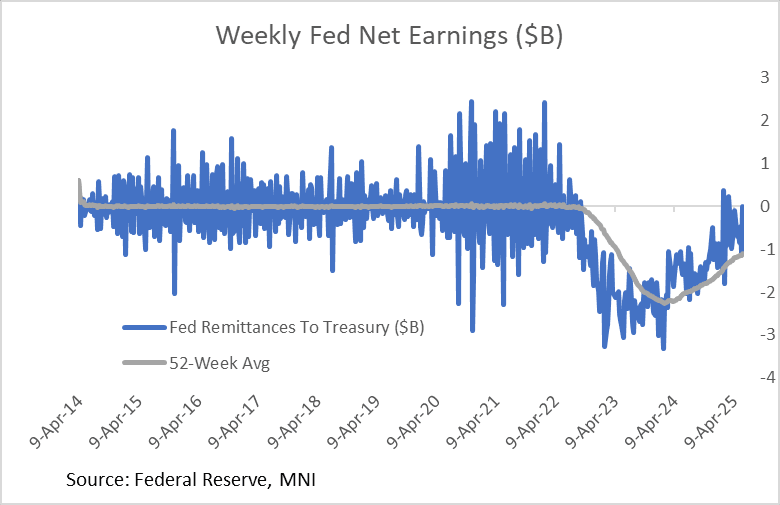

FED: Sen Cruz: "Robust Discussion" On Eliminating Interest On Fed Reserves

Jun-05 18:48

Senator Ted Cruz said today on CNBC (link to video) that he and his Senate colleagues this week "had a robust discussion" Wednesday about eliminating the Fed's ability to pay interest on reserves (IORB).

- Cruz: "The Federal Reserve pays banks interest on reserves, for most of the history of the Fed. They never did that, but for a little over a decade, they have. Just eliminating that saves a trillion dollars. So there's a lot of things we can do to rein in spending. And I'm urging my Senate colleagues, let's let's show responsibility for the next generation. Let's do what's right."

- Asked whether such legislation would go through, Cruz said: "I don't know. I can tell you, we had a robust discussion about it yesterday, and we're having a lot of robust discussions... I don't know if it's likely. It is certainly possible....The Fed used to generate money for the American taxpayer. It's now costing about $100 billion a year. And the way it used to work is, if banks wanted to make money, they had to go invest that money and make loans and take care of it on themselves. I don't see a reason why the taxpayers ought to be paying for it. That's one example that generates a trillion dollars."

- It's unclear how serious this proposal is, but were IORB to be eliminated, then among other issues, it would greatly complicate the Fed's ability to administer policy rates. Reminder from the NY Fed: "The IORB is the rate that the Fed pays on the reserves that banks hold overnight in their Fed accounts, thereby setting a floor on the rates at which banks lend overnight in the fed funds market. The Fed has paid IORB since October 2008."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Macro Since Last FOMC: Growth - Confidence Slumps [2/2]

May-06 18:44

- This relative resilience in the hard data, which still doesn’t yet reflect the escalation in US trade policy in April, is in firm contrast to soft data.

- The Conference Board reported consumer confidence fell for a fifth consecutive month in April to its lowest since May 2020, although its expectations component was even weaker at its lowest since Oct 2011. After a 12.5pt decline to 54.4, expectations are "well below the threshold of 80 that usually signals a recession ahead" per the Conf. Board press release. This came as "expectations about future income prospects turned clearly negative for the first time in five years".

- These findings are echoed in the University of Michigan consumer survey although it’s flash/final readings suggest the partial backtracking on reciprocal tariffs on Apr 9 after market turmoil following Apr 2 “Liberation Day” announcements prevented an even worse reading.

- Specifically, consumer sentiment fell from 57.0 in March to 52.2 as opposed to 50.8 in the preliminary reading (which had been collected Mar 25-Apr 8), although that’s still the lowest since mid-2022 and below any month for sentiment through 2008-09. Within the survey, unemployment expectations for twelve months out have seen two months with an index close to lows seen in 2008/09 (lows here being higher unemployment, and specifically the pace of increases rather than level of unemployment).

US OUTLOOK/OPINION: Macro Since Last FOMC: Growth - Solid Domestic Demand [1/2]

May-06 18:42

- Real GDP growth was technically negative in Q1 although not as bad as it could have been amidst particularly wide uncertainty in tracking estimates, not least owing to a surge in monetary gold imports that show in merchandise trade data but not national accounts.

- Real GDP fell -0.3% annualized, close to a consensus of -0.2% but one that hadn’t fully adjusted to a surge in consumer goods imports in advance March data just the day beforehand. A median of 26 analyst estimates updated the day prior expected -0.8% whilst the Atlanta Fed’s GDPNow gold-adjusted estimate was -1.5%.

- That clearly marked a sharp slowdown from the 2.45% in Q4 and 3.1% in Q3. However, hiding beneath some significant crosscurrents from net trade and inventories, private domestic demand was surprisingly robust. At 3.0% in Q1, it maintained the 2.95% in Q4 or 3.0% averaged in 2024, thanks to a surge in non-residential investment plus also firmer than expected personal consumption. Of course, there remain significant question marks over the extent to which it’s been boosted by tariff front-running.

- March's Personal Income and Outlays report showed a strong, partly tariff-related, pickup in real consumption in March (0.7% M/M after 0.1% in Feb and -0.4% M/M in Jan) that couldn't offset a weaker quarter as a whole.

- That said, personal income dynamics were fairly robust at quarter-end, suggesting that despite collapsing sentiment, there is still scope for consumer demand to remain underpinned heading into Q2.

- The least we can say is that if there is a recession looming, it did not start in March based on these data.

COMMODITIES: Crude Rebounds Amid Mid-East Tensions, Gold Recovers

May-06 18:32

- Crude has rebounded back to levels seen late last week amidst signs of rising tensions in the Middle East, while the market continues to digest oversupply risks after OPEC+ decided on a large output hike for June.

- WTI June 25 is up by 3.6% at $59.2/bbl.

- OPEC+ agreed to increase output by 411k b/d in June, following a similar rise in May.

- A medium-term bearish trend in WTI futures remains intact and short-term gains are considered corrective.

- Attention is on $54.67, the Apr 9 low and a bear trigger. Resistance to watch is $64.13, the 50-day EMA.

- Meanwhile, gold has rallied by a further 2.5% today to $3,417/oz, taking total gains this week to over 5%.

- The move comes amid a further decline in the dollar, which will have provided some support to the price of gold, along with continued haven demand stemming from ongoing tariff and geopolitical uncertainty.

- The rally in gold this week suggests that the correction between Apr 22 - May 1 is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3,500.1, the Apr 22 all-time high. Clearance of this level would confirm a resumption of the primary uptrend.

- Elsewhere, copper has also rallied by a further 1.3% to $476/lb, taking total gains this week to almost 2%.

- For copper, key short-term resistance has been defined at $498.25, the Apr 23 high. A resumption of weakness would expose $436.00, the Apr 10 low.