CNH: Steadies After Earlier PBoC Announcement, USD/CNH Well Under Key Resistance

USD/CNH sits around 100pips off earlier highs (6.8606), last near 6.8500, as the market digests the earlier changes around FX reverse requirements and vow to keep the yuan basically stable. These moves may help temper recent strong one-sided appreciation pressures. It was also followed up by a steady USD/CNY fixing, which was set +700pips above market forecasts. The largely steady downtrend in the USD/CNY fixing since Dec last year has been a key driver of yuan appreciation expectations, so this will be watched in coming sessions for signs of firmer resistance to yuan gains.

- Still, USD/CNH remains comfortably under all keys EMAs. First resistance looks to be back toward 6.91-94 but it seems unlikely than broader shorts in the pair won't be stressed unless we see a sustained move back above the 7.0000 area (see the chart below).

The reaction in implied vols has been fairly modest, with a tick lower across the benchmarks. The 1wk is around 3.30%, versus recent highs around 4%. The 1mth is around 3.17%, after being above 3.50% recently. - Risk reversals which have been trending higher since the start of the year, and therefore diverging from weaker USD/CNH spot levels, are off recent highs.

- Outside of broader macro watch points, like US Fed outlook, China export growth etc, focus will also be on local exporter FX conversion trends.

- Next week we get PMIs for Feb. The consensus doesn't expect sharp moves relative to Jan outcomes, and in any case PMI prints haven't impact yuan sentiment much in recent months.

Fig 1: USD/CNY Weekly Chart

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

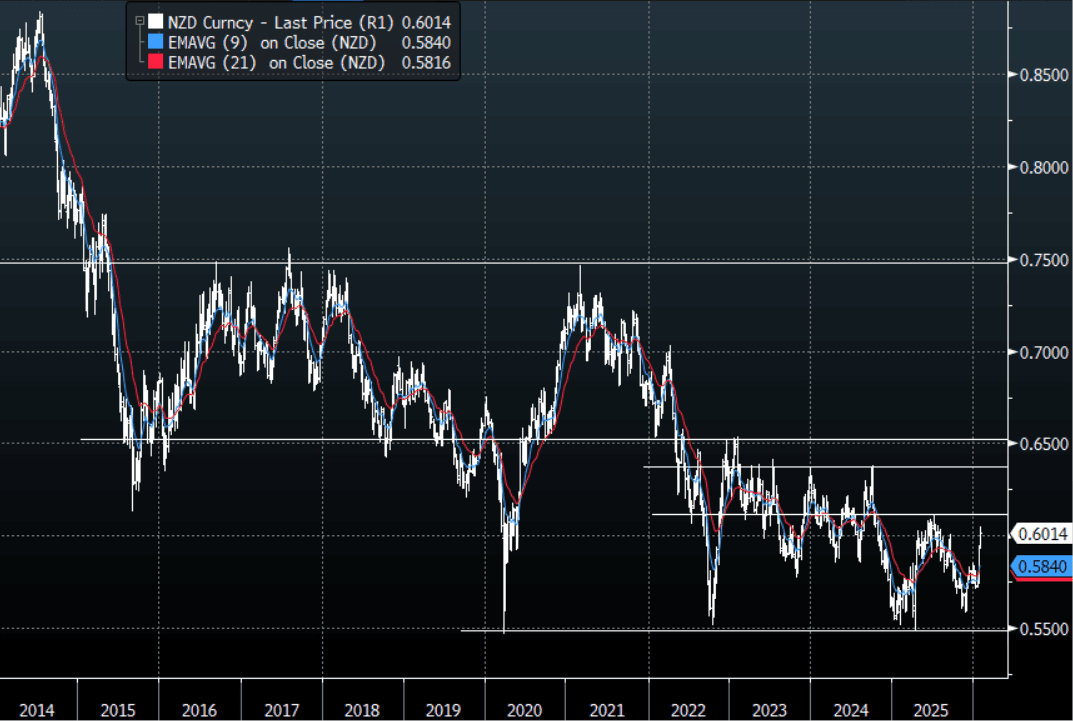

NZD: NZD/USD-Stalls Toward 0.6050 On First Attempt, Dips To Be Supported

The NZD/USD had a range today of 0.6008-0.6049 in the Asia-Pac session, it is currently trading around {NZD Curncy}. The USD looks to be in some real trouble and the Antipodeans will be a huge beneficiary of that. Trump commenting this morning he isn’t concerned by its decline will only add fuel to the fire that they prefer a weaker USD. It looks a little stretched short-term but you would be a brave man to fade this price action. Price has very quickly reached the pivotal 0.6000-0.6100 area and I would expect it to do some work here initially, but a sustained break above 0.6100 starts to potentially open up a move back toward the 0.6400-0.6500 area. Support should now be back towards the 0.5900-0.5950 area looking for a retest of the 0.6100 pivot.

- MNI AU - “Jobs Filled Flat In Dec, After Strong Nov Rise, Y/Y Close To Flat: New Zealand filled jobs for Dec were flat after a revised 0.5%m/m gain for Nov (originally reported as a 0.3% rise). The Nov rise was the strongest outcome since April 2023. This leaves the y/y pace at -0.1%. The data show the improvement in the labour market slowed somewhat in Dec, but this came after a strong Nov outcome. We would expect further general improvements in these trends, given expectations NZ growth improved late 2025 and into early 2026. The outcome is unlikely to shift near term RBNZ thinking..

