MNI US Employment Insight: Good Enough To Keep The Fed Patient

Jun-06 16:53By: Chris Harrison and 1 more...

Employment+ 4

Download Full Report Here

EXECUTIVE SUMMARY

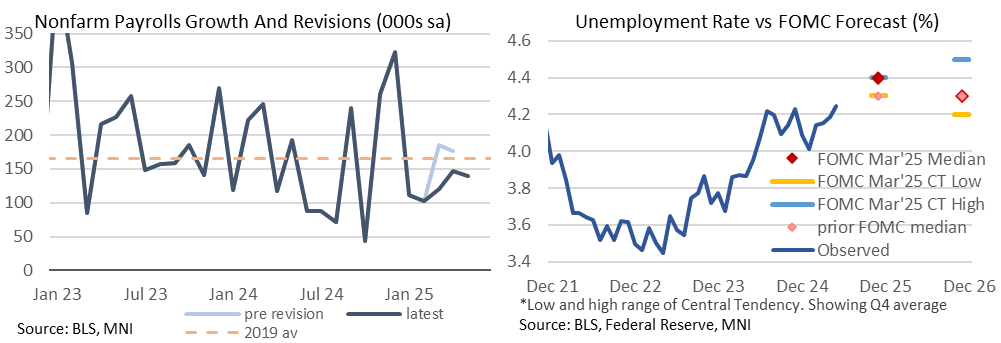

- Nonfarm payrolls growth modestly beat expectations in May with 139k (cons 126k) although it was more than offset by large two-month downward revisions of -95k.

- It leaves a three-month average of 135k, solid considering a slide in immigration. Long-term breakeven pace is assumed around the 100k mark.

- Note the large downward revisions in transportation & warehousing: the previous data had suggested that this sector was being buoyed by the strong inventory build seen in Q1 on tariff front-running, but the latest vintage points to a recent net negative impact from tariffs.

- The main standout statistic from May's Household Survey is the tick up in the unemployment rate to 4.244% from 4.187%, which while keeping the rate at 4.2% in line with consensus was the highest unrounded unemployment rate since October 2021.

- This suggested that upward pressure on the rate continued in more or less the steady but not rapid pace of deterioration envisaged by the Fed, and in a mixed Household report, most statistics underlying pointed to steady weakening in the labor market.

- There was a sizeable beat for AHE growth (0.4% M/M vs 0.3% expected), considering the average work week was as expected at 34.3.

- The lack of a sharper deterioration in the payrolls report saw a large hawkish reaction as it reversed the dovish build-up into the release that started with last week’s jobless claims increase and continued with Wednesday’s ADP employment and ISM services misses.

- It leaves a path back closer to recent hawkish extremes, with a next cut fully priced for October and 45bp of cuts to year-end. Out of interest, that was 79bp after last month’s NFP report.

- At least one analyst (Citi) pushed back their expectation of the next Fed cut (to September, from July).