AUSSIE 10-YEAR TECHS: (U6) Bear Leg Considered Corrective

* RES 3: 95.636 - 76.4% retracement Oct' 25 - Jan' 26 downleg (cont) * RES 2: 95.472 - 61.8% retrace...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Thursday Data Calendar: Wkly Claims, PPI, 30Y Bond Re-Open

- US Data/Speaker Calendar (prior, estimate). All times ET

- 06/11 0830 Initial Jobless Claims (225k, 220k)

- 06/11 0830 Continuing Claims (1.777M, 1.785M)

- 06/11 0830 PPI Final Demand MoM (1.4%, 0.7%), YoY (6.0%, 6.4%)

- 06/11 0830 PPI Ex Food and Energy MoM (1.0%, 0.5%), YoY (5.2%, 5.4%)

- 06/11 1130 US Tsy $70B 4W & $70B 8W bill

- 06/11 1300 US Tsy $22B 30Y Bond auction re-open (912810UU0)

- 06/11 1200 Household Change in Net Worth

- Source: Bloomberg Finance L.P. / MNI

BOC: Analysts Stick To Hold View Through 2026, Tightening In 2027 (2/2)

Accordingly, analysts did not change their outlooks for BOC policy following June's meeting, with the overwhelming consensus being that there will be a hold through 2026 followed by 50bp in hikes in 2027, a path slightly less aggressive than portrayed by OIS markets. Some post-meeting notes in alphabetical order of institution (along with rate outlooks pre-meeting, presumed unchanged):

- BMO (Hold through 2026 and 2027): "Very little new information from the Bank of Canada, as the June policy statement and opening statement were similar to April's. The extra line about the economy being "weak" is a touch more dovish, but there's still concern about the potential for rising inflation from higher energy prices."

- CIBC (Hold through 2026, 50bp hikes in 2027): "We view today's communication as highlighting a very patient central bank that has plenty of time to wait and see how risks to the economy play out... rates at their current level should support a recovery in the economy later this year and into 2027 assuming some of the uncertainties regarding oil prices and trade lessen during that time period."

- Desjardins (Hold through 2026, 50bp hikes in H1 2027): "Given the two-sided risks to the inflation outlook, the Bank of Canada appears comfortable leaving rates on hold for now....That said, we believe the Bank is discounting some tailwinds to the Canadian economy."

- National (Hold through 2026, 50bp hikes in 2027): "Overall, the decision played out largely in line with our expectations but there was perhaps a slight dovish bias stemming from the Bank’s discussion of the economy. Indeed, there appeared to be more of a focus on current excess capacity and less emphaisis on their previously communicated expectation that this slack would be absorbed. In any case, the Bank believes that, for now, holding rates steady is the best way to balance both upside and downside risks to the outlook. Like markets, we view 2026 policy risks as skewed towards tightening and we don’t doubt the Bank’s resolve in ensuring price stability. However, we’d judge that the near-term hike scenario is growing less likely and we still expect the Bank to remain sidelined through year-end."

- RBC (Hold through 2026, 100bp hikes in 2027): "In short, their key message of staying prudent yet nimble was retained to preserve flexibility for a rate move if necessary...Much as we are, we think the BoC is adopting a wait-and-see approach to confirm the persistence of weaker-than-expected economic data since April, amid a highly volatile and revision-prone data environment."

- Scotiabank (50bp hikes in Q4, 25bp hike in early 2026): "The broad tone of the statement and Governor Macklem’s opening remarks to his press conference continue to suggest it is in monitoring mode, avoiding overreaction to any developments whatsoever and seeking further clarity on key risks to the inflation outlook. The overall communications were in line with expectations for now and ahead of a key second half of the year. The tone was neutral as they take in more information which is entirely as expected. Frankly, they could well have just cancelled the event. There was nothing new."

- TD (Hold through 2026, 50bp hikes in H1 2027): "the overriding sense we get from the last two announcements is that the Bank does not have a clear sense on the timing or direction of the next move in interest rates. Given the extraordinarily high degree of geopolitical uncertainty, this is probably a prudent approach."

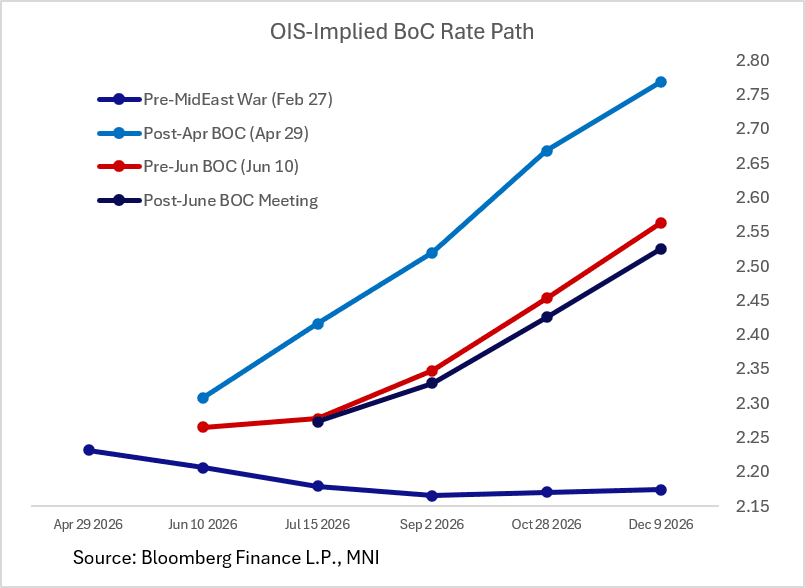

BOC: Retaining Message Of Flexibility Into The Summer (1/2)

The Bank of Canada's June meeting brought a very much expected overnight rate hold at 2.25% and only a slight implied change in hike expectations. The press conference concluded with about 26bp of 2026 tightening priced vs about 28bp pre-decision, although at least some of the overall dovish tone stemmed from a US CPI report earlier in the day that was slightly on the softer side of expectations. In short, the Bank didn't deliver any major surprises, and indeed retained a messaging and overall tone that was similar from the prior decision in April.

- The major risks remained the same - namely, a possible US trade shock to growth, and potential broadening and persistence of inflation from the Mideast war energy shock - and the overall tilt was toward tightening but not unduly so. Indeed Governing Council looks to retain the flexibility to either cut or hike as its next move, and does not seem in a hurry to commit.

- Even the removal of the April statement's reference to the current policy rate being "about right" if oil prices moderate in coming months was downplayed in the press conference, leaving the overall guidance intact: "consecutive" hikes if inflation broadens, or a possible easing if US trade relations deteriorate meaningfully.

- As MNI noted in our meeting preview, "Mixed activity data and an uncertain near-term geopolitical outlook make it likely that the BOC will also likely leave its message from the last meeting in April largely intact: potential upside in rates is greater than the downside at this juncture, but maintaining policy is still the “right thing to do for today” as uncertainty over trade and energy prices looms large."

- Should the BOC look to decide upon a more decisive message, the most logical timing would be July's meeting (July 15 decision) at which point it will have another round of business surveys and monthly data upon which to base its conclusions, and of course potentially less uncertainty over external risks. But at the current juncture, even that looks to be too early for such a shift. For now, the upside inflation/downside growth dilemma remains.