ASIA STOCKS: Stocks Flop on Oil Jump, Divergence in AI Stocks Key Theme

The Hang Seng Index is navigating a volatile risk-off day prior to May day break, down approximately...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Yields Slump With Global Trend, RBA Highlights Uncertain Outlook

Futures are holding around session highs, up 9bps for 10yr, 7bps for the 3yr. A generally positive futures backdrop from US and JGB moves likely aiding Aussie futures so far today. After a very strong sell-off in March to date we are consolidating somewhat into month. Some optimism around a potential end to the Iran conflict also emerged from a WSJ article, which stated Trump could end the war without re-opening the Strait of Hormuz. This has likely aided the bid in both bond and equity futures, although a lot will depend on oil prices (which are around steady so far today) and when actual flows through the Strait improve noticeably.

- Bonds futures for the 10yr, around 94.99, and 3yr at 93.325 are still under key resistance levels. 95.653 for the 3yr represents the 23.6% retracement for the downleg posted off the October high on the continuation contract.

- ACGB yields are down sharply, off 5.5-10bps, led by the back end of the curve. The 3yr is back to 4.64%, the 10yr around 4.975%.

- The 3/10s curve is slightly flatter at +33bps. The AU-US10yr spread remains within recent ranges at +66bps.

- The March RBA meeting minutes gave more detail around the different Board views on the timing of further monetary tightening. Part of the decision to hike was centred around showing its “clear commitment to returning inflation to target”. It appeared key to the decision that excess demand increased and the labour market tightened since the February meeting while “inflation remained too high”. The next decision is 5 May and the Board agreed that it wasn’t “possible to predict the future path” of policy given current heightened uncertainty.

- Tomorrow we get the Mar final S&P manufacturing PMI along with Feb building approvals.

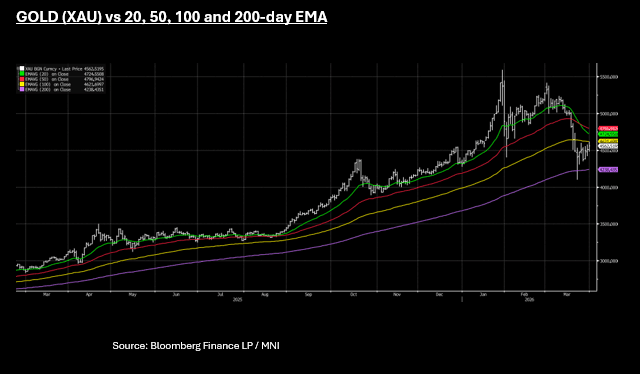

GOLD: Gold Back Above $4,500 as UST Yields Cool

- Gold is up Tuesday as US yields continue to subside on Federal Reserve comments that eased rate-hike bets and a report suggesting that US President Donald Trump is willing to end the Iran war without reopening the Strait of Hormuz.

- Gold has consolidated back above $4,500 with a +1.1% gain during the Asian trading day.

- Currently near US$4,561 / 4562, gold remains between the 100-day EMA of $4,621 and the 200-day EMA of $4,238.

BBG reports that the ongoing outflows from Gold ETFs sees a monthly decline of near 3%, the largest in over 3 years. The report shows that gold historically goes onto deliver credible gains in the months thereafter.

BONDS: NZGB Yields Follow Global Trend Lower, ANZ Survey Flags Stagflation Risks

NZGB yields have tracked lower through Tuesday trade. Benchmarks are down around 5-6bps, with fairly uniform moves across the curve. This follows the sharp move lower in UST yields on Monday, which has continued today, with a further 2-2.5bps in yield losses. Sentiment has been impacted by a WSJ story in which Trump has reportedly told his advisors that the US can exit the war with Iran without re-opening the Strait Of Hormuz. Risk appetite is better, although mostly in the US equity futures space, oil benchmarks are around flat for the session, while the USD is close to unchanged in index terms.

- For the NZGB 2yr we are now close to 20bps off recent March highs (last near 3.53%). We are still above all key EMAs but given we started March closer to 3.10% some consolidation is arguably not surprising. The 10yr is back near 4.70%, off around 16bps from recent highs.

- On the data front, ANZ's business survey showed a deterioration in business confidence, activity and outlook in March while inflation indicators were uniformly higher. Business confidence fell to 32.5 from 59.2, lowest since July 2024, while the activity outlook was down to 39.3 from 52.6, softest since August. The uncertainty around the implications of the Iran War and the duration of elevated fuel prices have weighed on the economy at a time of a nascent recovery, which is likely to add to the MPC's sentiment to stay on hold.

- Market pricing for the RBNZ has softened a little, now under 3.00% (last near 2.95%).

- Tomorrow on the data front we have Feb building permits, then home values later on.