ASIA STOCKS: Taiwan Inflow Momentum Slows, Indonesia Inflows Continue

Outside of Indonesia, net equity flow trends were mostly negative yesterday. Outflows from South Korea and Taiwan were relatively modest, but Taiwan now has seen aggregate outflows in the past 5 trading days. This followed a very strong inflow period, whilst the Taiex index has climbed close to record highs. Some outflow pressure may reflect profit taking, with the broader backdrop still seen firm from a tech/AI outlook perspective. In South Korea, the Kospi is struggling to trend higher after consolidating around the 3200 region. Concern around the reform agenda and potential tax changes (relating to stock investments) have been factors driving a more cautious backdrop.

- In South East Asia, Indonesian inflows continued, with the last 5 trading days seeing $300mn in net inflows. This comes as the local JCI index reached fresh record highs yesterday. Broader risk tones, amid Fed easing hopes, have helped market sentiment. Today we have President Prabowo Subianto delivering the annual state of the nation address. The 2026 budget speech will also take place. The market will be looking for signs that the fiscal outlook is still being managed prudently but at the same time looking to foster firm GDP growth.

- Elsewhere, outflow trends were mostly evident, with the steady net selling of Malaysian stocks still evident.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -26 | 510 | -4467 |

| Taiwan (USDmn) | -122 | -64 | 4490 |

| India (USDmn)* | -258 | -977 | -12699 |

| Indonesia (USDmn) | 51 | 300 | -3414 |

| Thailand (USDmn) | -17 | -220 | -1919 |

| Malaysia (USDmn) | -25 | -129 | -3314 |

| Philippines (USDmn) | 2 | 31 | -594 |

| Total (USDmn) | -395 | -548 | -21918 |

| * Data Up To Aug 13 |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

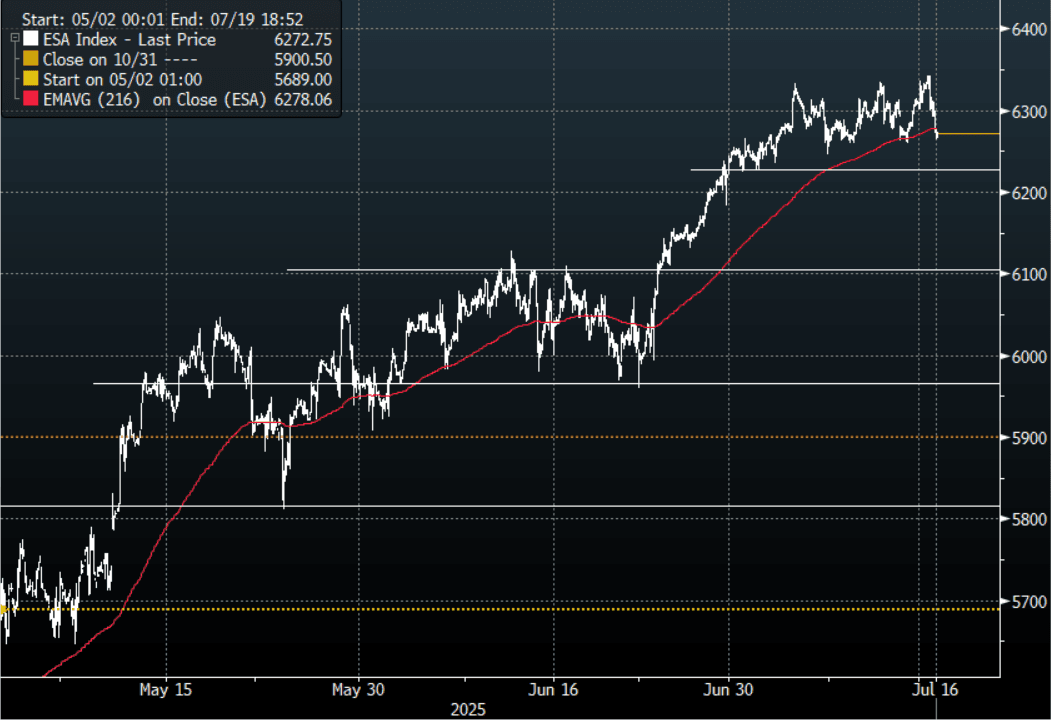

US STOCKS: Big Reversals Seen Across The Board, Notably Outside Of Tech

The ESU5 overnight range was 6272.50 - 6343.00, Asia is currently trading around 6270. The September contract made new all-time highs and then collapsed as the market interpreted that US CPI showed clear signs that tariffs are beginning to impact the core goods data. This morning has seen US futures open under pressure, ESU5 -0.20%, NQU5 -0.20%. The Price action does not look great with 3 failures now to extend beyond the 6350 area, a break back below 6230/50 could signal a deeper correction back to 6000/6100. Huge reversals in the broader market outside of tech, Russell -1.99%, Dow Transports -1.63%, Regional Bank Index -3.74% points to this weakness potentially having more to play out.

