IRAN: Snr. Official: War Should Lead To New Regime For Control Of Hormuz

Iran's semi-official outlet Tasnim reports : https://tasnimnews.ir/fa/news/1404/12/28/3544580/%D9%82...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: GERMANY ZEW FEB ECONOMIC EXPECTATIONS 58.3

- MNI: GERMANY ZEW FEB ECONOMIC EXPECTATIONS 58.3

- GERMANY ZEW FEB CURRENT CONDITIONS -65.9

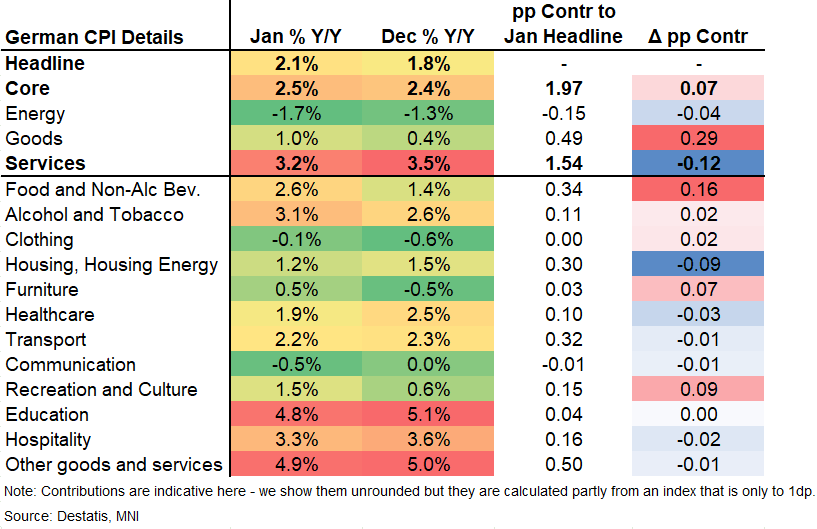

EUROPEAN INFLATION: German Final CPI Confirms Broad-Based Services Slowdown

Final German CPI data, unrevised at a headline level with 0.1% M/M and 2.1% Y/Y, confirms our reading of the state-level data that the January services slowdown was broad-based. This indicates the annual repricing of a large amount of items under the category has been slower than before, an encouraging sign for the ECB's view that services inflation will moderate over the medium term. Separately, German HICP data is available for January but back data details appear to be missing. We'll comment once released in full but for now, the press release notes that HICP inflation was confirmed at -0.1% M/M and 2.1% Y/Y. Turning to CPI details:

- The overall services deceleration to 3.2% Y/Y (from 3.5%) was driven by a wide set of slow-moving categories, while, as we projected after state-level data, volatile airfares (and package holidays) did not "add" to the services slowdown this time.

- Specifically, downward contributions vs December came from stationary healthcare services (-0.03pp, driving the broader healthcare slowdown), lodging away from home (-0.02pp, driving the hospitality slowdown). Insurance (-0.01pp) and services provided by social institutions (-0.01pp) flow into the "other goods and services" category.

- Within hospitality, restaurant inflation interestingly remained at a firm 3.6% Y/Y, implying that the restaurant food VAT reduction by 12pp to 7% has been used to support margins for now. The category remains in focus with potential scope for a slowdown for the Y/Y rate in coming months as some price rises which would have been in the pipeline for later this year could be delayed or skipped as a function of the tax cut.

- The housing and housing energy slowdown was mainly driven by household energy (-0.07pp), partially countered by fuels accelerating a little.

- As projected after state-level data, both categories associated with core goods printed notably firm: Clothing added 0.02pp to headline, and furniture a more substantial 0.07pp. The recreation and culture acceleration was also driven in full by the goods items underlying the category such as audio and IT equipment.

- Food and non-alcoholic beverages meanwhile was the main upside driver in January inflation, the category added 0.16pp as it accelerated to 2.6% Y/Y, the highest since September 2025.

