GLOBAL POLITICAL RISK: Trump Says To Help Some Ships Exit Hormuz Starting Monday

May-03 21:12

An early story this morning that Trump says the US will begin guiding some trapped ships that aren't...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US LABOR MARKET: MNI US Employment Insight: Strong Bounce Alleviates Concerns

Apr-03 16:01

We've just published our latest U.S. Employment Insight: Download Full Report Here

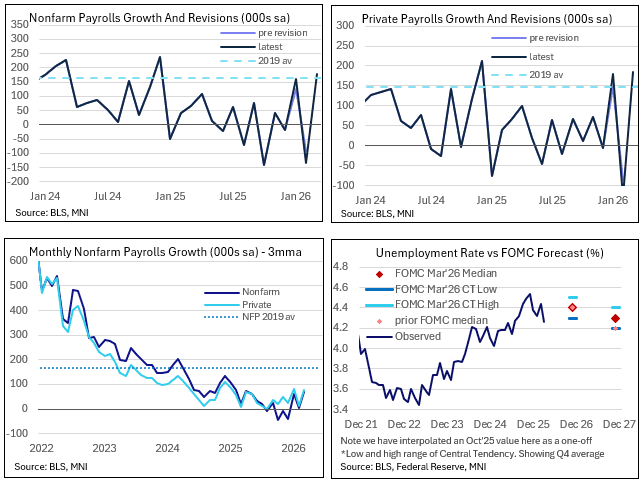

US LABOR MARKET: Strong Payrolls Report, But Supply Vs Demand Debate To Go On

Apr-03 14:59

March's BLS employment report was undoubtedly strong in the main readings, and will have allayed concerns that February's pullback in payrolls portended a renewed leg of weakness in the labor market.

- The 178k headline gains in the Establishment survey easily beat the 70k MNI dealer median, with private payrolls up 186k vs the 75k expected. And the dip in the unemployment rate to a 9-month low 4.26% (consensus 4.4%, 4.44% prior) in the Household Survey suggested that the headline payroll gains were no fluke.

- But while this was a better than expected report, it comes in the context of significant volatility in month-to-month figures, including major revisions to February's reading (-113k vs -92k, offset by a +34k upside revision to January). And the rebound, while impressively broad across sectors, was still heavily driven by healthcare employment and other sectors that appeared impacted by one-off factors in February.

- Stepping back, the 3-month change in payrolls has been a solid if more modest +68k (an 11-month high), with the 6-month average gains rising to 15k from -2k in Feb for the highest since in 6 months. So, an improvement in trends, but not enough to suggest that employment gains are doing anything but treading water. Payrolls have grown by just 0.2% Y/Y.

- Indeed while the unemployment rate drop was suggestive of reduced labor market slack, it was flattered by a decline in the size in the labor force as well as falls in the participation and employment-to-population ratios, as well as the weakest response rate in survey history.

- Additionally, growth in average hourly wages continued to decline to fresh post-2021 lows on a Y/Y basis and well off post-pandemic highs.

- Taken together, the FOMC will probably be relieved that it has another month to assess the fallout from the Middle East war without being unduly concerned about an imminent collapse in the labor market (for which evidence of near-term war impact is so far scant).

- The Committee will continue to see a low-hiring, low-firing labor market that is indicative of being roughly in balance, with the underlying data meaning the debate is set to continue over whether it is weakness in labor supply or demand that has the upper hand.

- Indicative of this reinforced wait-and-see stance, market-implied Fed rate cuts were pared in the wake of the report, with Fed funds futures currently seeing just 1bp of cuts in 2026 as we head into the holiday weekend, vs around 5bp pre-report.

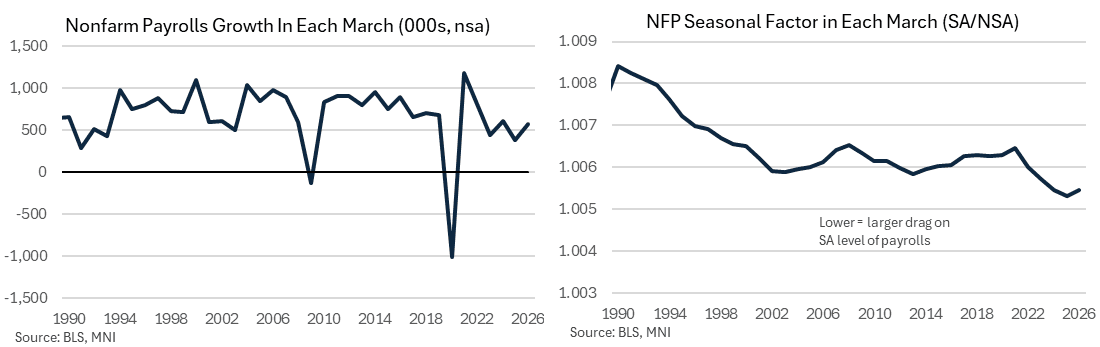

US DATA: Limited Distortions From Birth-Death, Seasonal Adjustments

Apr-03 14:38

Even though March's headline payrolls number handily beat expectations, seasonal adjustments and the establishment Birth-Death adjustment were not particularly favorable to the reading.

- The non-seasonally adjusted change in nonfarm payrolls was +571k, coming after +476k. In keeping with March typically being a strong month on an NSA basis, the seasonal adjustment factor was negative for the gains, but at 0.995 was little different than in March 2025 (the chart below shows the reciprocal).

- The BLS's Birth-Death model subtracted 47k (NSA) from payrolls after adding 90k in February, for a 3rd subtraction in 4 months. That compares to -33k in March 2025 and was larger than the -22k average for the last 5 March's.

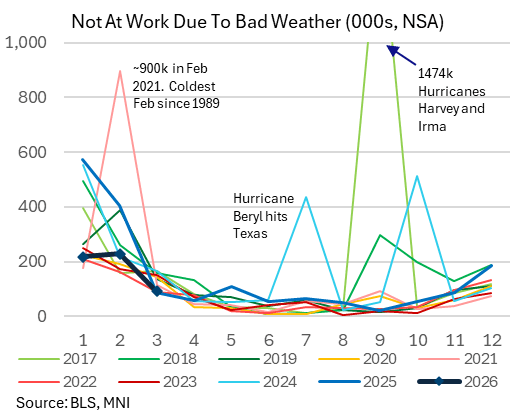

- As far as the Household Survey is concerned, weather wasn't really a factor: 91k (NSA) were not at work due to bad weather, almost identical to the prior year (87k) though slightly lower than the 122k average of the last 5 March's (this year's weather was particularly good for March). The rebound in construction and leisure/hospitality payrolls in March were also suggestive of a more solid-than-usual weather effect after February's depressed figures.

Trending Top

May-01 21:26