KRW: South Korea To Act If One-Sided Moves Seen in FX

"*S. KOREA: TO TAKE ACTIONS IF ONE-SIDED MOVEMENT IS SEEN IN FX" - BBG A shot across the bow for US...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: Steady Near 6.8300, Onshore Back Tomorrow, Trump Trip Coming Into Focus

China markets remain closed for the final day of the Labor Day break period today, returning tomorrow (onshore markets have been out since last Friday). Spot USD/CNH tracks near 6.8320 in early Tuesday dealings, up from Monday intra-session lows near 6.8150. Broader USD sentiment edged higher as Monday trade unfolded, supported by higher oil prices, as the fragile US/Iran ceasefire threatened to falter (amid strikes on UAE energy infrastructure). The USD BBDXY index finished 0.19% higher for Monday's session.

- For USD/CNH spot, we are sub the 20-day EMA resistance point, which sits near 6.8385. Downside focus will on test of 6.8000, which would take us back to fresh lows for this cycle (we touched 6.8059 back on Apr 14). For now, we are likely to track USD trends, albeit with a continued fairly low beta.

- Tomorrow, when onshore markets return, we have the April RatingDog Services and Composite PMIs due. The market consensus for the services PMI is 52.0, versus 52.1 in March.

- Focus will also start shifting to Trump's planned trip to Beijing (scheduled for May 14-15). Trump stated overnight, via BBG: "“I’m going to go see President Xi in two weeks. I look forward to that,” Trump said Monday during a White House event. “Actually it’ll be a very important trip.”

- This trip also comes as China, from the weekend, ordered companies not to abide by US sanctions; Via BBG: "Beijing has directed companies not to abide by US sanctions on private refiners linked to the Iranian oil trade, including heavyweight Hengli Petrochemical (Dalian) Refinery Co."

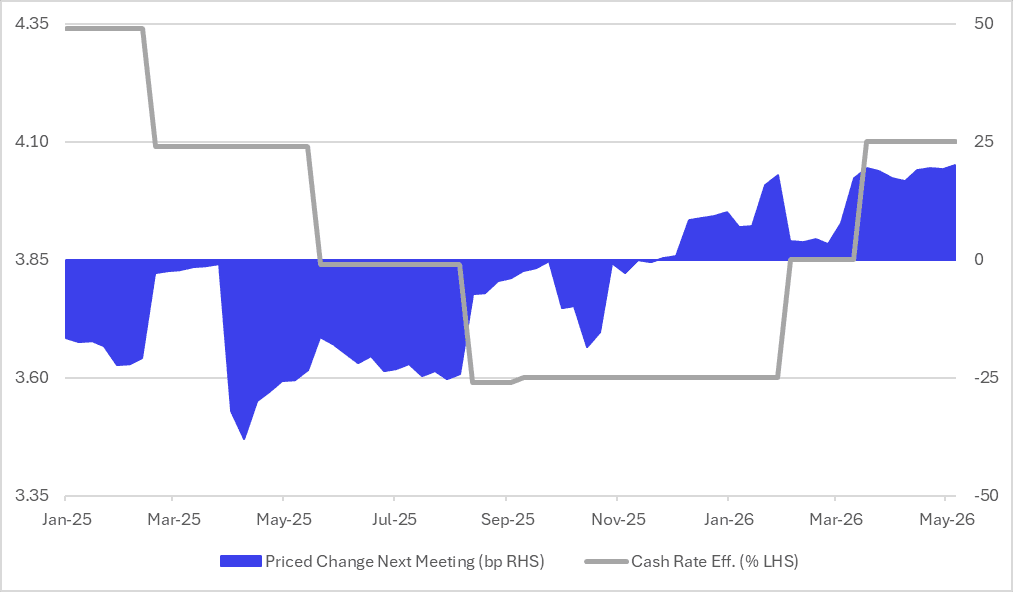

AUSSIE BONDS: Modestly Cheaper Ahead Of RBA Policy Decision

ACGBs (YM -2.5 & XM -3.5) are weaker after US tsys finished 6-7bps cheaper as sentiment soured on Middle East tensions.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +58bps.

- Today, the local calendar will see the RBA Policy Decision.

- The RBA's 5 May decision is expected to be closely contested, with another split vote possible, though most analysts still expect a 25bp hike given persistent inflation, excess demand, and early signs of price pass-through from higher costs linked to the Iran war and Strait of Hormuz disruption.

- Despite some argument for a "wait and see" approach, recent commentary from Deputy Governor Hauser suggests limited confidence that policy is restrictive enough, reinforcing the case for further tightening as firms continue to struggle passing on rising costs. (See MNI RBA Preview here)

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 81% for today to 175% by August and 261% by December 2026.

- Moreover, the market remains more confident about a hike today than it was ahead of February and March 25bp hikes.

- The AOFM plans to sell A$1000mn of the 4.25% 21 March 2036 bond on Wednesday and A$1000mn of the 1.25% 21 May 2032 bond on Friday.

Figure 1: RBA-Dated OIS – Cash Rate V Priced Change Next Meeting

Bloomberg Finance LP / MNI

BONDS: NZGBS: Cheaper With US Tsys As M/E Tensions Rise

NZGBs are 2-3bps cheaper after US tsys finished 6-7bps cheaper across the curve as sentiment sours on Middle East tensions. Early headlines that UAE intercepted missiles saw US tsys extend session lows with equities and gold, while crude and the US$ gained.

- BBC reported an unnamed Iranian military source has warned that all UAE interests could become legitimate targets if Abu Dhabi takes action against Iran, the IRGC linked Tasnim News Agency reported on 4 May.

- U.S. monetary policy is "well positioned" to balance rising risks to the Federal Reserve's maximum employment and price stability goals from tariffs, supply chain disruptions and heightened uncertainty from the Iran war, NY Fed President John Williams said Monday.

- Swap rates are flat to 1bp higher.

- RBNZ-dated OIS pricing is little changed across meetings. 8bps of tightening is priced for May, while February 2027 assigns 102bps.

- The local calendar will see ANZ Commodity Price data, ahead of Wednesday's publication of the RBNZ's Financial Stability Report and Q1 Employment data.

- "New Zealand's unemployment rate likely rose in 1Q as the labor-market recovery sputtered." - BBG

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 1.50% May-31 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.