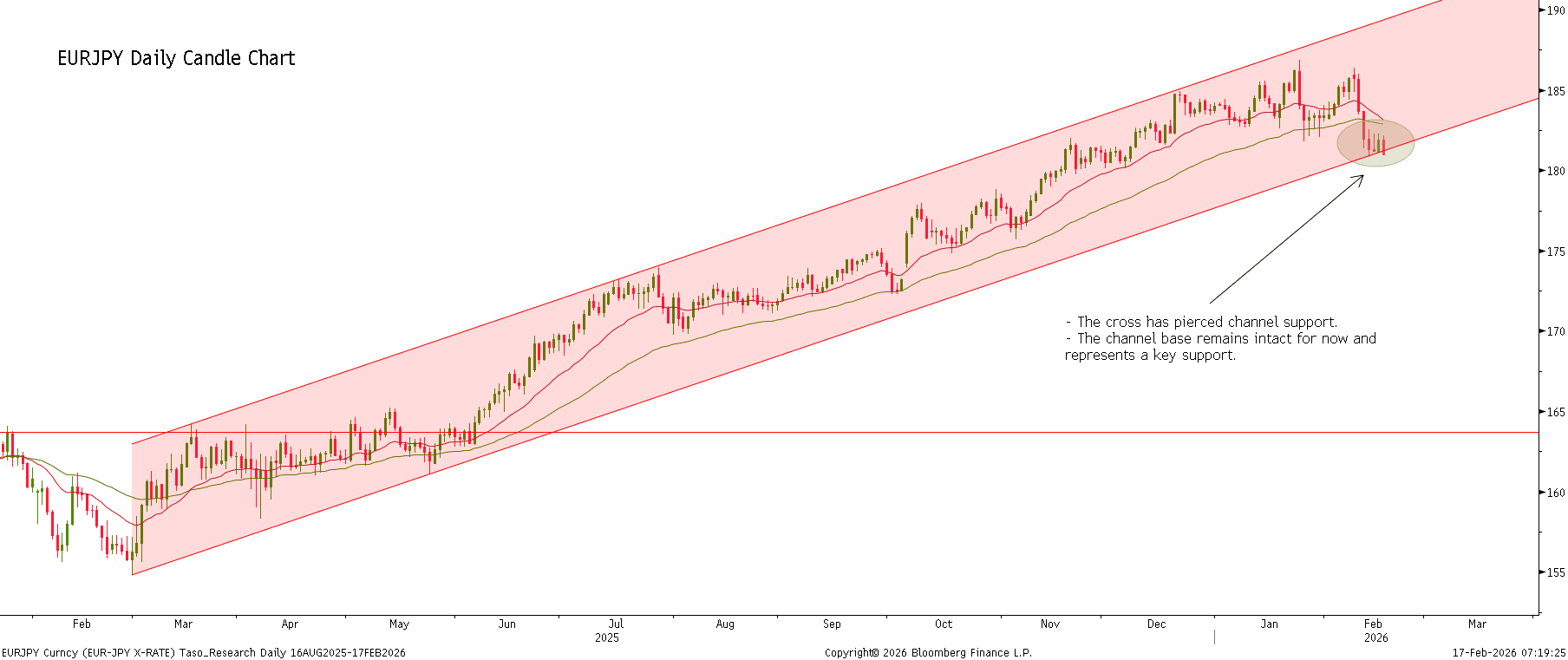

JPY: USDJPY Slips Back Below 153.00, EURJPY Pierces Channel Support

- The Japanese yen is the best performer across the G10 Tuesday, steadily reversing yesterday’s post GDP price action as the softer risk sentiment across global markets also weighs at the margin.

- USDJPY has slipped back below 153.00 in sympathy and lows at 152.60/37/27 look like potential acceleration points ahead of the 152.10 yearly lows. Note that a trendline support, drawn from the Apr 22 ‘25 low, lies at 151.89 and also marks a key support, emphasising the importance of this area.

- After consolidating its break below the 50-day EMA and 209.60 last week, this morning’s weakness for sterling following labour market data has prompted a solid 0.65% bump lower for the cross. 206.78 represents the next target for GBPJPY, the Dec 16 low.

- Elsewhere, a lack of renewed optimism for the Euro has been weighing on EURJPY, prompting fresh two-month lows below 181.00 this morning. Notably, EURJPY is testing key support at 181.22 - the base of a bull channel drawn from the Feb 28 ‘25 low. A clear break of this support would highlight a stronger reversal and signal scope for a deeper retracement. A move down would open 180.10, the Dec 5 ‘25 low.