US 10YR FUTURE TECHS: (U5) Fades on Fed

- RES 4: 112-15 61.8% retracement of the Apr 7 - 11 sell-off

- RES 3: 112-12+ High Jul 1 and a bull trigger

- RES 2: 111-28 High Jul 3

- RES 1: 111-14+ High Jul 22 & Jul 30

- PRICE: 110-31+ @ 20:21 BST Jul 30

- SUP 1: 110-19+/08+ Low Jul 24 / Low Jul 14 & 16

- SUP 2: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 3: 109-28 Low Jun 6 and 11

- SUP 4: 109.25 Low May 27

Treasury futures traded higher Tuesday, but faltered into the Wednesday close on the Fed decision. Recent gains resulted in a break of the 20-day EMA, strengthening the recovery that began mid-July. Note too that resistance at 111-13+, the Jul 10 high, has been pierced. A clear break of it would highlight a stronger reversal and open 111-28, the Jul 3 high. Key support is 110-08+, the Jul 14 and 16 low. Clearance of this level would reinstate a bearish theme. First support is at 110-19+, the Jul 24 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Late Sep'25 30Y Buy

- +6,700 USU5 115-15, buy through 115-14 post time offer at 1459:24ET, DV01 $830,000.

- The 30Y contract trades 115-11 at the moment, however, +28

SOFR: Morgan Stanley Opinion: Buy Dec'25 SOFR Ahead May Jolts, June NFP Data

- Morgan Stanley strategists suggest buying SFRZ5 futures ahead of tomorrow's May Jolts and Thursday's June Non-Farm Payrolls release that may underpin rate cut projections that are over halfway between 50bp to 75bp in rate cuts by year end.

- "Downside risks to US labor market data remain underpriced, especially considering the potential for near 0k payroll prints starting as soon as July," MS suggested in a recent strategy piece.

- Projected rate cut pricing gains slightly vs. late Friday (*) levels: Jul'25 at -5.3bp (-4.8bp), Sep'25 at -28.6bp (-28.2bp), Oct'25 steady at -46.3bp, Dec'25 at -66.8bp (-66.2bp).

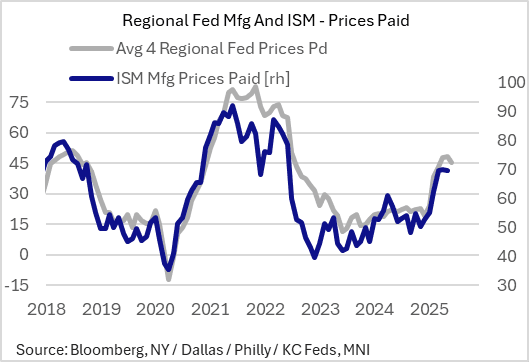

US OUTLOOK/OPINION: ISM Manufacturing Prices Paid Seen Steady (2/2)

The Prices Paid component of June's ISM Manufacturing survey, which will be closely watched for signs that tariffs are feeding into goods inflation, is expected by consensus to see a fairly flat reading of 69.5 vs 69.4 prior.

- Regional Fed surveys were extremely mixed though overall they point to flat or if anything slightly lower prices paid, but this could be dependent on when the question was asked. Empire State (New York) prices paid pulled back to a 3-month low, with Philly's at a 4-month low; however Kansas City prices pad rose to a 36-month high, with Dallas's ticking up to a 2-month high.

- The latter two regions are relatively impacted by energy sector developments so there may have been an element of the June oil price jump involved, particularly since this occurred in the latter half of the month before receding. For example Dallas's was collected June 17–25, with the high in oil prices right in the middle of those dates.

- Richmond's 12-month change meanwhile showed a sharp rise to a 26-month high (6.1%). though this is not really on a comparative basis with the index readings elsewhere.

- The S&P Global flash PMI noted a sharp rise in price pressures in the month :"Manufacturers’ input prices and selling prices both rose at rates not seen since July 2022, as higher costs were passed on to customers. Close to two-thirds of all manufacturers reporting higher input costs attributed

these to tariffs, whilst just over half of respondents linked increased selling prices to tariffs."