JGBS: Slightly Cheaper After A Subdued End To the Week, BOJ SOO On Monday

JGB futures are unchanged after giving up overnight gains fueled by a rally in US tsys.

- Yesterday, US tsys turned to alternative employment data due to the ongoing US Govt shutdown. Revelio Labs' estimate of October nonfarm payrolls growth showed its first negative M/M reading since May.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday's solid rally.

- MNI - Sep Household Spending Below F/Cs, Focus To Get Real Wages Higher: Japan Sep real household spending data was softer than forecast. Real spending fell 0.7% m/m, against a -0.1% forecast (per Rtrs). In y/y terms, we were up 1.8%y/y, against a 2.5% forecast. Given generally softer cash earning outcomes in recent month,s some moderation in spending was not a surprise. The authorities' focus will remain on returning cash earnings growth to real positive territory, as without that, we may see spending trends soften as we progress towards year-end and into 2026.

- Cash JGBs are flat to 1bp cheaper across benchmarks. The benchmark 10-year yield is 0.1bp higher at 1.684% versus the cycle high of 1.705%.

- Swap rates are 1-2bps higher.

- On Monday, the local calendar will see BOJ Summary of Opinions (Oct. MPM) and Leading/Coincident Index data alongside a speech by BOJ Board Nakagawa in Okayama.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: Asia-Pac: AUD/USD Drifts Lower In Sympathy With The NZD

The AUD/USD has had a range of 0.6558 - 0.6586 in the Asia- Pac session, it is currently trading around 0.6560, -0.30%. The AUD has continued to drift lower after topping out above 0.6600, this is in sympathy to the move in the NZD and the general bid tone of the USD. This puts the AUD firmly back within its recent range, and if the USD pullback continues to build the risk is skewed towards further losses, first support lies back toward the 0.6475 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6300(AUD899m), 0.6725(AUD 398m). Upcoming Close Strikes : 0.6545(AUD607m Oct 10) - BBG

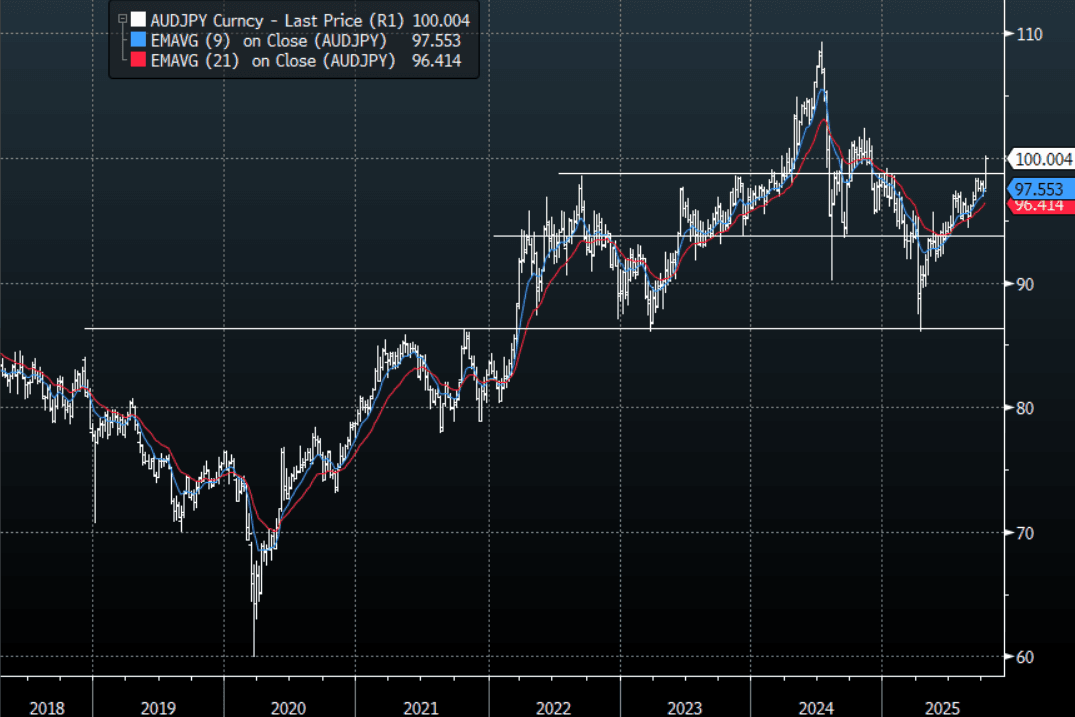

- AUD/JPY - Asia-Pac range 99.89 - 100.20, Asia is trading around 100.05. The pair has surged higher breaking some pivotal resistance. The move extended higher overnight even with risk wobbling. Dips should now continue to be supported as the focus turns toward trying to break above 100 and then beyond.

