STIR: SONIA Futures A Little Firmer, BoE Pricing Little Changed

Dec-27 07:49

SONIA futures are flat to +3.0 through the blues. Core global FI markets are in line to a touch above levels seen at the close of Friday’s shortened UK STIR session.

- BoE-dated OIS is little changed to ~1bp softer through ’24 MPC contracts.

- The first 25bp cut is more than fully discounted come the end of the May MPC, with ~145bp of cuts showing through ’24.

- Local headlines continue to focus on the potential for fiscal loosening ahead of the ’24 election, while there has also been increased coverage of late Thursday comments from BoE MPC member Haskel.

- Haskel’s comments read dovishly, particularly when married up to his history of hawkish dissent, although that will have largely been priced in on Friday, in the run up to the Christmas break.

- The local docket is limited in the gap between Christmas and the start of ’24.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Feb-24 | 5.193 | +0.7 |

| Mar-24 | 5.103 | -8.3 |

| May-24 | 4.897 | -28.9 |

| Jun-24 | 4.646 | -54.0 |

| Aug-24 | 4.368 | -81.8 |

| Sep-24 | 4.136 | -105.0 |

| Nov-24 | 3.899 | -128.7 |

| Dec-24 | 3.731 | -145.5 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

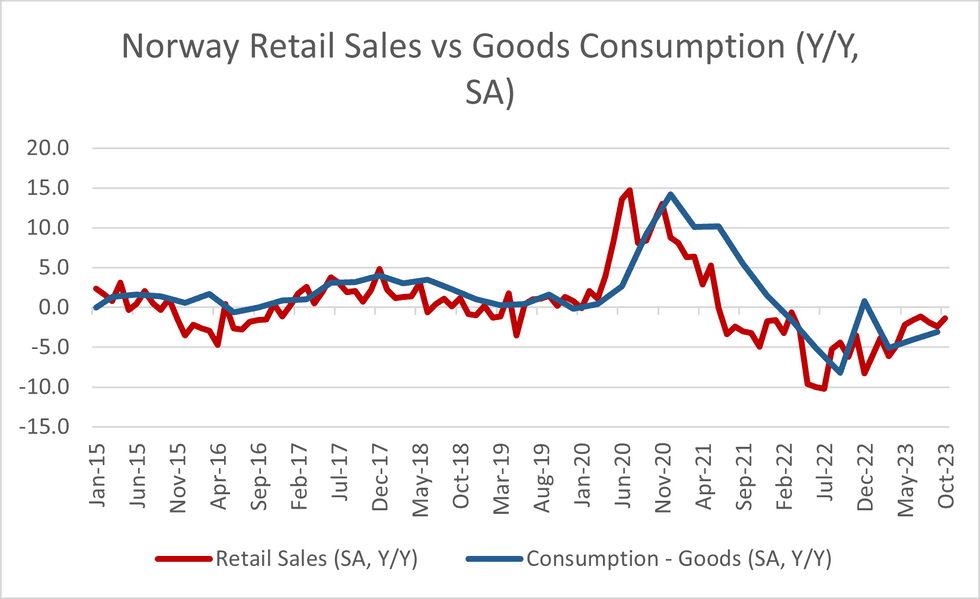

NORWAY: Retail Sales Show Signs Of Returning To Pre-Covid Trend

Nov-27 07:39

Norway SA retail sales for October rose +0.6% M/M (vs. -0.3% prior). The three economists that formed the bbg consensus had expected a -0.2% M/M print. Today's data provides further evidence that the retail sales index is re-aligning with pre-covid trends, as the process of rebalancing the economy back to services persists and we continue to move away from the pandemic-induced increase in goods consumption.

- In Y/Y terms, the index fell -1.4% Y/Y (vs -2.4% prior), an uptick consistent with the goods consumption data in the Q3 GDP release last week. The 3-month index fell -0.8% in the three months from Aug - Oct 2023 (vs +0.6% May - Jul 2023).

- Also released today was Statistics Norway's Index of Household Consumption of Goods, which rose +2.3% M/M in October (vs +0.3% prior). However, this was heavily influenced by a +21.2% M/M rise in electricity/heating fuels consumption, a function of higher electricity prices in October.

- NOK did not react meaningfully to the release, but remains at the top of the G10 to start the week following a positive session in Asia.

USD: In the red across G10s

Nov-27 07:34

- The Dollar traded closer to flat against the CAD, AUD, NZD and the SEK overnight, but stays offered and leans in the red post the Govie cash open despites some small recoveries off the lows in Etsoxx futures.

- It's another Volatile session for the Yen, after USDJPY rallied some 260 pips last week, USDJPY has cleared Friday's low overnight and is now through Thursday's low that was at 148.89.

- Next support is seen further out, towards 148.10/148.02.

BUNDS: A busy week ahead

Nov-27 07:23

- An active week ahead, EU CPIs are back at the forefront, Investors will finish rolling into December for Gilt and Treasuries in the next two days, and they will start rolling/closing their Eurex positions starting in the latter part of the week.

- Govies Month End, although closer to averages for this period in Treasuries, Bond extensions are still decent for the US, small for Europe and a non event for the UK.

- For Bund, support seen last week at 130.13 still holds printed a 130.11 low Friday and 130.16 overnight.

- To the upside, sees 130.46 (small gap) followed by 130.77 initially.

- There's no data on note for today, with EU CPIs starting as off Tomorrow, with Germany and Spain.

- SUPPLY: EU 2027 (equates 13k Bobl), 2033 (equates 14.8k Bund), shouldn't have any impact. US sells $54bn of 2yr, and $55bn of 5yr Notes.

- SPEAKERS: ECB Lagarde in EU Parliament.

Trending Top

Mar-27 20:13