JGBS: Trading To Resume After Yesterday's Holiday

In post-Tokyo trade on Tuesday, JGB futures closed stronger, +32 compared to settlement levels.

- Overnight, A stronger-than-anticipated US jobs report spurred a slide in US tsys as traders pared bets on Federal Reserve rate cuts in 2026. The yield on 2-year climbed 6bps to 3.51% while that on the 10-year rose 3bps to 4.17%.

- Nonfarm payrolls growth was far stronger than expected in January at 130k (cons 65k) after negligible two-month revisions of -17k (mainly in Nov). Private payrolls saw a larger beat, both with the 172k (68k cons) in January but with also a two-month revision of +49k (fairly evenly split over Dec and Nov).

- The Household survey showed a stronger labor market than expected, with the unrounded unemployment rate of 4.283% not just below the consensus of 4.4% and 4.375% prior, but also the lowest since July.

- MNI: Fed's Schmid - Policy Should Keep Pressure On Inflation. Federal Reserve Bank of Kansas City President Jeff Schmid said Wednesday interest rates should stay at a level where they continue to put some pressure on the economy so that inflation can cool further, while also advocating further efforts to shrink the central bank's balance sheet.

- Today, the local calendar will see PPI and Tokyo Avg Office Vacancies data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Sell-Off Post Strong QSBO, NZ-AU 10Y Diff UP

NZGBs are 4-5bps cheaper after the release of the Q4 QSBO Survey.

- The Q4 NZIER (New Zealand Institute of Economic Research) Quarterly Survey of Business Opinion (QSBO) printed a little while ago and showed a strong improvement versus the Q3 result. This should increase confidence in the economic recovery taking hold in 2026 and adds to the case for a steady RBNZ hand in the near term (at the margin).

- US tsys finished slightly weaker on Monday amid uncertainty over future Federal Reserve independence. This after the DOJ announced it's investigation of Fed Chairman Powell over the weekend related to his testimony before the Senate Banking Committee last June.

- With US tsys only modestly cheaper overnight and ACGBs little changed, the NZ-US and NZ-AU 10-year yield differentials are 2bps and 4bps higher, respectively.

- Consistent with the move in the NZ-AU 10-year differential, market expectations for the NZ-AU policy rate differential over the next year, as reflected in the AU–NZ 1-year forward 3-month swap (1Y3M) spread, has increased ~8bps versus Friday’s closing level.

- Swap rates are 2-5bps higher, with the 2s10s curve flatter.

- However, RBNZ-dated OIS pricing is, so far, little changed across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

Bloomberg Finance LP

US: Trump - 25% Tariff On Any Countries Doing Business With Iran

US President Trump has posted via Truth Social that any country doing business with Iran will be charged a 25% for all of the business they do with the US. The full Truth Social post is outlined below, with no timeline of when this comes into effect. At face value this could impact economies like India and also China. The move follows comments from Trump yesterday where he stated the US was considering its options around Iran, in the wake of protests (which overnight Iran claimed were being bought under control). However, it was also floated that there is the possibility of a meeting between the two countries. Via BBG/Axios: "Axios earlier Monday reported Araghchi and Witkoff discussed a potential meeting. The report, citing anonymous sources, described the move as an effort by Iran to deescalate tensions with the US or buy more time before Trump decides whether to take military action."

- "Effective immediately, any Country doing business with the Islamic Republic of Iran will pay a Tariff of 25% on any and all business being done with the United States of America. This Order is final and conclusive. Thank you for your attention to this matter!"