Fig 1: AUD/JPY spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Asia-Pac: Yields Slightly Higher In A Quiet Session

The TYZ5 range has been 112-19+ to 112-22 during the Asia-Pacific session. It last changed hands at 112-21+, unchanged from the previous close.

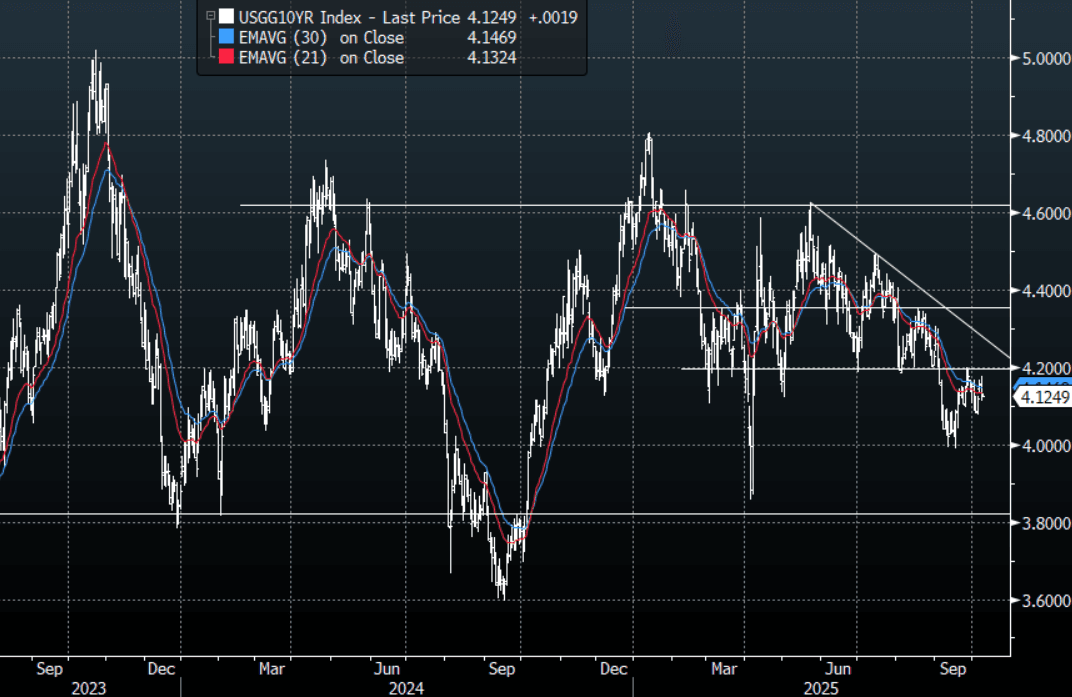

- 10-Year yields bounced to start the week on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade bounces higher looking for a move back towards 4%.

- The US 10-year yield is trading around 4.125%.

- The US 2-year yield is trading around 3.568%.

- MNI Brief - Stephen Miran emphasized the importance of an independent U.S. central bank, and said he will not be playing a part in the search for the next Fed chair.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Data-Light Session, YM Biased Lower, AU-US 10YY Near Top Of Range

ACGBs (YM flat & XM +2.0) are modestly stronger in today's data-light session but off session bests.

- According to MNI’s technicals team, Aussie 3-yr futures (YM) have traded lower, and the contract has cleared the Sep 3 low of 96.435. A break of this level negates the recent short-term bullish theme. This breach signals scope for an extension towards 96.280, the May 15 low on the continuation chart. The short-term resistance to watch is 96.615, the Sep 12 high. Clearance of this level is required to reinstate a bullish theme.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +23bps. At 23bps, the differential is approaching the top of the +/- 30bp range it has traded in since late 2022.

- The bills strip is flat to +2 across contracts.

- RRBA-dated OIS pricing is largely unchanged across meetings today. Markets now assign a 40% probability to a 25bp rate cut in November, with a total of 14bps of easing priced by year-end. This marks a notable shift from late September, when markets had fully priced a 25bp cut ahead of the August CPI release.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data.