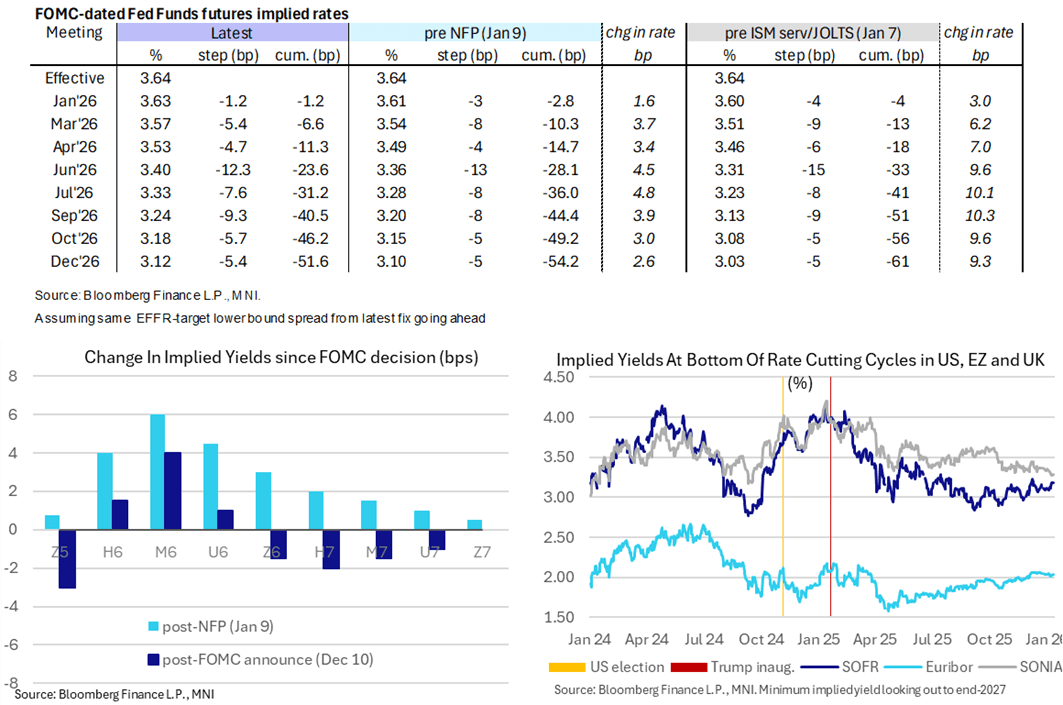

US TSYS: Treasury Yields Rise After Stronger Than Expected Job Gains

- Treasuries look to finish broadly weaker Wednesday, off initial knee-jerk lows following this morning's Jan employment data release.

- Nonfarm payrolls growth was far stronger than expected in January at 130k (cons 65k) after negligible two-month revisions of -17k (mainly in Nov). Private payrolls saw a larger beat, both with the 172k (68k cons) in January but with also a two-month revision of +49k (fairly evenly split over Dec and Nov).

- The Household survey showed a stronger labor market than expected, with the unrounded unemployment rate of 4.283% not just below the consensus of 4.4% and 4.375% prior, but also the lowest since July.

- Treasuries dropped from 112-19 to 112-00 low(-16.5) - the initial technical support (20-day EMA) holding while futures see-sawing off lows through midday. Brief risk-off support as Bitcoin fell 4% to near 66k before paring losses to -2.05%.

- Treasuries retreated after the $42B 10Y note auction (91282CPZ8) tailed, drawing 4.177% high yield vs. 4.162% WI; 2.39x bid-to-cover vs. 2.55x prior. Lowest since Aug 2025: indirect take-up retreats 64.54% vs. 69.65% prior.

- Looking ahead: UK GDP and US jobless claims highlight a lighter calendar on Thursday, before he focus turns to Friday’s release of US CPI.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late Treasury Roundup: Future Fed Independence At Risk, Geopol Tensions

- Treasuries look to finish mostly weaker Monday, curves bear steepening with the long end underperforming amid uncertainty over future Federal Reserve independence. This after the DOJ announced it's investigation of Fed Chairman Powell over the weekend related to his testimony before the Senate Banking Committee last June.

- Chairman Powell quickly responded to the criminal indictment threats, in short "this is about whether the Fed will be able to continue to set interest rates based on evidence and economic conditions—or whether instead monetary policy will be directed by political pressure or intimidation" Powell said.

- Note, geopolitical tensions continue to heat up (or at least simmer) after the US attack on Venezuela, followed by threats to Iran and Greenland.

- Short end rates outperformed as markets continue to anticipate no rate change from the Fed at it's next meeting on January 28. The first full (25bp) cut priced in around June-July.

- Treasuries climbed to session highs after the Tsy 10Y auction re-open stopped through: drawing 4.173% high yield vs. 4.179% WI, but retreated again in late trade as markets set sights on headline CPI inflation metric for December. Currently, the TYH6 contract trades -2.5 at 112-04.5, above a key support at 111-29, the Dec 10 low. A breach of 111-29 would open 111-19 initially, a Fibonacci projection.

- Reminder, the next earnings cycle kicks off in earnest this week with Bank of NY Mellon, JPM reporting on Tuesday January 13, Bank of America, Wells Fargo and Citigroup on Wednesday, Goldman Sachs, Blackrock and Morgan Stanley on Thursday.

AUDUSD TECHS: Recent Pullback Considered Corrective

- RES 4: 0.6872 38.2% retracement of the 2021 - 2025 L/T downtrend

- RES 3: 0.6858 1.000 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 2: 0.6795 0.764 proj of the Nov 21 - Dec 10 - 18 price swing

- RES 1: 0.6767 High Jan 7 and the bull trigger

- PRICE: 0.6714 @ 17:29 GMT Jan 12

- SUP 1: 0.6664 Low Jan 9

- SUP 2: 0.6627 50-day EMA

- SUP 3: 0.6593 Low Dec 18

- SUP 4: 0.6553 Low Dec 3

Recent weakness in AUDUSD appears corrective and this has allowed an overbought condition to unwind. Initial firm support lies at 0.6678, the 20- day EMA. It has been pierced, a clear break of it would expose support at the 50-day EMA, at 0.6627. The area between the two EMAs represents a key support zone. For bulls, a resumption of the uptrend would open 0.6795 next, a Fibonacci projection.

US INFLATION: FOMC To Downplay December CPI Payback

This will be the last major data report ahead of the Fed’s end-January meeting, but is very unlikely to sway the FOMC away from holding rates as is heavily priced (only about 1bp of cuts implied by futures). By the same token, a particularly strong reading probably won't be taken as a major warning signal about resurgent inflation, given the expected upside distortions mentioned in our CPI preview.

- Fed Chair Powell had warned in December ahead of the Oct/Nov CPI report that “data was not collected in October and half of November. So, we're going to get data, but we're going to have to look at it carefully and with a somewhat skeptical eye.” And following that report, NY Fed President Williams downplayed the signal from the data, confirming that the FOMC will interpret these readings with extreme caution, using the December CPI report due out before the January meeting to make more sense of underlying price dynamics.

- Even if the data are more robust this time, the continued distortions in the December report will probably keep the Committee waiting for the next two CPI reports available by the following meeting on March 17-18 to get a better sense of underlying pressures (January's is out February 11; February's is out March 11 - of course this assumes that there isn't another government shutdown in February).

- Indeed some FOMC members have identified the turn-of-the-year price-setting by firms as a key determinant of whether tariff-related inflation is set to be meaningfully passed through.