POLITICAL RISK: SENEGAL-Power Struggle At Top Of Gov't Risks Further Instability

The political environment at the top of Senegalese politics remains in a state of high tension amid the ongoing speculation regarding the country's ability to meet its debt obligations (see EM CEEMEA CREDIT: Senegal: Update post IMF’s Press Briefing). Speaking at a rally in Dakar over the weekend, Prime Minister Ousmane Sonko said the country "would “make sacrifices” and raise taxes on gambling and other services, rather than restructuring its debt. “Anyone who denies the hidden debt should go to prison,” he said, referring to the previous administration that has repeatedly denied that it lied about the state of the country’s finances", reports the FT.

- An apparent political power struggle could further hinder the gov'ts ability to function effectively. President Bassirou Diomaye Faye announced on 11 November that he was replacing Aïssatou Mbodj, one of Sonko's closest allies, at the head of the Diomaye-President Coalition with his own High Representative, former PM Aminata Touré, in order to restructure the group. Opponents claim this is an effective coup within the governing alliance.

- Sonko's supporters within his left-wing African Patriots of Senegal for Work, Ethics and Fraternity (PASTEF) party have claimed Diomaye Faye does not have the power to replace Mbodj. They argue the Diomaye-President Coalition effectively ceased to exist after the 2024 presidential election and that the restructuring has already taken place, with the coalition set to become the APTE (Patriotic Alliance for Work and Ethics).

- Diomaye Faye is seen to largely owe his presidency to the backing of Sonko in the 2024 election, where he was selected as PASTEF's candidate at a time when it was unclear if Sonko would be allowed to run. As such, Senegalese politics remains in a state of friction, where Sonko's supporters want to see him installed as president ASAP, but Diomaye Faye is unwilling (and has no obligation) to give up the presidency.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W AUCTION: NON-COMP BIDS $397 MLN FROM $69.000 BLN TOTAL

- US TSY 17W AUCTION: NON-COMP BIDS $397 MLN FROM $69.000 BLN TOTAL

UK DATA: August Monthly Activity Data: Modest Gain Expected, Led By Services

All sell-side previews we've read look for a 0.1% M/M rise in GDP in the August print (in line with Bloomberg consensus), following July's flat reading. The growth is expected to be services-led, with the monthly index of services (a subcomponent of GDP) also expected to rise 0.1% M/M (vs 0.1% July), with two-sided risks. Note that the monthly GDP series will be revised to take into account the revisions seen alongside the publication of the final Q2 data on 30 September that incorporated the Blue Book as well as extra data incorporated for the July print.

- August's PMIs mostly surprised to the upside, with Services PMI jumping to a 16-month high at 54.2. Retail sales also grew by 0.5% M/M during August, partly attributed to good weather - Goldman Sachs estimate that this would contribute 2-3bps to headline GDP growth. However, NatWest Markets note that Barclaycard data suggest a slight cooling in demand in August. Elsewhere, July's NHS strikes did not continue into August and will therefore providing a boost to M/M services in August.

- The main downward driver is expected to be construction output. Sell-side forecasts converge around -0.2% M/M (though the Bloomberg surveys sees a wide range of estimates from -0.6% to +0.5%).

- There is little of note for industrial production (Bloomberg consensus 0.2% M/M), where an adjustment is seen after July's surprisingly weak M/M print at -0.9%. Stronger oil output is flagged, but much of the growth in industrial production is expected to be due to base effects. August's Manufacturing PMI fell 0.3 points short of consensus, at 47.0.

- Looking ahead to the quarterly print for Q3 (releasing 13 November), the sell-side previews we've read point to 0.2% Q/Q growth, slightly undershooting the BOE's forecast of 0.3% from the August MPR (unchanged from May).

- Factors noted include September's data fully incorporating the impact of the Jaguar Land Rover shutdown, as well as much of 2025H1 strength being driven by transitory factors (frontloaded spending, government consumption, inventory accumulation), both suggesting a weaker reading.

- An interesting point here is that the Bank's own survey indicator model also forecasts an undershoot for Q3 GDP, aligning with the sell-side on 0.2% Q/Q growth.

- Thursday's release also comes alongside trade data for August (also 07:00 BST).

- The trade balance is seen at GBP-4.81bln (Bloomberg consensus), versus GBP-5.26bln in July.

- Note that this will be the last monthly GDP release used by the OBR in its Budget forecasts.