- Bloomberg - “NZ'S WILLIS: RBNZ WILL BE GUIDED BY DATA, RBNZ WILL 'EASE OFF ACCELERATOR' AT SOME POINT.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5810(NZD327m). Upcoming Close Strikes : none - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 65 Points

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Yields Outperform, NZ-US 10yr Threatens Break Higher

NZGB yields are holding firmer, outperforming in yield terms softer trends elsewhere in the region. JGB and Aussie bond yields are down, likewise for UST yields as well. We are around 3-4bps firmer across the NZGB curve, with moves fairly uniform. The 2yr is around 3.33%, while the 10yr sits at 4.615%, after having breached the 4.60% resistance point. The NZ-US 10yr rate differential is threatening to break higher, last around 39.5bps. The Fed outcome is in focus later.

- NZGBs have largely ignored the softer tone in Aussie yields, which came despite a solid Dec/Q4 CPI backdrop. This has pushed RBA hiking odds for Feb higher. Aussie yield weakness looks reflective of a pause after a strong move higher, rather than the start of a downtrend.

- Earlier data in NZ showed a flat jobs filled outcome for Dec, after a solid rise in Nov. Labour market conditions should gradually improve with better economic growth.

- NZ FinMin Willis stated that, via BBG: "....forecasters are predicting economic growth to continue in 2026 as low interest rates provide stimulus, in response to questions in parliament. “Of course, at some point in the future as the economy strengthens, the Reserve Bank will start to ease of that accelerator a little.”

- 2yr swap rates are edging higher, last just above 2.91%. RBNZ pricing is very flat for the next few meetings.

- Tomorrow, we get Dec trade figures, along with the ANZ Jan activity/business confidence print.

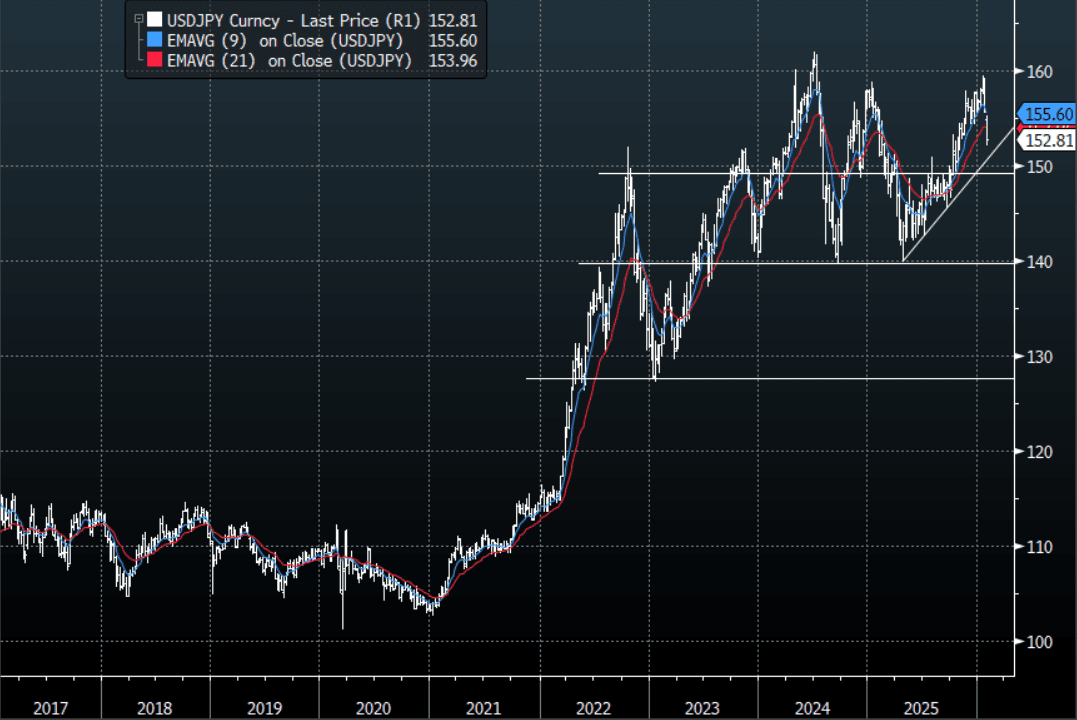

JPY: USD/JPY - Drifts Back Toward 153.00 After Knee-Jerk Move Lower

The USD/JPY range today has been 152.18 - 153.07 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. USD/JPY continues to slide as a leveraged market is forced to pare back large Yen shorts. If the market's take is correct this could be a big deal but as of yet it looks to have been little more than words to me, I feel there will need to be real and active intervention and the participation of the FED would need to be key to give it any real probability of success. For the moment the collapse lower has released a pressure valve causing leveraged funds and CTA’s to have to pare back large JPY shorts, but I suspect unless we get something more significant and clarity around FED involvement dips could remain supported once those shorts have been purged. In today's Asian session, we could continue to see shorter term players and CTA’s continue to reduce, first sell-zone is 153.75-154.25 and then 155.50-1.5600. The price has moved quickly lower and is now approaching its longer-term support, the area between 149.00-152.00 is wide but nothing has really changed and this area should start to offer good risk/reward again for Yen bears again.

- MNI - Dec BoJ policy meeting minutes. Familiar themes were addressed at the meeting (which delivered a 25bps hike). Via BBG: "While the BOJ emphasized that the Dec. 19 hike was due to economic developments moving in line with its outlook, the minutes signaled growing alarm among board members over the impact of the weak yen." Market sentiment wasn't impacted though.

- Bloomberg - “Today’s 40-year JGB sale passed the litmus test with a bid-to-cover ratio slightly above the one-year average and a high yield slightly lower than forecast.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 154.00($727m). Upcoming Close Strikes : 153.75($1.26b Jan 29), 156.00($1.33b Jan 30) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 177 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P