EM ASIA CREDIT: TSMC (TAISEM): Q4 results on tapes

( Aa3/AA-/NR) "*TSMC 4Q GROSS MARGIN 62.3%, EST. 60.6%" - BBG "*TSMC 4Q NET INCOME NT$505.7B, EST. ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH Fresh Lows Under 7.0400, Can We Test 7.00 Sooner Than Expected?

USD/CNH is just up from session lows (7.0373), last in the 7.0375/80region. The currency is only marginally stronger, but is outperforming some other North East Asia currencies so far today, with KRW and TWD under pressure amid fresh equity market weakness. USD/JPY is lower though, back to 154.75/80, so this may be seeing some positive spill over to CNH. USD/CNY spot is also down but remains above 7.0400 at this stage. The earlier USD/CNY fix was set above market forecasts but still comfortably below yesterday's outcome. Also via BBG: "dollar-buying by major Chinese banks softens, reducing resistance to further gains for the renminbi."

- Until we see greater push back on yuan gains the market remain comfortable to keep looking for downside in USD/CNH, with the 7.00 region the likely next focus point.

- BBG notes that a stronger yuan backdrop is also gaining traction onshore amongst economists and former central bank officials: see this link.

- Despite the break lower in USD/CNH, vol and risk reversal markets still look well behaved. The 1 month implied vol is a little higher, but at 2.44%, remains close to recent cycle lows. The 1 month RR is also up from recent lows, last -0.47.

- Focus remains on stronger yuan gains to address external imbalances, although expectations of a sharp rally in the yuan is not the consensus view point. The BBG survey only has CNY strengthening to 7.00 by Q3 2026.

US TSYS: Yields Grind Lower as Equities Fall, Attention Turns to Data

Bond futures opened up this morning in Asia but with limited follow on. The US 10-Yr opened at 112-10+ and got to 112-12+ where it has stayed all day as it nears the topside resistance being the 100-day EMA of 112-14+.

Cash was stronger with yields -0.2 - 1.00bps lower across the curve with intermediate maturities the best performers.

- The 2-Yr is down -0.6bps at 3.497%

- The 5-Yr is down -0.9bps at 3.717%

- The 10-Yr is down -0.6bps at 4.17%

- The 30-Yr is down -0.2bps at 4.846%

US Non Farm Payrolls are the next focus for markets. Here is the MNI US Payrolls Preview: Double NFPs And A Single Unemployment Update

https://media.marketnews.com/USNFP_Nov2025_Preview_postshutdown_392dffc2d3.pdf

Tonight there is a US$75bn 6-week auction as the primary focus.

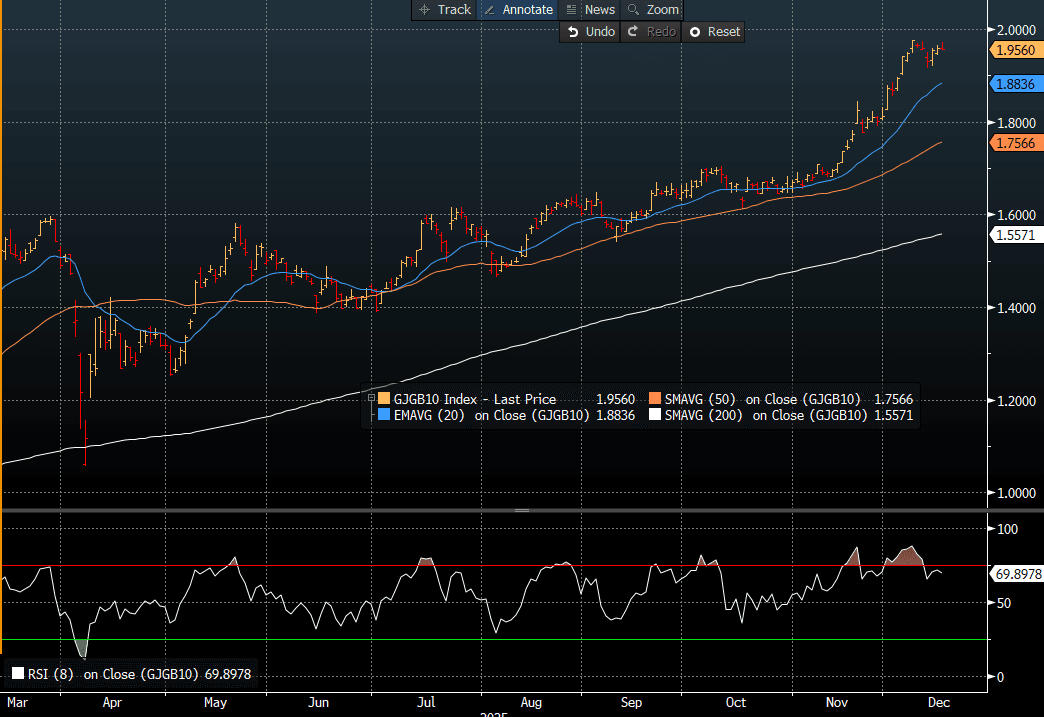

JGBS: Subdued Session, BOJ Hike On Friday Is Fully Priced

JGB futures are little changed compared to settlement levels.

- The BOJ is widely expected to raise its policy interest rate by 25 basis points to 0.75% at the upcoming December 18-19 Monetary Policy Meeting.

- Some analysts, however, caution that a December hike is not guaranteed. A 26 November Reuters article described a December move as merely “possible.” Goldman Sachs has emphasised that with only a limited number of companies having announced wage plans so far, there is a risk that insufficient information will be available by the December meeting. In that scenario, the BOJ may delay a hike until wage announcements by large firms later in December and the January Branch Managers’ meeting.

- Cash US tsys are slightly richer, with a steepening bias, in today's Asia-Pac session ahead of today's heavy US data schedule that includes headline NFP for November, weekly ADP, Retail Sales and S&P Global flash PMIs.

- Cash JGBs are little changed across benchmarks out to the 20-year, and ~2bps richer (30-year) beyond. The benchmark 10-year yield is 0.3bp lower at 1.956% versus the cycle high of 1.976%.

- Swap rates are little changed.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data alongside 1-year supply.

Source: Bloomberg Finance LP