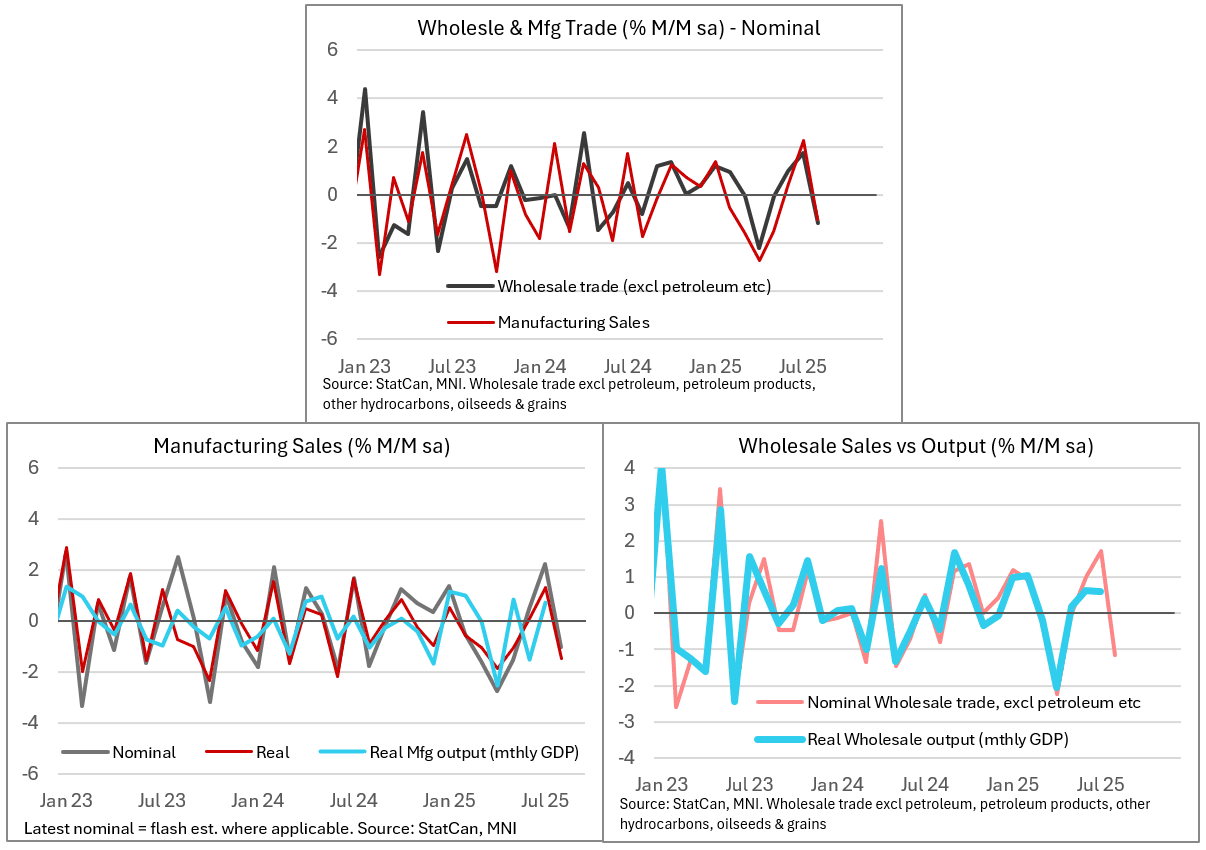

CANADA DATA: Sales Figures Point To Softer Activity In August, Led By Autos

Canadian manufacturing and wholesale sales (Ex-petroleum, products, other hydrocarbons, oilseed & grains) came in slightly better than expected in September, at -1.0% / -1.2% M/M respectively. This compares to the advance estimates of -1.5% for manufacturing (prior rev to 2.2% from 2.5%) and -1.3% for wholesale sales (1.7% prior rev from 1.2%) and despite is suggestive of a drag on August GDP from wholesale and manufacturing output (the August GDP advance estimate is for flat growth M/M overall).

- From a momentum perspective both sales categories appear to be past the worst - but the auto industry appears to remain under duress, with the trade conflict with the US continuing to pose headwinds.

- Looking first at manufacturing sales, the decline nonetheless pared the contraction in the 3M/3M annualized pace to -1.3%, which was a 5th consecutive drop but far better than the -17.6% posted in June that helped drag on Q2 GDP. In volume terms, higher prices meant that the picture was less positive: they fell 1.5% in August, worst in 4 months and erasing the 1.3% rise prior. They're contracting at a 3.4% quarterly pace, with the level of shipments at the lowest since September 2021. Year-to-date through the first 8 months of the year, sales are down 1.0% Y/Y.

- Manufacturing inventories ticked up 0.3% to the highest since November 2023, with the inventories-to-sales ratio remaining relatively steady over the last 4 months at a relatively high 1.75x. StatCan noted lower sales in 12 of 21 subsectors, with the biggest drops coming in the transportation equipment (-5.7%, with motor vehicle parts falling 5.2% and vehicles 3.3% amid "lower than typical seasonal sales of motor vehicle parts as well as production slowdown at a major auto assembly plant in Ontario") and food (-1.9%) subsectors, while primary metal sales increased the most (+3.6%).

- And as for the wholesale data, sales fell in 3 of 7 subsectors, led by motor vehicle parts/accessories (-8.8%). Ex-petroleum, products, other hydrocarbons, oilseed & grains sales rose for the 3rd consecutive month (1.3%) and is rising at a solid 3.9% 3M/3M pace which is a post-April best. In volume terms, gains were firmly negative in the month however (-2.7% M/M), the first drop in 3 months, though the 3M/3M ann rate was still elevated at 6.8%. Overall wholesale sales jumped 7.4% on a 3M/3M annualized basis, which would be the fastest since February, though again that's in nominal terms.

- Inventories-to-sales for ex-petroleum etc picked up to 1.58x from 1.55x prior, which excluding the first 2 months of the pandemic was the highest since at least 2000 - suggesting a building overhand that could depress future activity.