JAPAN DATA: Tokyo CPI Above Expectations, Services Inflation Edges Up

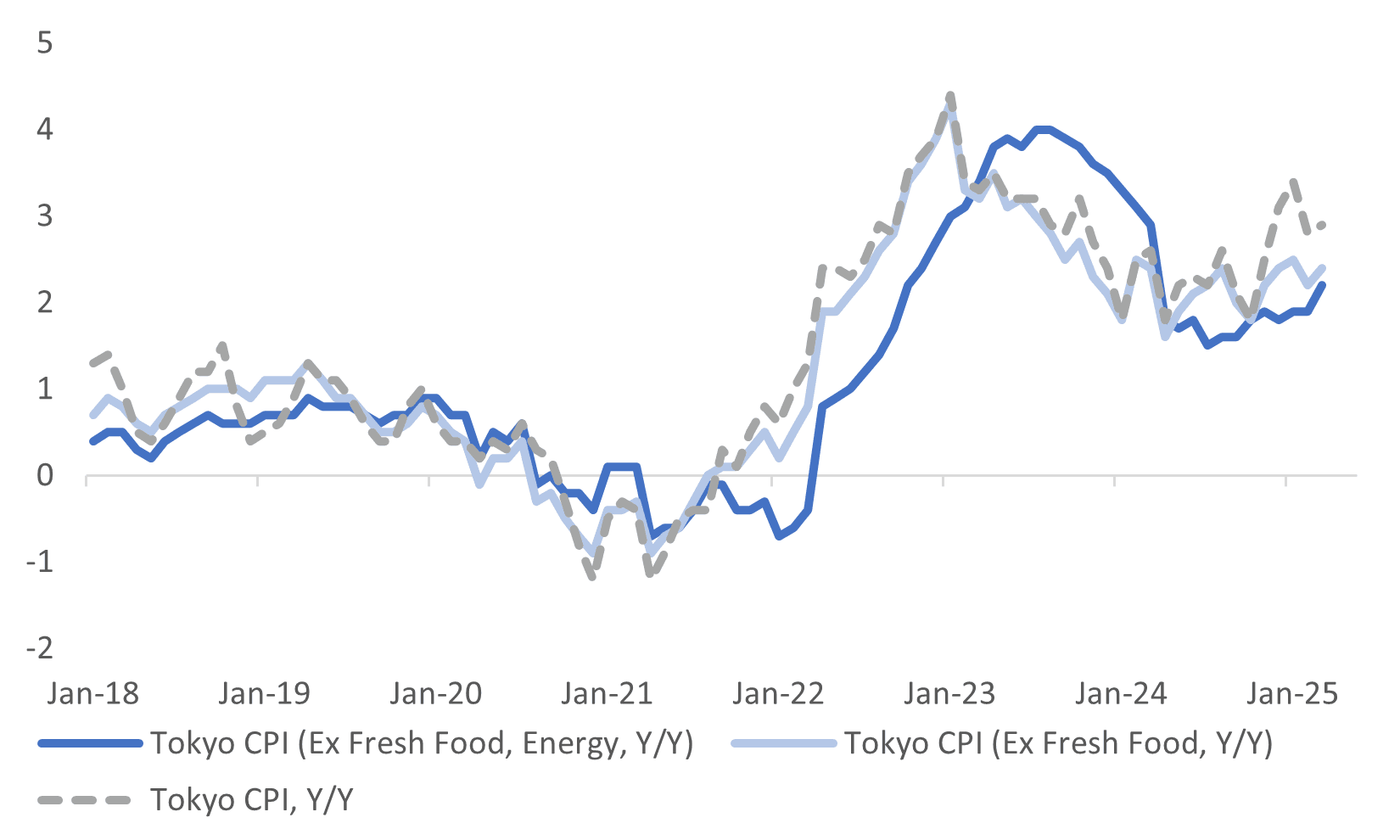

The Tokyo March CPI printed above market forecasts. The headline rose 2.9%y/y, versus 2.7% forecast. The prior month was revised down a touch to 2.8% (initially reported as a 2.9% rise). The ex fresh food measure was also above expectations at 2.4%y/y (2.2% was the forecast, which also the Feb read). The ex fresh food and energy measure rose 2.2%y/y, against a 1.9% forecast.

