JGBS: Shorter Dated Yields Push To Multi-Decade Highs On Stagflation Fears

JGB futures are weaker and at cycle lows, -55 compared to settlement levels, as energy driven stagfl...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

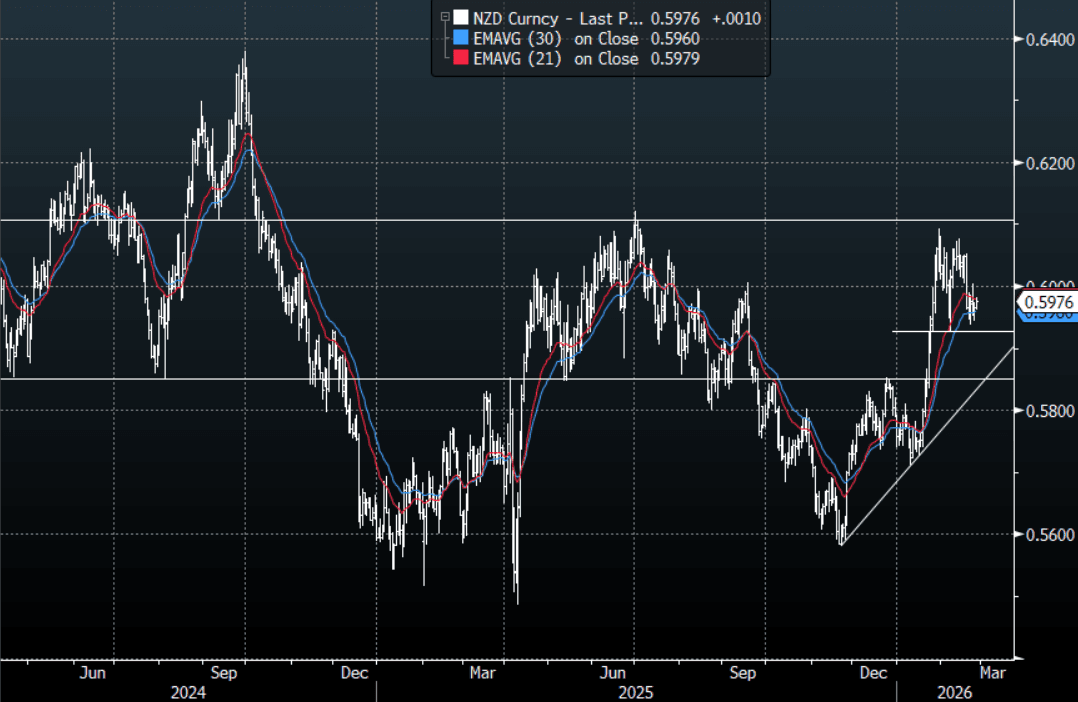

NZD: NZD/USD - Dragged Higher By The AUD & A Softer USD

The NZD/USD had a range today of 0.5961-0.5981 in the Asia-Pac session, it is currently trading around 0.5977, +0.18%. The NZD drifted a little higher in sympathy with the move in the AUD and a USD back under some pressure. The pivotal resistance toward 0.6100-0.6150 continues to cap for now and the dovish read of the RBNZ has delayed its challenge in the short-term. On the day, price remains in the potential 0.5885-0.6015 range, I will be watching to see if the USD bears can regain control. A sustained break back above 0.6015-0.6025 could potentially see another test of the year's highs.

- “New Zealand Central Bank Sold Net NZ$250m in January. RBNZ sold a net NZ$250m in January, according to data released by the central bank on its website.This follows NZ$259m of net NZ dollar sales in December.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5950(NZD408m). Upcoming Close Strikes : 0.5695(NZD577m Feb 27) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 49 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Cheaper After CPI Shows No Signs Of Softening, Q4 Capex Tomorrow

ACGBs (YM -4.5 & XM -3.5) are weaker after Jan's inflation report came in above market expectations. It is difficult to find signs of softening underlying inflation pressures.

- The headline printed at 3.8%y/y, unchanged from Dec (3.7% was the forecast), while the trimmed mean, the RBA's preferred measure of underlying inflation rose 3.4%y/y (against a 3.3% forecast, which was also the Dec outcome).

- The trimmed mean rounded to two decimal places was 3.36% in Jan, from 3.34% in Jan, so only a marginal increase.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session.

- Cash ACGBs are 3-4bps cheaper on the day with the AU-US 10-year yield differential at +68bps.

- The bills strip pricing is -2 to -6, with late whites / early reds weakest.

- RBA-dated OIS pricing firmed across all meetings following today’s data. Pricing shows the probability of a 25bp hike rising from 19% for March (18% pre-data) to 111% by June (99% pre-data) and 166% by December 2026 (150% pre-data).

