EU CREDIT SUPPLY: Stellantis: 3Q25 Deliveries

(STLA; Baa2/BBBneg/NR)

A mixed bag but encouraging signs on key new models.

- Global deliveries increased 13% YoY, in line with BBG consensus.

- NA had 35% growth, with 22% expected. That reflects inventory reduction measures in 2024 and new model shipments.

- Europe grew 8%, also helped by new models, but lagging 13% expected. It flagged LCV weakness again, and lower shipments in some countries.

- Other regions grew 3% in aggregate, largely in line.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGBS: Commerzbank Expect Frequent Use Of New Eurex EU-Bond Future

In light of today’s Eurex EU-Bond future launch, Commerzbank note that “the EU Jul-34 will become cheapest-to-deliver (CTD) in the December contract. Liquidity will be key, as only a highly liquid future will offer the necessary market depth for efficient hedging, arbitrage and positioning. However, note that the open interest for Eurex futures is reported with a one-day lag, while the turnover should be available in real time”.

- Nonetheless, they expect “the future to develop into a frequently used product based on conversations with clients”.

- In terms of valuation, Commerzbank suggest that “the December futures seem fairly priced with implied repo rates (IRRs) trading close to €STR. Given no switch risk in the EU future, its IRR should also trade close €STR”.

GILTS: Bullish Corrective Phase Intact, Cross-Market & Fiscal Drivers Eyed

Gilts look to wider cross-market cues early on Wednesday, rallying as European stocks pulled back from highs, before trimming the rally as fresh demand came into equities.

- Gilt futures trade as high as 91.58 before stabilising around 91.45.

- Initial support and resistance 90.65/91.66, corrective bullish phase remains in play.

- Yields 2bp higher to 1bp lower as the curve twist flattens.

- Domestic focus remains on the run into the late November Budget as PM Starmer reportedly assembles a “Budget Board” focused on pro-growth policies, while Chancellor Reeves has reportedly limited Cabinet colleague access to the Treasury’s emergency funds ahead of the Budget.

- BoE-dated OIS shows ~10bp of easing through year-end after printing below 8bp in recent sessions.

- Little of note on the UK data calendar until Friday’s monthly economic activity readings.

- Today’s supply comes via GBP4bln of the 4.00% Oct-31 gilt.

- That will leave wider macro and geopolitical developments at the fore for much of today, with U.S. PPI data providing the key scheduled risk event and fallout from the Russian drone incursion into Poland eyed.

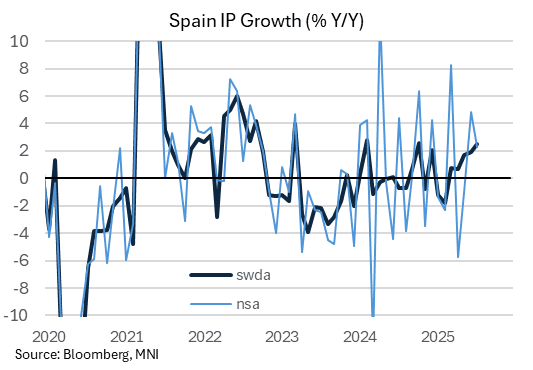

SPAIN DATA: July IP Dragged By Volatile Capital Goods And Energy Production

Spanish headline IP fell 0.5% in July, below the five-analyst strong consensus of -0.2% and June's 0.8% (revised from 1.0%). Energy (-2.7% M/M) and capital goods (-3.6% M/M) production dragged heavily on the print, both can be volatile and often reverse, meaning that underlying trends might be not as poor as the relatively weak sequential headline reading suggests.

- 3m/3m IP growth was 0.7%, as in June (revised from 0.8%), the joint highest reading since December 2024. On a Y/Y comparison, IP read 2.5%, the strongest since October 2024.

- Recall Spanish manufacturing PMI gives a firm outlook for August as it strongly outperformed on that month, quoting "fastest growth of the manufacturing sector since last October [...] output, new orders and employment all rose to stronger degrees compared to July. Expectations were positive that growth will be sustained, although buying activity increased only slightly amid ongoing supply-side challenges".

- Today's Spanish data comes after German July IP was marginally stronger than consensus (at 1.3% M/M) but France saw a setback as some one-off factors reversed (-1.1% M/M). Italy is scheduled for release at 0900BST/1000CEST today, with consensus standing at 0.1% M/M (after +0.2% in June).