CNY: Stronger CNY Fix Triggers Best CNH Session in Six Weeks

Oct-09 11:23

In contrast with the stronger USD trade today, the CNH is outperforming, with USD/CNH holding close to daily lows headed into the NY crossover. Moves follow the far stronger-than-expected CNY fix overnight (fixed at 7.1102 vs. Exp. 7.1458) - helping trigger the downside in USD/CNH and snap the past 5 sessions of gains.

- The higher-than-expected CNY fix is likely use of the counter-cyclical factor to lean against the recent upleg in USDCNY, but may also be looking to partially address and offset the capital inflow pressures emanating from the local equity rally: the Shanghai Comp surged to 3937 overnight, the highest since 2015.

- Commerzbank wrote earlier this week that they expect USDCNY to trade in the 7.10-7.15 range into year-end, a revision from their prior expectation of 7.20-7.30 previously. Similarly, Goldman Sachs see CNY as deeply undervalued, and gradual strengthening is likely. They roll forecasts to 7.00 for year-end and 6.90 in six- and twelve-months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - S&P E-Minis Bull Cycle Intact

Sep-09 11:21

- In the equity space, a bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a 2.00 projection of the Apr 7 - 10 - 21 price swing. Initial support to watch is 6456.35, the 20-day EMA.

- A corrective bear cycle in EUROSTOXX 50 futures remains in play. Recent weakness resulted in a breach of 5368.87, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, initial resistance to watch is 5377.49, the 20-day EMA. It has been pierced, a clear break of it would be a bullish development.

US TSYS: Off Yesterday’s Highs With Payroll Revisions and 3Y Supply Ahead

Sep-09 10:51

- Treasuries are mildly cheaper overnight, gently pushing back against yesterday’s bull flattening but comfortably within yesterday’s ranges.

- Today is highlighted by preliminary benchmark payrolls revisions at 1000ET (MNI Preview link), added attention on Trump administration BLS criticism, 3Y supply and then broader Trump comments. The docket will be seen in light of PPI and CPI coming on Wed and Thu respectively.

- Cash yields are 1.2-1.9bp higher on the day, with increases marginally led by 30s.

- Curves are marginally steeper but broadly consolidate yesterday's second day of flattening, including 5s30s at 113.9bp vs a briefly seen post-NFP high of 126.9bp (multi-year steeps).

- TYZ5 trades at 113-15+ (-02) off earlier lows of 113-11, on limited overnight volumes of 250k.

- Friday’s post-payrolls high of 113-21+ still carries weight having hit another fresh short-term cycle high. It marks the next resistance level after which lies 113-26+ (2.764 proj of Jul 15-22-28 price swing) whilst support is seen at 112-28+ (Sep 5 low).

- Data: Preliminary benchmark payrolls revision (1000ET).

- Coupon issuance: US Tsy $58B 3Y Note auction - 91282CNY3 (1300ET). Last month’s 3Y saw another small tail of 0.7bp although the bid-to-cover firmed a touch from 2.51 to 2.53.

- Bill issuance: US Tsy $85B 6W bill auction

- Politics: Press briefing with WH Press Sec Leavitt (1300ET), Trump participates in swearing-in ceremony for US Ambassador to Portugal (1600ET), Trump signs proclamation (1630ET)

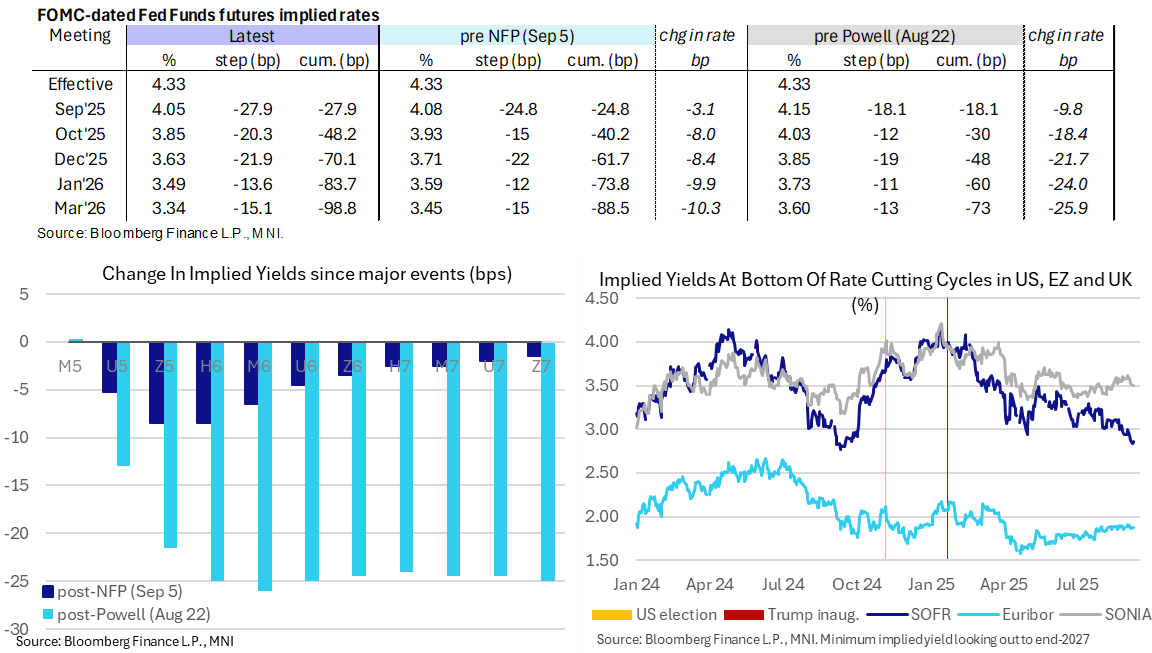

STIR: 70bp Of Fed Cuts Seen To Year-End With Payroll Revision Estimate Eyed

Sep-09 10:31

- Fed Funds implied rates are 1.5bp higher on the day for end-2025 rates, pulling a little further away from fully pricing three consecutive rate cuts, but remain within post-NFP ranges ahead of payrolls benchmark revisions at 3pm.

- Cumulative cuts from 4.33% effective: 28bp Sep 17, 48bp Oct, 70bp Dec, 83.5bp Jan and 99bp Mar.

- The SOFR implied terminal yield of 2.86% (SFRH7) is 2bp higher on the day after yesterday saw a fresh lowest close since Sept 2024 (when it saw cycle lows in the high 2.7s), hovering just shy of 150bp of cuts ahead from current levels.

- Today’s US macro docket is headlined by the preliminary estimate for payrolls benchmark revisions at 1000ET. There’s a wide range of estimates here but we judge the median expectation to be circa -750k. MNI Preview: https://media.marketnews.com/US_Prelim_Benchmark2025_Preview_f1d718139b.pdf

- On a related note, the WSJ reports that advisers to President Trump are preparing a report laying out alleged shortcomings of the BLS’s jobs data including revisions.

- Tomorrow (Sep 10), the Senate banking committee will vote to approve CEA's Miran for the Fed Board of Governors at 1000ET. He would still have to be approved by the full Senate to be fully confirmed but this is moving quickly enough to assume that he will be at the FOMC table at the Sept 16-17 meeting.