- Fireside chat with RBA Governor Bullock at the Melbourne University Faculty of Economics & Business Foundation Dinner tonight (1940 AEST). Tomorrow, the local calendar will see Q4 Private Capital Expenditure.

- The AOFM plans to sell A$800mn of the 2.75% 21 November 2028 bond on Friday.

Bloomberg Finance LP

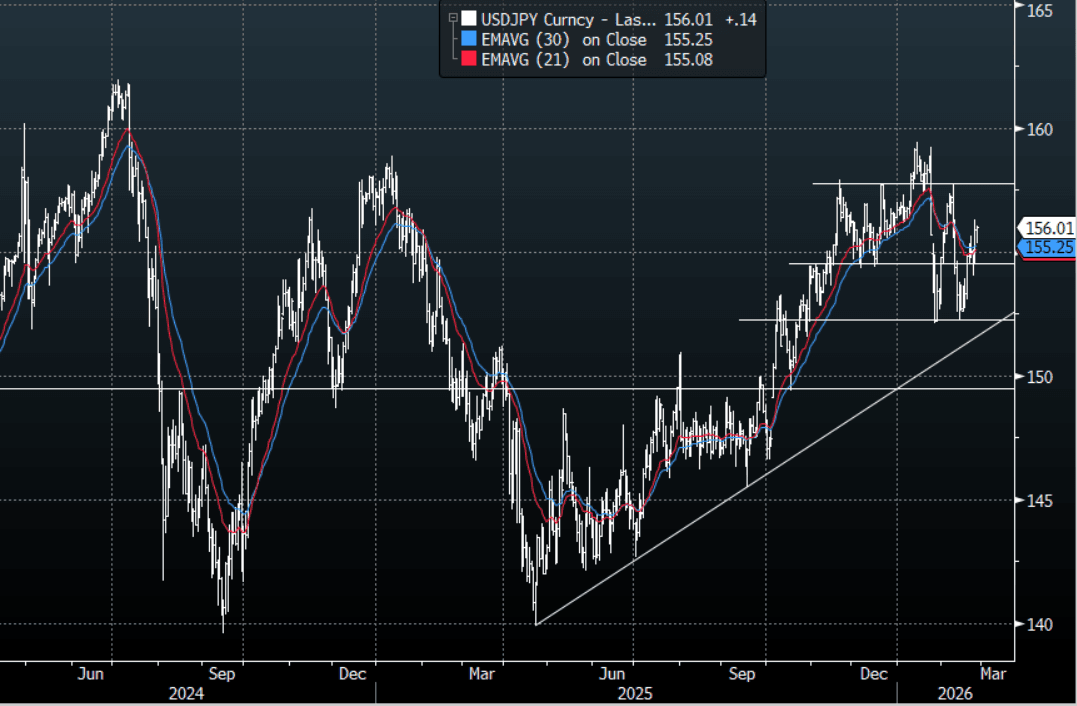

JPY: USD/JPY-Pushback On Takaichi Report Yet BOJ Nominations Point Dovish

The USD/JPY range today has been 155.35-156.04 in the Asia-Pac session, it is currently trading around 155.90. USD/JPY drifted lower as Japanese officials tried to push back on the Takaichi report made yesterday. But the nomination of what is perceived to be doves for the board saw the market move quickly back to 156.00. This potentially brings all the reasons to be short Yen back to the fore. Spare a thought for all the leveraged funds who have significantly reduced their positions. The pair looks to potentially have put a base in toward 152.00 and is looking to re-challenge the 155.50-157.50 area. On the day, look for buyers now on a dip back towards 155.00-155.50 as the pair looks to reassert its upward momentum. The official pushback looks to have been ignored as the market turns its focus back to 160.

- MNI BRIEF: Govt Nominates Doves For BOJ Board. Japan's government on Wednesday nominated Toichiro Asada, a professor at Chuo University, and Ayano Sato, a professor at Aoyama Gakuin University, as Bank of Japan board members, the Nikkei reported. They are in favour of easy policy and active fiscal spending.

- MNI AU - Japan Jan Services PPI As Expected, Sitting Higher Than Headline CPI

- BOJ Deputy Cabinet Secretary - Specifics Of Monetary Policy Left To BoJ: Headlines, via BBG, from Japan Deputy Chief Cabinet Secretary Ozaki, stating that specifics of monetary policy are left to the BoJ. He adds that he is aware of reports around Takaichi's concern around further BoJ hikes but stated that Takaichi didn't have a specific request for BoJ Governor Ueda.

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($2.48b). Upcoming Close Strikes : 153.48($832m Feb 26), 155.00($1.89b Feb 27)) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 132 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P