rate were being considered ahead of reserve tiering (full piece available here).

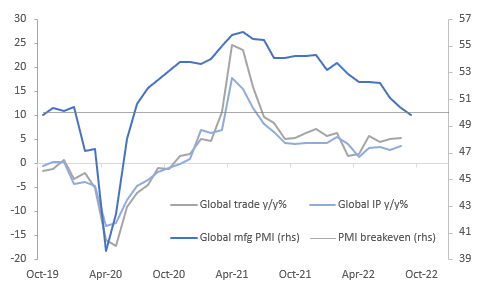

GLOBAL: August Global Trade And Production Data Don’t Show Slowdown … Yet

Oct-26 06:02

CPB data for August have been released and show that growth in global trade volumes and industrial production was steady at 5.2% y/y and 3.6% y/y. Export momentum on a 3-month basis was also steady at a robust 7.2% with both advanced and emerging economies solid. The expected slowdown had not yet hit the global economy in August but shipping and PMI data suggest it is coming.

Global growth vs PMI

Source: MNI - Market News/CPB/S&P Global

AUSTRALIA: MNI Insight: Q3 CPI Beat Sees Tightening Cycle Extend Into 2023

Oct-26 05:53

After today’s higher-than-expected Australian inflation data, we look at the details of the report and don’t expect them to be enough to shift the RBA back to a 50bp tightening pace. The cycle is likely to be extended into 2023 instead.

- Q3 Australian headline CPI data came in higher than expected but in line with the previous month but the trimmed mean underlying measure not only was higher than expected but also up on Q2 (1.8% q/q and 6.1% y/y, a new series high). Inflation momentum also remains strong. The proportion of major sub-indices with inflation stronger than 2.5% y/y (the mid-point of the RBA’s target band) rose to over 90%, fresh highs back to the early 2000s.

- RBA commentary also points in the direction of a 25bps move rather than 50bps on November 1.

- In the October minutes, the Board said that it could “draw out policy adjustments” which would “help to keep public attention focused for a longer period” on the Board’s determination to return to price stability.

- Deputy Governor Bullock commented recently that the RBA has more meetings than other central banks and so can do less per meeting but achieve the same result.

- Many of the reasons for pivoting haven’t changed, such significant uncertainties, lags involved, considerable tightening this year and wages consistent with the target.

- Read MNI Insight: Australian Q3 CPI Beat Sees TIghtening Cycle Extend Into 2023 here.