- The chart below plots these three metrics, all in y/y terms. The core print, ex fresh food, energy has been steadily rising and should add marginally to the BoJ's confidence around achieving its 2% target in the second half of the outlook period.

- In m/m terms, the headline rose 0.3%, while the core components were also positive m/m, reversing softer trends seen in Feb. Goods and services prices rose 0.3%m/m (seasonally adjusted). The core measure which excludes all food and energy was up 0.4%m/m, the firmest rise since August last year (but this data is not seasonally adjusted).

- By segment, food prices were up 0.3%m/m, after the Feb -0.9% fall. Fresh food prices were still down m/m. Other segments were mostly positive and firmer than Feb's pace. Notable was the 1.1%m/m rise in entertainment prices, while utilities rose 0.5%m/m, after Feb's sharp fall (due to govt energy subsidies). Clothing and footwear was up 1.6%m/m as well. Services prices increased 0.8% from the prior month's 0.6%.

Fig 1: Tokyo CPI Trends Y/Y - Firmer In March

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: ACGB Apr-37 Auction Result

The AOFM sells A$800mn of the 3.75% 21 April 2037 bond, #TB144:

- Average Yield (%): 4.4666 (prev. 4.3459)

- High Yield (%): 4.4675 (prev. 4.3475)

- Bid/Cover: 3.6688x (prev. 3.2188x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 59.2 (prev. 43.7)

- Bidders: 41 (prev. 34), successful 12 (prev. 14), allocated in full 4 (prev. 7)

LNG: European Prices Lower But Market Remains Vulnerable To Supply Disruptions

Natural gas prices were mixed on Tuesday with Europe sharply lower but the US higher. European gas fell 6.7% yesterday to EUR 43.99 to be down 17.4% this month. It reached a peak of EUR 59.39 on February 11 but has been trending lower on hopes of peace in Ukraine allowing the use of Russian pipeline flows again but a lot has to happen before sanctions will be eased. Also with prices high and storage at below-average levels, German utility Uniper SE has suggested reducing refilling targets to 80% ahead of next winter (Bloomberg).

- Cold weather and lower wind-driven power resulted in significant inventory drawdown but more recent higher-than-average temperatures have allowed Belgium and France to add slightly to storage, according to Bloomberg. Prices remain elevated though and the market remains vulnerable with significant flows needed to restock ahead of next winter.

- Ukraine’s largest private energy firm DTEK is negotiating LNG import agreements. Supplies will mainly come from the US but also the Middle East (Qatar is a major LNG exporter), according to Bloomberg. The gas would be used to fill its storage facilities, which Europe uses, and would transit through ports in Germany and eastern Europe.

- US natural gas rose 4.7% on Tuesday to $4.18 to be up 37.4% in February. Buyers were attracted to the market following Monday’s 6% fall, which was driven by forecasts for milder weather. The Commodity Weather Group is projecting higher temperatures across much of the US in early March.

- Oil markets have worried about the strength of China’s demand for some time given the lacklustre economic outlook. China has imposed tariffs on US oil and LNG imports but its overall LNG imports were around 13% below the 5-year average according to ANZ.

AUSSIE BONDS: ACGB Apr-37 Supply Faces A Higher Yield & Steeper Curve

Bidding at today’s auction of A$800mn of the 3.75% 21 April 2037 bond is likely to be shaped by several key factors:

- The outright yield is roughly 10bps higher than at the previous auction but remains about 30-35bps below the November 2024 peak.

- The 3/10 yield curve is around 15bps steeper than the previous auction and sits near its steepest level since August 2022.

- Sentiment toward longer-dated global bonds has improved over recent weeks, as reflected in the US 10-year Treasury yield, which is currently 50bps below its recent highs.

- Notably, this bond is included in the XM futures basket, which may lend additional support to demand.

- Overall, firm pricing is still anticipated at today’s auction, given the higher yields and other favourable factors.

- Results are due at 0000 GMT / 1100AEST.