- Callum Thomas on X: "Deploy the Cash" Fund manager cash allocations drop to multi-year lows...”

- Lance Roberts(RIA): “Our most significant concern for Q2-2025 earnings and the rest of the year is slowing economic growth, which will spill over into consumer spending. There is a high correlation between Personal Consumption Expenditures (PCE) and earnings. To wit: “One of the better measures for developing a framework for future earnings growth is personal consumption expenditures (PCE), since they comprise nearly 70% of the economic equation. The annual percentage change in forward earnings tracks the yearly percentage change in PCE fairly closely. Given the recent softness in the employment data and the downturn in PCE, the risk to earnings is rising.”

- Andreas Steno Larsen on X: ”If it wasn’t for the word “tariffs”, literally no one would care about the level of goods inflation we saw today. No one - this will pass to”

- (Bloomberg) -- The S&P 500 Index closed lower for the second time in three sessions on Tuesday, weighed down by financial companies as mixed earnings results from banks offset an upbeat report showing consumer prices are cooling.

- Short-term this is starting to look a little overdone with topside momentum having stalled above 3300 could we now get a healthy reversion back to the mean. First support is back towards the 6000/6100 area.

Fig 1: SPX(ESU5) Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: ACGB Mar-36 Supply Faces Higher Yield With A Similar Curve

The Australian Office of Financial Management (AOFM) will today sell A$800mn of the 4.25% 21 March 2036 bond. The line was last sold on 30 May 2025 for A$1200mn. This new line was sold by syndication on 5 February 2025 for A$15.0bn. Bidding at today’s auction is likely to be shaped by several key factors:

- The outright yield is roughly 10-15bps higher than the previous auction level and about 10bps below the late February peak.

- However, the 3/10 yield curve is slightly flatter than the previous auction level and sits around 20bps flatter than its recent high.

- On the other hand, sentiment toward longer-dated global bonds has deteriorated over recent weeks.

- However, this bond is included in the XM futures basket, which may support demand.

- Overall, firm pricing is still anticipated at today’s auction, given the higher yields and other favourable factors.

- Results are due at 0200 BST / 1100 AEST.

ASIA STOCKS: Taiwan Inflows Buoyant Amid Tech Optimism, Outflows In India & SEA

Positive inflow momentum was a standout for Taiwan and South Korean markets yesterday. Sentiment around the AI/tech space was boosted by Nvidia resuming sales of a key chip to China (which was part of the broader US/China trade truce). Taiwan remains the best performer, with just under $1.8bn in net inflows in the past 5 trading days. Month to date, Taiwan has seen over $4.5bn in inflows. Tech equity bourses outperformed globally in Tuesday trade, although the firmer US yield backdrop (post the CPI outcome, which showed tariff effects emerging), has tempered sentiment in this space.

- Elsewhere, trends were mostly softer, with India unable to sustain a positive bounce from the end of last week.

- Recent positive momentum into Thailand cooled.

- Indonesian markets also continued to see outflow pressures, now at over $350mn in July to date. The overnight news of a 19% tariff deal with the US may help stabilize sentiment, at least on a relative value basis with tariff rates elsewhere in the region mostly higher.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 203 | 840 | -8137 |

| Taiwan (USDmn) | 710 | 1796 | -1395 |

| India (USDmn)* | -92 | -406 | -8420 |

| Indonesia (USDmn) | -20 | -108 | -3591 |

| Thailand (USDmn) | -18 | 97 | -2341 |

| Malaysia (USDmn) | -21 | -76 | -2813 |

| Philippines (USDmn) | -6 | -8 | -556 |

| Total (USDmn) | 756 | 2136 | -27254 |

| * Data Up To July 14 |

Source: Bloomberg Finance L.P./MNI