US-JAPAN: Takaichi: Confirmed Close Cooperation & US Visit In Trump Call

Japanese PM Sanae Takaichi posts on X following a phone call with US President Donald Trump: "We confirmed the close cooperation between Japan and the United States under the current international situation. At President Trump's invitation, we also concurred to coordinate in detail to realize my visit to the United States this spring. The call was extremely meaningful as we reaffirmed the close coordination of the Japan-U.S. Alliance at the beginning of the new year. I look forward to working with President Trump to make 2026 a year in which we carve out a new chapter in the history of the Japan-U.S. Alliance."

- As noted in an earlier bullet (US-JAPAN: Kyodo-Trump & Takaichi To Hold Call Today), the Japanese gov't has been keen to secure a visit to the US for talks with Trump ahead of the US president's trip to Beijing in April.

- The deterioration in Sino-Japanese relations was exemplified on 31 Dec, when the annual trip of ~200 Japanese CEOs to Beijing, due to start 20 Jan, was called off for the first time in 13 years. In a statement, the Japan-China Economic Association said, “Under the current state of Japan-China relations, we have made sustained efforts to make this delegation a reality. However, we have found it difficult to secure sufficient exchanges with Chinese government agencies, including meetings with national leaders.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Roundup: Deutsche Bank, Citigroup on Tap

- Date $MM Issuer (Priced *, Launch #)

- 12/03 $Benchmark Deutsche Bank 6NC5 +115a

- 12/03 $Benchmark Citigroup PerpNC5 7.125

- 12/03 $Benchmark Protective Life +3Y +90a

- 12/03 $500M Freedom Mortgage 5.5NC2.5

- $5.85B Priced Tuesday, $23.6B/wk

BONDS: EUREX ROLL (Updated)

- Buxl: 54%.

- Bund: 57%.

- Bobl: 77%.

- Schatz: 65%.

- BTP: 63%.

- BTS: 80%.

- OAT: 68%.

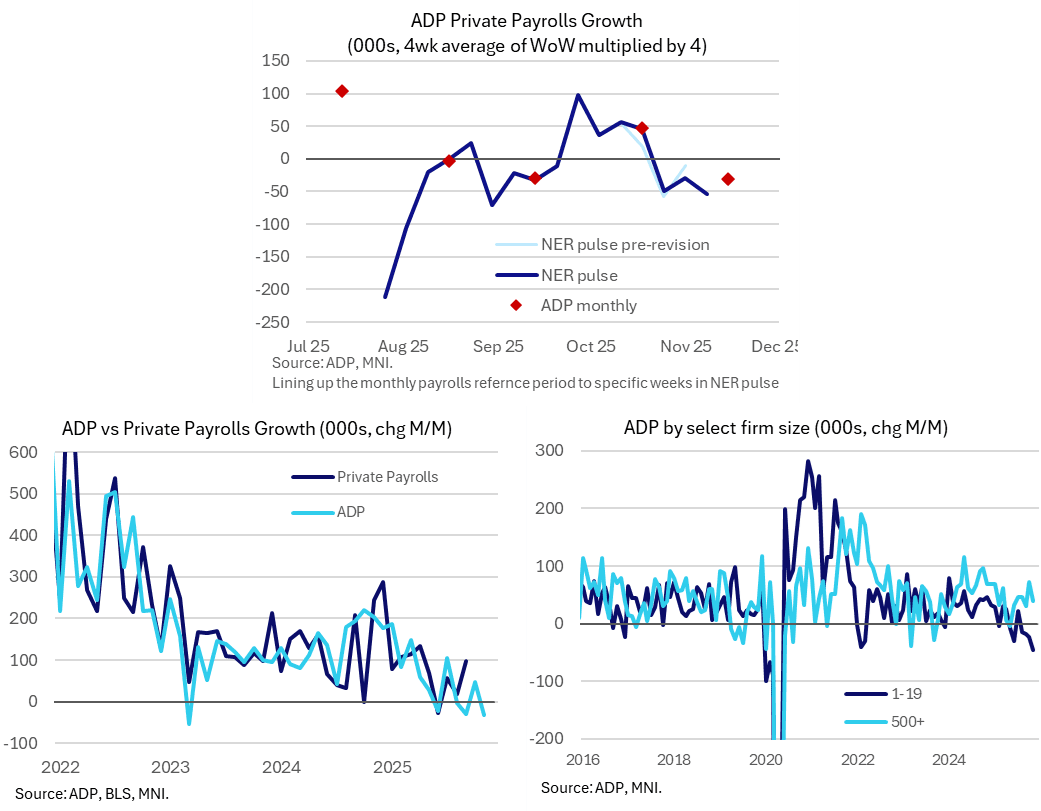

US DATA: No Real Surprises For ADP As Confirms Return Of Declining Employment

The monthly ADP report in November turned out closer to the weakness implied by its own weekly tracker than Bloomberg consensus which had surprisingly eyed a small increase on the month. It confirms a return to a monthly decline in private employment, with a third decline in the past four months.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- However, as noted in our preview this morning, this had looked an odd consensus figure considering last week’s ADP NER Pulse update saw an average weekly change of -13.5k in the four weeks up to Nov 8, i.e. closer to a -55k decline on a rolling monthly basis.

- In theory, this monthly report should have offered limited new information from that in the weekly series as, broadly mimicking the BLS payrolls report, its reference period is the week including the 12th of the month.

- As we wrote: “The weekly series is prone to revisions although we’d be surprised if they were strong enough to materially alter a weak trend that has seen three weeks averaging -11k (on the same four-week rolling basis, i.e. closer to -45k in monthly terms). “

- Further, the previous current vintage for the weekly tracker had pointed to a ~46k increase back in October so today’s modest upward revision also chimes there.

- Back to today’s monthly report, smaller firms clearly felt pressure in November, with -46k for those with 1-19 employees and -74k for those with 20-49. The offsetting 90k increase elsewhere was led by a 39k increase for those with 500+ employees after a strong 73k increase for the latter in October.

- From today's press release (link): "Job creation has been flat during the second half of 2025 and pay growth has been on a downward trend. November hiring was particularly weak in manufacturing, professional and business services, information, and construction.

- * Hiring has been choppy of late as employers weather cautious consumers and an uncertain macroeconomic environment. And while November's slowdown was broad-based, it was led by a pullback among small businesses."

- The broader momentum in the series should be viewed as an important indicator for jobs growth, with the three-month average slowing through the year to date (200k in Dec 2024, 139k in Mar, 22k in Jun, 24k in Sep and -4k most recently in Oct).