US-CHINA: Trump - Will Ask Xi To 'Open Up' China

US President Trump has posted via Truth Social as he heads towards China, with key US business leade...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

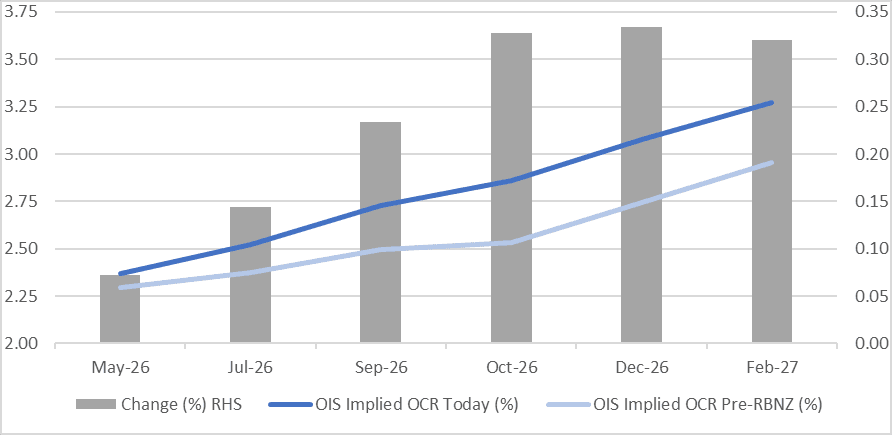

STIR: RBNZ-Dated OIS Pricing Post-RBNZ Firming Extends

RBNZ-dated OIS pricing is 2-10bps firmer across meetings today and 7-33bps firmer than last Wednesday’s pre-RBNZ levels.

- In a unanimous decision, the RBNZ kept rates at 2.25% but warned that it is prepared to hike if inflation is not expected to return to the 2% band mid-point over the medium term. If core and wage inflation as well as inflation expectations aren’t contained “decisive and timely increases in the OCR would be required”.

- Food and other monthly prices for March are released on Friday and likely to be the focus of this week as it will be the first gauge of the impact of higher fuel prices from the Iran War and if there are already signs of second-round effects. Q1 CPI data are released 21 April but any uptick from March will be mitigated by the more “usual” January/February months.

- 12bps of tightening is priced for May, while February 2027 assigns 102bps.

Figure 1: RBNZ Dated OIS Current vs. Pre-RBNZ (%)

Source: Bloomberg Finance LP / MNI

CROSS ASSET: Risk Off Stabilizes, As Markets Await Iranian Response To Blockade

Risk sentiment has stabilized somewhat as the Asia Pac Monday session unfolds, with focus on Iran conflict/Hormuz headlines. Risk assets have moved away from earlier lows, but remain in the red, while oil prices are holding 7-8% gains. WTI has settled near $104/bbl, off earlier highs above $105/bbl. US equity futures, per Eminis, are down 0.75%, but are up from earlier lows sub 6800. The USD is firmer, but likewise away from best levels, particularly against higher beta plays. AUD/USD hit lows of 0.6986 in early dealings, but is now back to 0.7035/40 (off around 0.40% versus end Friday levels). Dutch TTF (natural gas) is 5.4% below its high earlier, which started trading in our time zone as of today.

- Earlier it was announced the naval blockade would commence 10am US ET on Monday. Headlines indicated the blockade will focus on ships entering or exiting Iranian ports and not ports from other countries. It remains to be seen though how much shipping flow from other countries flows under such a regime.

- Focus will be on the Iranian response, particularly in terms of outbound oil flows, along with threats to disrupt Saudi Arabia flows through its East-West pipeline, which are exported via the Red Sea.

- Elsewhere the WSJ reported that Trump is considering resuming limited military strikes on Iran to prompt a return to the negotiating table and break the stalemate.

- Trump also gave an impromptu press conference, largely reiterating his previous remarks around the destruction of Iran's military forces. He added the naval blockade will be very effective and it does not matter if Iran does not come back to the negotiating table.

CHINA PRESS: PPI Strengthens, Downstream Profits May Get Squeezed

China’s PPI rose 0.5% year-on-year in March, ending a 41-month decline, and jumped 1.0% month-on-month — the biggest gain in 48 months, driven by rising global commodity prices and better industrial supply and demand. “Upstream prices increased sharply while demand in downstream sectors remained weak, which may squeeze profits,” reported China Business News, citing an analyst with Golden Credit Rating Company Monday.