US 10YR FUTURE TECHS: (U5) Outlook Remains Bullish

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5 and the bull trigger

- PRICE: 111-25 @ 11:12 BST Aug 20

- SUP 1: 111-11 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

A bullish theme in Treasury futures remains intact. The contract continues to trade above support at the 50-day EMA, at 111-.11. A clear break of this average would expose support at 110-23+, the Aug 1 low. For bulls, a resumption of gains would refocus attention on 112-15+, the Aug 5 high and bull trigger. A break of this hurdle would resume the uptrend and pave the way for a climb towards 112-23 initially, the May 1 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Bunds Test Next Resistance

Looks like block flow helps drive this latest leg of Bund strength with ~2.5K lots lifted at 130.15.

- Contract nears resistance at the 50-day EMA (130.21).

- Flow helps underpin wider core global FI as NY participants start to filter in, new session highs registered across the major contracts.

- Little new on the headline front, focus remains on hawkish U.S.-EU trade reports released over the weekend.

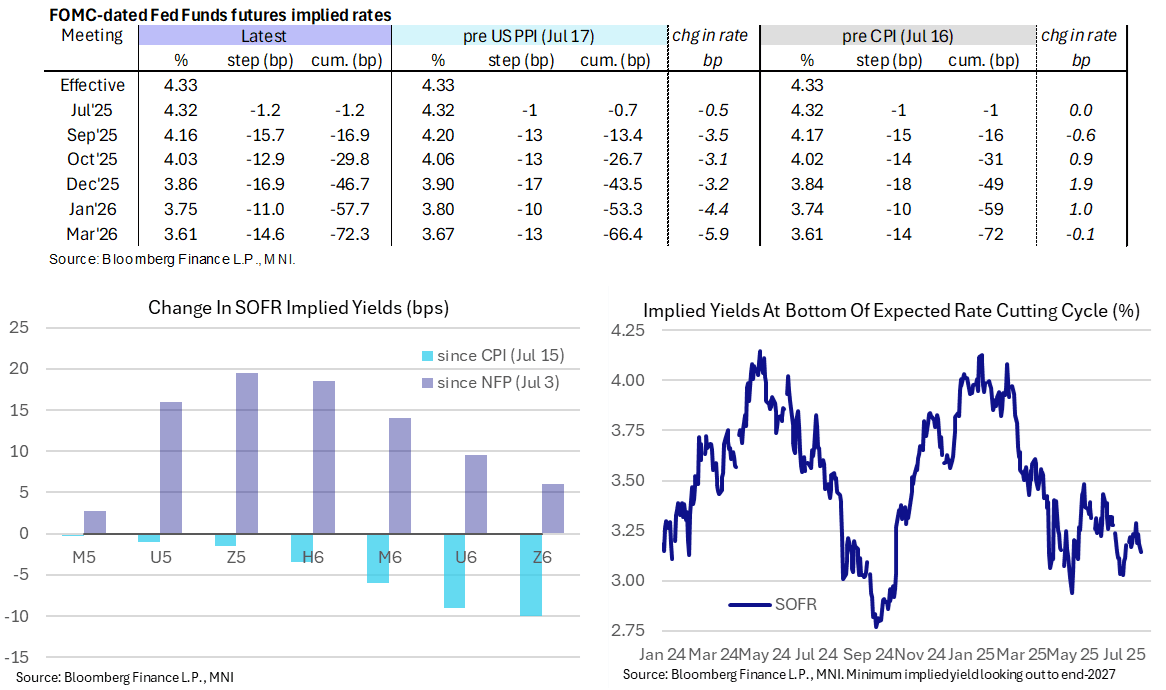

STIR: Fed Rates Cool With Trade Policy In Focus

- Fed Funds implied rates are up to 1bp lower overnight for 2025 meetings, seemingly stemming from a WSJ report reiterating stances seen last week that the EU is preparing to pushback more firmly against US trade measures.

- Cumulative cuts from 4.33% effective: 1bp Jul, 17bp Sep, 30bp Oct, 46.5bp Dec, 57.5bp Jan and 72.5bp Mar.

- The near-term path remains within last week’s range though, primarily driven by some hawkish CPI details before Trump-Powell headlines notably built on a dovish PPI report.

- Rates see larger rallies further out the curve as weaker growth prospects weigh.

- That’s demonstrated by the SOFR implied terminal yield dropping 4bps from Friday’s close for 3.145%, tilting a little closer to five rather than four cuts for the cycle from current levels.

- The FOMC has entered its media blackout ahead of the Jul 29-30 meeting.

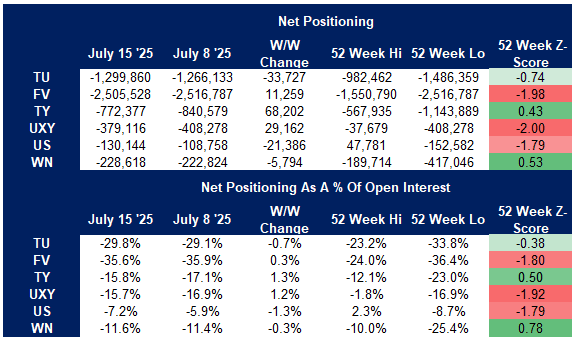

US TSY FUTURES: CFTC Shows Asset Managers Trimming Long, Funds Trimming Short

The latest CFTC CoT report pointed to cover of existing positions across the major investor cohorts (in curve-wide terms) that we track during the week ending July 15.

- Asset managers trimmed net longs in all contracts outside of TU futures (where they extended their net long), reducing their net long exposure by a little over $13mln DV01, albeit remaining net long across the curve.

- Leveraged funds also trimmed net shorts in most contracts (only extending net shorts in TU & US futures), reducing exposure by ~$4.5mln DV01, but remaining net short across the curve.

- Broader non-commercial net positioning saw net shorts added to in the wings (TU, US & WN), while net shorts were trimmed in the belly & intermediates (FV, TY & UXY), with the cohort remaining net short across the curve.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.