SCHATZ TECHS: (U5) Support Tested

- RES 4: 107.430 High Jun 13

- RES 3: 107.360 High Jul 22 and a key resistance

- RES 2: 107.197 50-day EMA

- RES 1: 107.123 20-day EMA

- PRICE: 107.070 @ 07:20 BST Aug 15

- SUP 1: 106.990 Low Aug 12

- SUP 2: 107.993 1.500 proj of the Jul 7 - 11 - 22 price swing

- SUP 3: 106.964 1.618 proj of the Jul 7 - 11 - 22 price swing

- SUP 4: 106.928 1.764 proj of the Jul 7 - 11 - 22 price swing

The sell-off in Schatz futures resulted in the bear trigger being pierced Tuesday: the 107.010 support gave way, signalling potential for further near-term losses. The move lower marked new contract lows, exposing projection levels layered between 106.928-107.993, which should act as a modest zone of support ahead of the March levels on the continuation contract. The 20-day EMA remains the upside level of interest, having defined the early August downtrend, today at 107.123.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

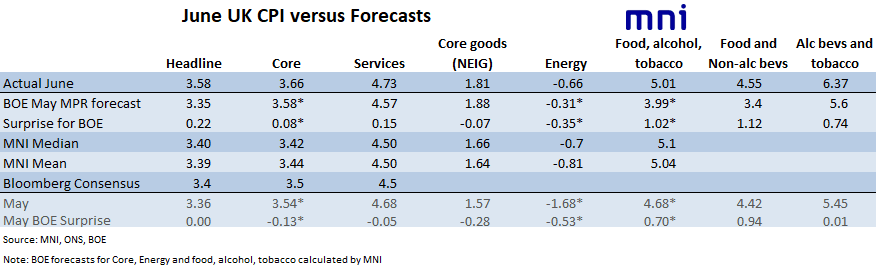

UK DATA: CPI: Air fares, clothing, media drivers with marginal broad services

- Looking through, other than the air fares there's no one thing that is driving the beat for services. Core goods are likely driven by clothing and recording media. There were just a lot of categories that added 0.01ppt here and there - so it looks a relatively broad-based marginal increase in quite a few services categories here.

- This does put headline CPI 0.22ppt above the BOE's May MPR forecast with services 0.15ppt above forecast, core goods 0.07ppt below forecast, food 1.02ppt above forecast and energy 0.35ppt below forecast.

- Overall, we think the BOE will largely describe inflation in the August MPR as broadly in line with their forecast, albeit with food price inflation higher than expected.

Notable categories:

- Air fares were stronger than expected at 7.9%M/M (the consensus there was around 3%). That contributed 0.03ppt to headline CPI, and around 0.06ppt to services CPI.

- Clothing relatively strong, adding 0.04ppt to headline CPI.

- Recording media also added 0.03ppt to headline CPI.

- Accommodation actually detracted -0.04ppt from headline CPI.

EURJPY TECHS: Northbound

- RES 4: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 3: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 2: 173.43 High Jul 12 ‘24

- RES 1: 173.24 High Jul 15

- PRICE: 172.91 @ 07:17 BST Jul 16

- SUP 1: 171.60 Low Jul 14

- SUP 2: 170.03 20-day EMA

- SUP 3: 169.32 Low Jul 3

- SUP 4: 167.31 50-day EMA

The trend condition in EURJPY is unchanged, a bull phase is in play and fresh cycle highs this week reinforce current conditions. The move higher also maintains the price sequence of higher highs and higher lows and note that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 173.43, the Jul 12 ‘24 high. Support to watch lies at 170.03, the 20-day EMA.

EGBS: Knee Jerk Lower Post UK CPI; Bearish Theme Intact

Bund futures fell ~25 ticks to a low of 129.31 following the stronger-than-expected UK CPI report, but have since settled around 129.39 (-7 ticks today). A bear cycle remains intact, with initial support the July 14 low at 129.08. Clearance of this level would expose the key support and reversal trigger at 128.97 (May 14 low).

- Bunds drifted higher overnight alongside USTs, but the bulk of yesterday’s US CPI reaction has held.

- The 10s30s JGB curve has flattened 8.5bps, unwinding almost all of month’s steepening. Primary focus for JGB markets remains on Sunday’s Upper House Election.

- US President Trump suggested pharma tariffs may start to be applied from month’s end – but no specific levels were cited at this stage.

- Germany will return to the market this morning to hold a 30-year Bund auction. On offer will be E1.0bln of the 1.25% Aug-48 Bund alongside E1.5bln of the 2.90% Aug-56 Bund.

- There will be focus on OATs following yesterday’s 2026 budget announcement. While the market reaction at the time was limited, several political opponents from the right and left of the spectrum came out and criticised Bayrou’s proposals. This increases the risk of a censure in the short-term.

- Yesterday evening, ECB’s Nagel re-iterated his preference for a “steady hand” in setting rates, in line with previous comments and his hawkish leaning view.

- Today’s regional calendar includes final Italian June HICP and May Eurozone trade data. Wider focus will be on the US PPI report following yesterday’s CPI reading, which started to show some tariff impact in core goods categories.