MNI EXCLUSIVE: Two-Part Interview With Ex-Cleveland Fed President Mester

Jul-18 2025 13:41

- MNI discusses the risks to Fed independence and discusses tariffs' impact on inflation with former Cleveland Fed President Loretta Mester -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR: The Strip leans on the flatter side

Jun-18 2025 13:40

- Volumes along the Euribor strip are still below averages and are limited, the strip is still leaning on the Flatter side, with similar moves seen in Core Govie curves.

- Latest notable flow in the strip is seen in ERZ5, just bought in over 5k.

EQUITY TECHS: E-MINI S&P: (U5) Trend Structure Remains Bullish

Jun-18 2025 13:39

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6047.75 @ 14:27 BST Jun 18

- SUP 1: 5979.00/5896.83 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. For now, the most recent shallow pullback is considered corrective. The contract has pierced support at 6003.83, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5896.83. Key short-term resistance and the bull trigger has been defined at 6128.75, the Jun 11 high.

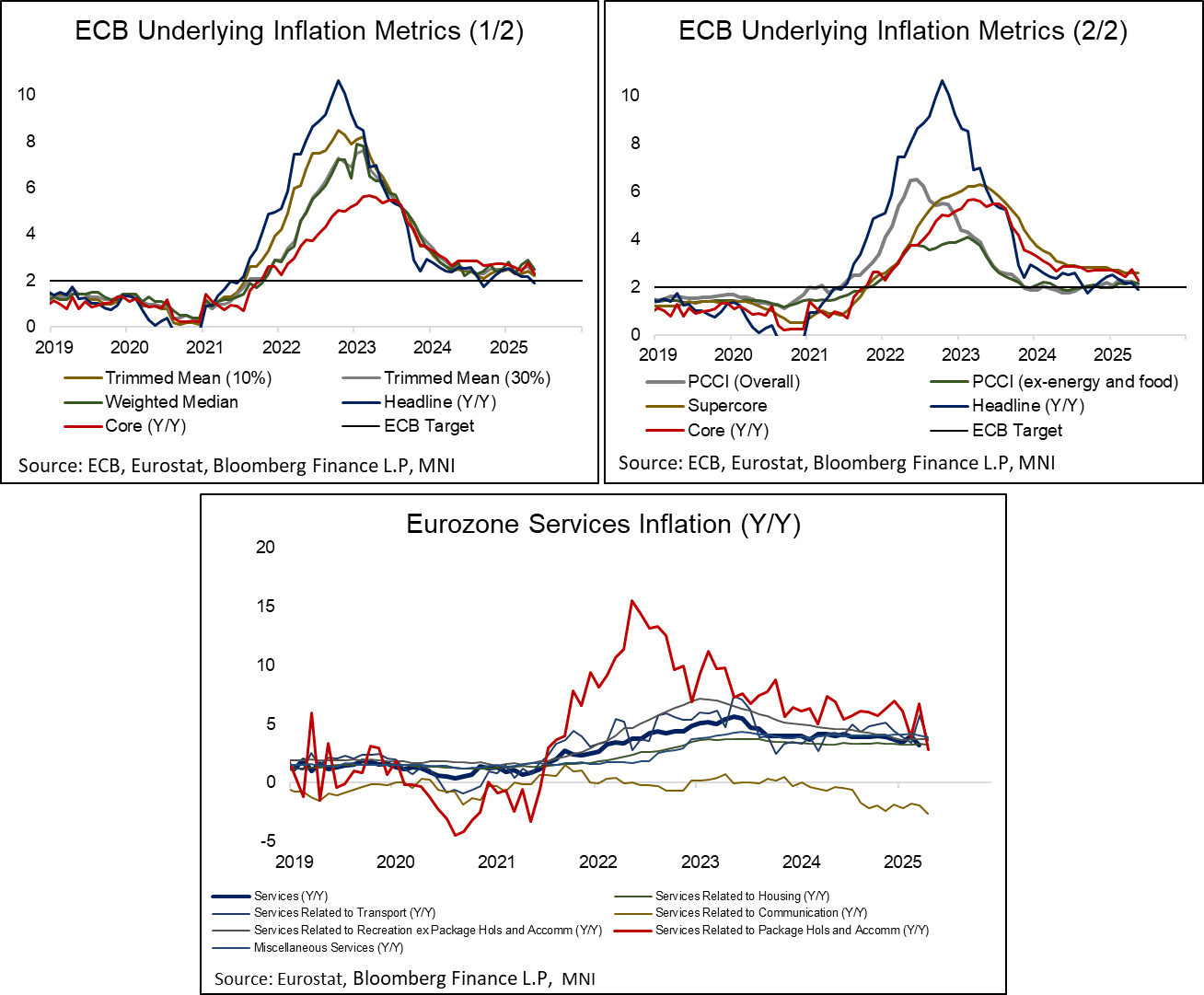

EUROPEAN INFLATION: Easter Sensitive Categories Drove May Services Disinflation

Jun-18 2025 13:27

- As foreshadowed by country-level data, the pullback in Eurozone services inflation to 3.23% Y/Y (vs 3.98% prior) was largely a function of lower airfares, package holidays and accommodation inflation (i.e. Easter-sensitive categories).

- Despite this, the ECB has expressed broader confidence around the outlook for services inflation. In the June projections, they staff noted that “In the medium term, the decline in HICPX inflation mainly relates to services inflation as post-pandemic reopening effects unwind and the as the downward impact from monetary policy tightening continues to feed through. A faster unwinding of services inflation is seen to be hindered by declining but still elevated upward pressures from labour cost developments.” Services inflation is seen at 3.2% Y/Y in Q4 2025 and 2.5% Q/Q in Q4 2026.

- Indeed, the ECB’s underlying inflation metrics saw a broad-based softening in May, converging slowly towards the 2% level.

- Services related to package holidays and accommodation eased to 2.84% Y/Y in May (vs 6.73% prior), the lowest since 2021. Meanwhile, services related to transport (mostly airfares) fell to 3.62% Y/Y (vs 5.74% prior).

- Other services categories saw much smaller movements on the month:

- Services related to communication: -2.59% Y/Y (vs -1.92% prior),

- Services related to housing: 3.28% Y/Y (vs 3.29% prior).

- Services – miscellaneous: 3.86% Y/Y (vs 4.00% prior).

- Services related to recreation and personal care, excluding package holidays and accommodation: 3.72% Y/Y (vs 3.74% prior).

- The ECB’s seasonally adjusted data saw immaterial revisions relative to the flash release. Services prices fell 0.17% M/M (in line with flash) while non-energy industrial goods were revised down to 0.03% M/M from 0.06% initial.