EU CONSUMER CYCLICALS: Sodexo: 1H Results

(SWFP; Baa1/BBB+/BBB+) Net new business negative with retention dropping into low 90s. It has cut F...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

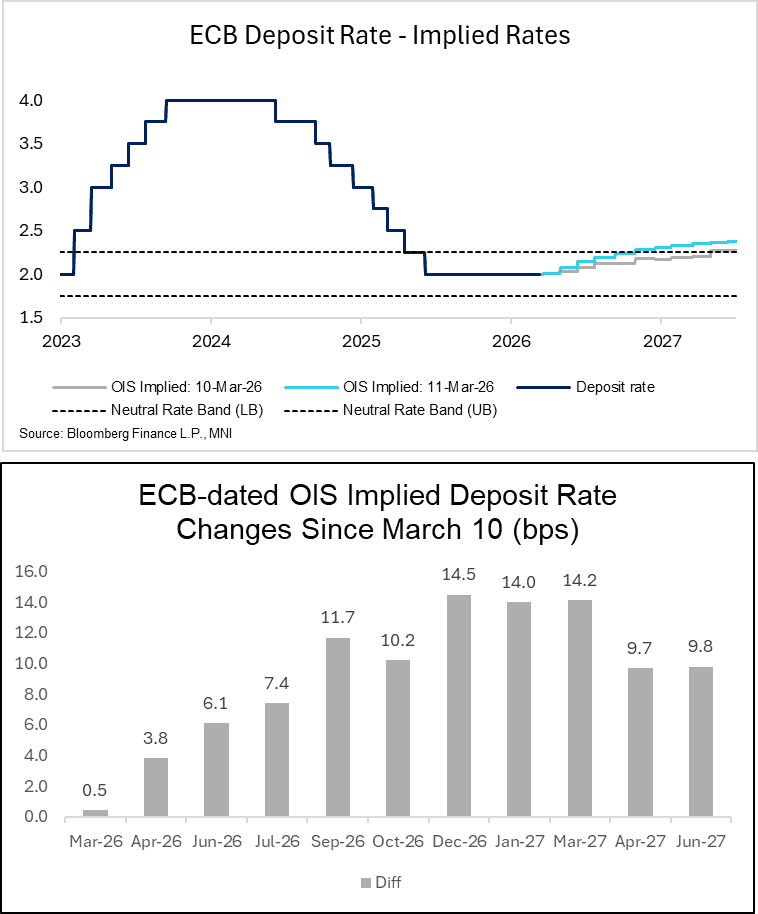

ECB: Hawkish Front-end Repricing As Kazimir Hints At H1 Hike Potential

ECB implied rates rise following comments from Governing Council hawk Kazimir. There are now 31bps of hikes priced through year-end. That's up from 16bps at yesterday’s close, but below the hawkish extreme of 35bps seen in the immediate aftermath of Kazimir's comments.

- Kazimir noted that a rate hike may come sooner than thought, specifically suggesting that the April and June meetings could be in play.

- For now, EUR 5y5y inflation expectations remain close to the 2% target, which pushes back on the need for a knee-jerk ECB rate reaction. More focus will be on the guidance/risk assessment at next week’s decision.

- It remains unclear if the ECB has a “line in the sand” on the level and persistence of medium-term inflation expectations that would warrant a policy response. Governing Council members will also need to account for the growth impact of tighter policy when deciding whether to raise rates.

Summarising comments from ECB officials since yesterday’s close, including from President Lagarde:

- Lagarde: “We are in an economic situation that’s different, we are in a better situation and we have a greater capacity to absorb shocks,” … “We will do all that is necessary to ensure inflation is under control”.

- “We won’t rush into a decision because there is too much uncertainty, too much volatility.”

- She also noted that the ECB would employ scenarios in its March macroeconomic projection report.

- Villeroy: “We have a Governing Council meeting next week — as things stand today, I don’t think we should raise rates now,”

- Kazimir: “For the time being, we need to stay calm,”, though “I’d say a reaction by the ECB is potentially closer than many people think,” …“I don’t want to speculate about April or June. But we will be ready to act if needed.”

- “The balance of risks regarding inflation has clearly shifted to the upside,” ….“We can forget about all the discussions about an inflation undershoot

- “I have no reservations against hiking without new forecasts. What’s clear is that considerations on further cuts are definitely off the table now”

- Kazaks: “"At the moment, I think that the interest rates are still appropriate”… “"If we have concerns that the supply shock, namely the rise in fuel prices due to geopolitical reasons, triggers second-round effects, starts to take root and also raises inflation expectations, then, of course, this intervention by raising rates will be necessary. At this point, it is really not yet visible”

EQUITIES: EU Cash Opening Calls

Estox 50: -1.15%, Dax: -0.90%, CAC: -0.91%, FTSE -0.47%, SMI -1.09%.

STIR: 5bp Of BoE Cuts Priced

Hawkish adjustments in GBP STIRs with core global FI markets on the defensive after some hawkish comments from the ECB Governing Council and a recovery from Tuesday lows in crude oil.

- BoE-dated OIS 2.5-12.5bp less dovish through ’26, showing ~5bp of easing through July. A reminder that as much as ~22bp of tightening was priced through year-end during Monday’s hawkish repricing.

- SONIA futures flat to -11.5, SFIZ6 is still the best part of 30 ticks above Monday’s low. While both SFIZ6/Z7 & SFIZ6/Z8 trade away from this week’s lows.

- BoE’s Breeden will speak in front of the House of Lords Financial Services Regulation Committee this morning, but will cover Stablecoinns, so don’t expect much on monetary policy.

- That will leave geopolitical matters and related oil volatility at the fore.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA (bp) |

Mar-26 | 3.726 | -0.4 |

Apr-26 | 3.696 | -3.4 |

Jun-26 | 3.687 | -4.3 |

Jul-26 | 3.682 | -4.8 |

Sep-26 | 3.695 | -3.4 |

Nov-26 | 3.704 | -2.6 |

Dec-26 | 3.706 | -2.4 |