JPY: USD/JPY - Dips Remain Supported, Trying To Gain Momentum Above 158.00

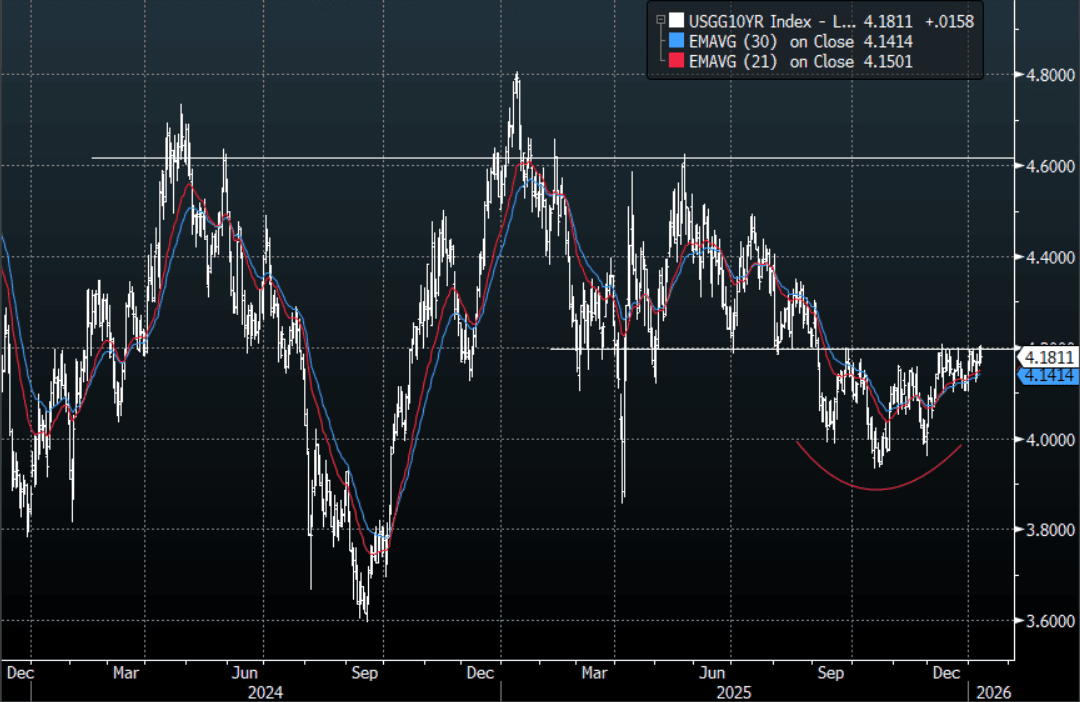

The overnight range was 157.68 - 158.20, Asia is currently trading around {USDJPY Curncy}. USD/JPY chopped around 158.00 in a relatively contained range. The BOJ is in a tough spot, and they are going to need to do something significant to turn around the market's perception of a weak Yen. A test of the BOJ/MOF resolve looks inevitable at the moment as the market moves its focus back toward the important 160.00 area. USD/JPY remains in an uptrend and while the support back toward the 154.00-155.00 area is intact it remains a buy on dips. In today's Asian session, look for dips back toward 157.50 to remain supported initially, should this 157.00-157.50 area fail to hold it could signal a pullback. I suspect we will get more official jaw-boning as we approach 160 and any move above there would dramatically increase the chances of them getting involved. US yields are also approaching some pivotal levels a break above 4.20% in the 10-year could also provide further headwinds for the Yen, see Graph below.

- Bloomberg - “Mizuho Bank’s Masayuki Nakajima. “From Tuesday onward domestic long-term interest rates are likely to face upward pressure, with selling bias prevailing in the government bond market,” he wrote in a note. “Overall, reports of a possible dissolution are likely, in the short term, to act as a catalyst strengthening the combination of ‘higher stock prices, a weaker yen, and higher interest rates’”

- Options : Close significant option expiries for NY cut, based on DTCC data: 157.00($535m), 157.50($537m), 158.50($647m). Upcoming Close Strikes : 158.00($1.84b Jan 16), 160.00($3.74b Jan 16) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 80 Points

- Data/Event : BoP Current Account Balance, Eco Watchers Survey Current

Fig 1 : US 10-Year Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P